This Bank of America Presentation Reveals an Important Insight

The presentation that Bank of America (NYSE: BAC) created for its annual investor day this year is full of interesting insights, but one thing caught my eye.

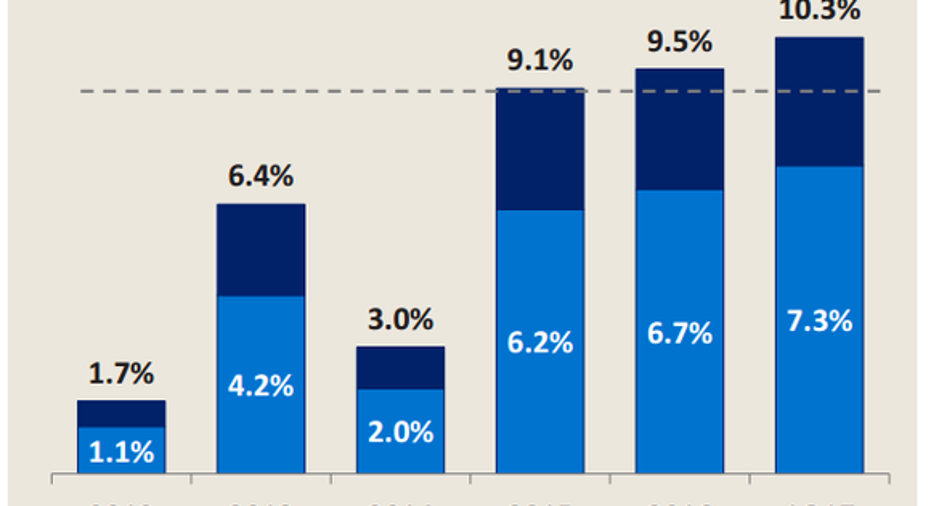

It's a chart of Bank of America's profitability since 2012, measured by return on average tangible common equity. This is the primary profitability target in the bank industry. It's calculated by dividing a bank's net income by its tangible common shareholders' equity.

Data source: Bank of America.

An obvious takeaway from this chart is that Bank of America's performance is not only improving, but it's also getting more consistent. While the bank's earnings bounced around before 2014, they've since settled into a gradually upward-sloping trend.

This is important for a number of reasons. Stable earnings tend to support higher credit ratings, which bring down a bank's cost of funds. Less volatile earnings are also viewed favorably by regulators when they decide to approve or deny big bank capital plans as a part of the annual stress test. Finally, predictable earnings often translate into a higher stock valuation, as investors are known to abhor uncertainty.

Yet, while the trend toward consistency is important, it's not what caught my eye. What I noticed instead was the dotted line at 9%. That's Bank of America's internal estimate of its cost of capital.

Cost of capital refers to the opportunity cost associated with investing in a specific stock. It's somewhat of an esoteric concept, but the important thing to remember is that for a bank to create value for shareholders, its return on tangible common equity must exceed its cost of capital.

Banks that succeed at this, tend to trade for premiums to their book values, while banks that come up short generally sell for discounts to book value. You can see this relationship clearly in the chart here.

Bank of America Tower (center) looms over Manhattan's Bryant Park. Image source: Getty Images.

I've previously estimated Bank of America's cost of capital to be 11.7%. Another analyst has put it above 12%. Bank of America's own estimate is obviously more favorable.

This aside, Bank of America has made it clear that a 9% cost of capital isn't its target profitability. It's instead pegged a 12% return on tangible common equity as one of its three principal performance goals.

Bank of America still has ground to cover before it reaches that target, as its return on tangible common equity in the first quarter of this year was only 10.3%. But based on the bank's projections, it could be there by the end of this year.

10 stocks we like better than Bank of AmericaWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Bank of America wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of May 1, 2017

John Maxfield owns shares of Bank of America. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.