These Social Security Income Limits Could Reduce Your Benefits

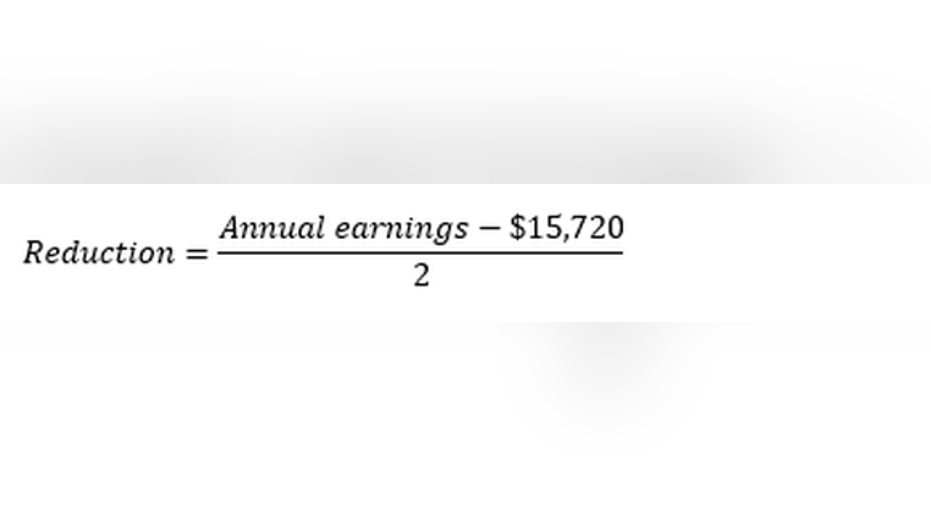

If you're working and drawing Social Security, your benefits may be subject to income limitations. For those who won't reach normal retirement age by the end of 2016, any earnings in excess of $15,720 ($1,130 per month) could reduce your Social Security benefits by $2 for every $1 above this threshold. Beneficiaries who will reach retirement age during 2016 are subject to a higher exemption amount.

Here are the details of the Social Security earnings test, and what it could mean to your monthly benefits as well as your future Social Security income.

Three categories of Social Security beneficiaries

In order to determine the effects of working on Social Security benefits, the Social Security Administration (SSA) separates beneficiaries into three categories.

- The first category includes people who receive benefits, but will attain their normal retirement age after 2016. In this group, the first $15,720 of earnings are exempt and will have no effect on the ability to collect benefits. Any earnings above this amount will result in a benefit reduction of $1 for every $2 in excess earnings.

- The second category includes beneficiaries who will attain their normal retirement age during 2016. This group has a higher exemption amount of $41,880, as well as a more favorable reduction formula. Their benefits are reduced by $1 for every $3 in excess earnings. What's more, only earnings before the month of reaching normal retirement age are counted.

- The final group includes Social Security recipients who have attained their normal retirement age (66 for those reaching retirement age now). This group is free to work and earn as much as they can without any benefit reduction.

Examples

First, consider a 63-year-old whose calculated Social Security benefit is determined to be $1,000 per month. If this person also receives a salary of $30,000 from working, the excess over the $15,720 threshold, or $14,280 will be counted for benefit reduction purposes. Because of their age, this individual's benefits will be reduced by $1 for every $2 of excess earnings, so this translates to a $7,140 annual benefit reduction, or $595 per month. Therefore, their $1,000 calculated monthly benefit will be reduced to $405 because of their earnings.

Next, consider a 65-year-old beneficiary who will turn 66 in September, and who receives a $1,500 monthly Social Security benefit. Let's say that this individual has a job with a $60,000 annual salary -- or $5,000 per month. Although this salary is above the $41,880 earnings cap, the only earnings that count are those from January through August, or eight months' worth. Since this only represents $40,000 of the total salary, there will be no benefit reduction.

You can get it back later

Finally, it's important to point out that even though the Social Security earnings test can reduce your monthly benefit amount, there's a positive trade-off later. For every month's benefits that the SSA withholds, you're treated as having taken benefits a month later than you actually did.

If your Social Security benefits are withheld because of your earnings, the effect is that your monthly benefit will be permanently increased once you reach normal retirement age and the earnings test no longer applies to you.

In other words, don't let the fear of losing some of your benefits prevent you from filing for Social Security early if you want to do so. As you can see from the example, you could still potentially receive some Social Security income in the meantime, while boosting your benefits for later on when you've reached normal retirement age.

The article These Social Security Income Limits Could Reduce Your Benefits originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.