These 3 Dividend-Paying Gold Stocks Are Up Around 100% in 2016

Gold is often included in an investor's portfolio as a diversification play. Income investors searching for dividends, though, might not find the generally low-yielding fare in the precious-metals space all that interesting. However, if you want that diversification and income, you can find it in Barrick Gold (NYSE: ABX), Newmont Mining (NYSE: NEM), and Yamana Gold (NYSE: AUY), three dividend-paying gold stocks that are up about 100% so far this year.

Yamana Gold employees working a mine. Image source: Yamana Gold

Eye-catching

First off, investors need to think about what a gain of 100% means. Essentially, the stocks of Barrick, Newmont, and Yamana have roughly doubled in a little more than 10 months' time. In fact, despite that heady gain, each is off from earlier levels, with Yamana having fallen by more than a 40% from its mid-year highs (it's "only" up around 90% for the year at this point). That speaks to something very important in the gold and precious-metals space -- volatility.

The big advance in 2016 has come because gold and silver have risen off the multi-year lows reached at the start of the year. By stepping in after such a large advance, you're taking on added risk that gold prices move lower and gold stocks follow it down. However, we could also be at the beginning of a longer-term uptrend, in which case gold will fluctuate as wildly as it always has but trend generally higher. That would lead gold stocks higher.

Ready for the turn

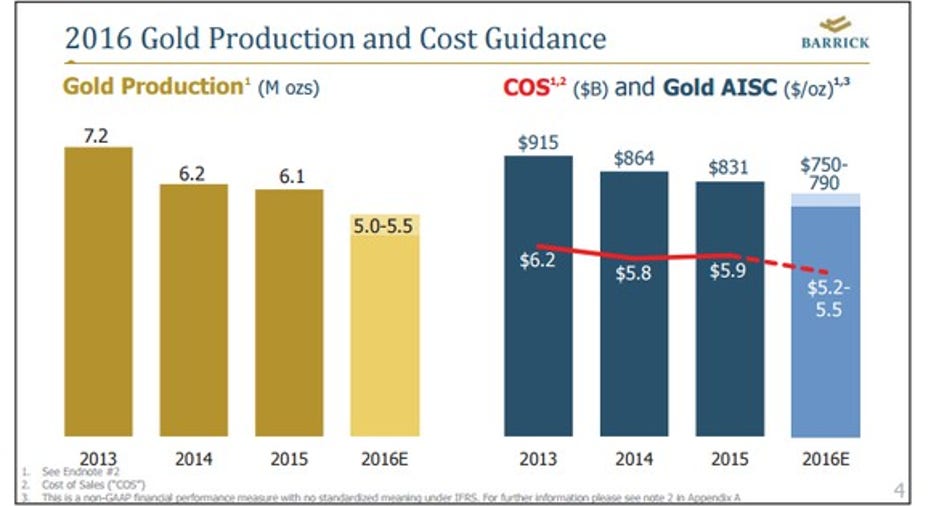

That said, a lot has changed with the precious-metals miners. When times were flush, spending on growth projects was all the rage. With prices for gold and silver falling, many of these investments fell to the wayside and cost-cutting become far more important. For example, Barrick Gold is hoping to reduce its all-in sustaining costs, a measure of how much it costs to mine an ounce of gold, by as much as 18% by the end of the year compared with what it cost in 2013.

Clearly, this isn't unique to Barrick. Newmont has done even better on the cost front, as it expects to trim its all-in sustaining costs by more than 20% over the same time period. Yamana hasn't done quite as well on the cost front. However, through the first half of the year, the miner was able to trim its all-in sustaining costs by around 8% from 2013's levels. The big picture here for all three miners, though, remains that costs are going down. That means they will be better able to handle gold's price swings going forward. And if gold goes up, well, more money will flow through to the bottom line.

Barrick Gold's AISC and production over time. Image source: Barrick Gold.

Some key differences

There is one interesting difference between these miners, though. Barrick expects to reduce its gold production by around 25% from 2013 levels, focusing on its best assets in an attempt to trim costs. Newmont is expecting to keep production this year pretty much flat with the 5.1 million ounces of gold it dug up in 2013. And Yamana Gold is hoping to grow its production as much as 10% above 2013 levels this year.

That provides a slightly different view of each company. Barrick is kind of circling the wagons, Newmont is holding the line, and Yamana is trying to balance growth against cost, which helps explain why it might be having a little more trouble reducing its all-in sustaining costs.

Which one catches your eye will pretty much depend on your view of the world. All three are better prepared today for gold-price swings than they were just a few years ago. But if you see the glass half empty (gold prices could stagnate or fall), then Barrick and Newmont might be the better options. If you think the glass is half full, on the other hand, then Yamana's push to expand would be more enticing, with Newmont's efforts to hold the line a fallback option.

That said, of the trio, Barrick has the heaviest debt load. Long-term debt makes up roughly 50% of the giant miner's capital structure, something that could crimp the bottom line if gold prices sink. The company is well aware of the issue, making debt reduction a core goal for the miner today. That figure, meanwhile, is around 30% for Newmont, providing the miner with a lot more breathing room to adjust to volatile precious metals markets. And Yamana, which is the growth-focused name, counts long-term debt at just about 25% of it capital structure. So the company with the most risk on the execution front appears to have plenty of fire power left on its balance sheet to support those efforts.

Newmont Mining dividend policy. Image source: Newmont Mining.

Dividend plays?

All of that said, don't expect huge dividends from this trio. The yield on each is half a percent or less -- you won't get rich on dividends here. But those payouts at least give you something, and a lot of competitors in the space don't pay dividends at all. And you'll still benefit from the diversification aspect of owning a gold miner.

There's one last topic to touch on. Newmont has a unique dividend policy that ties its distribution to the price of gold. Thus, if gold goes up, you can predict the payout you're likely to receive (see the preceding chart). At some level, that might make it the most conservative play and the one that's right for dividend-focused investors looking to include a gold miner as a diversifying investment.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Reuben Brewer has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.