The Worst Mistake Cintas Corporation Investors Can Make Right Now

This picture's not about the food; it's about the uniform. Image source: Cintas.

It's hard to suggest that Cintas Corporation is anything but a great company. Over 30 years of annual dividend increases and revenue growth of nearly 20% over the past five years are hard to argue with. But that's the past, and while you shouldn't expect Cintas' performance to sucker-punch you, don't forget about the impact the economy plays in all of this. In other words, don't get too excited right now.

Boring, but neededSo Cintas' business is pretty boring. Its largest operations is selling, renting, and maintaining uniforms. This business is about 85% of the top line. The other top-line category is providing first aid and safety equipment, 15% or so. That said, the company's product offering list is pretty long, including such things as welcome-mat maintenance and bathroom cleaning services. But there's one thing about everything Cintas does that you need to keep in mind: Its customers are businesses.

When Cintas' customers are dealing with an economic pullback, there's a tap-on effect. It's true that Cintas has a wide customer base, with around a million businesses using its services, so no single customer is all that important. But that diversification just makes Cintas more dependent on the broader hiring and firing cycles that go along with economic booms and busts. So in the end, Cintas, despite a solid core operation that's well diversified, is still something of a cyclical business.

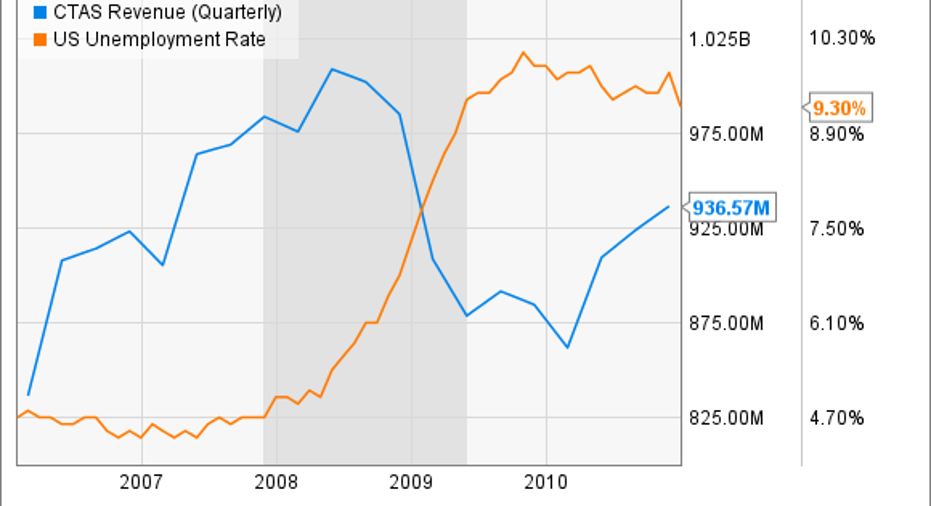

Look no further than the deep 2007-to-2009 recession for proof. The following graph spells it out pretty clearly: As the percentage of the workforce that's unemployed goes up, Cintas' revenues go down -- the shaded area in the graph is the recession. This dynamic makes complete sense when you step back and think about it. If businesses are laying people off, they don't need as many uniforms cleaned.

CTAS Revenue (Quarterly) data by YCharts

But here's the thing. The company's stock price tends go along for that economic roller-coaster ride, too. At the depths of the 2007-to-2009 recession, Cintas' share price was off as much as 50% from the highs before the recession. So an economic downturn can take a big toll on the company's share-price performance.

Don't look now!That's what makes today so interesting. Although the U.S. economic expansion coming out of the 2007-to-2009 recession has been anemic at best, the economy has been heading higher for some time. Sure, that's done wonders for Cintas' business, as the following chart shows. But maybe things are too good.

For example, Cintas' price-to-earnings, price-to-book, price-to-cash flow, and price-to-sales ratios are all above their five-year averages. Add in the long economic recovery without a notable pullback, like a recession, and maybe, just maybe, investors are a little too optimistic right now. The stock is trading near all-time highs.

Buying opportunitySo if there's an economic downturn that includes a notable drop in employment, you could see Cintas' share price fall dramatically. That doesn't suddenly make Cintas a bad company. But it does mean that current shareholders might want to step back from buying more right now, and those looking into initiating a position might want to wait. The next recession -- and we will have one eventually -- could lead to a bargain price. At the very least, such a downturn would take the edge off the high multiples being afforded the company today.

The article The Worst Mistake Cintas Corporation Investors Can Make Right Now originally appeared on Fool.com.

Reuben Brewer has no position in any stocks mentioned. The Motley Fool recommends Cintas. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.