The Simplest Way to Find Your Retirement Number

How much cash do you need to reach your retirement number? We'll help you figure out. Photo: Tax Credits, via Flickr.

In some finance circles, "The Retirement Number" has become the holy grail of financial planning.

This represents the size that your nest egg must grow to in order to retire without ever having to work for money again. It is based on the idea that you can safely withdraw 4% of your nest egg in Year One of retirement, and adjust that number for inflation every year thereafter.

While the process of figuring out this number is important to help you get your bearings, it's also important to realize that the vast majority of retirees find themselves to be quite happy in retirement -- even though most of them retired with nest eggs far below their retirement number.

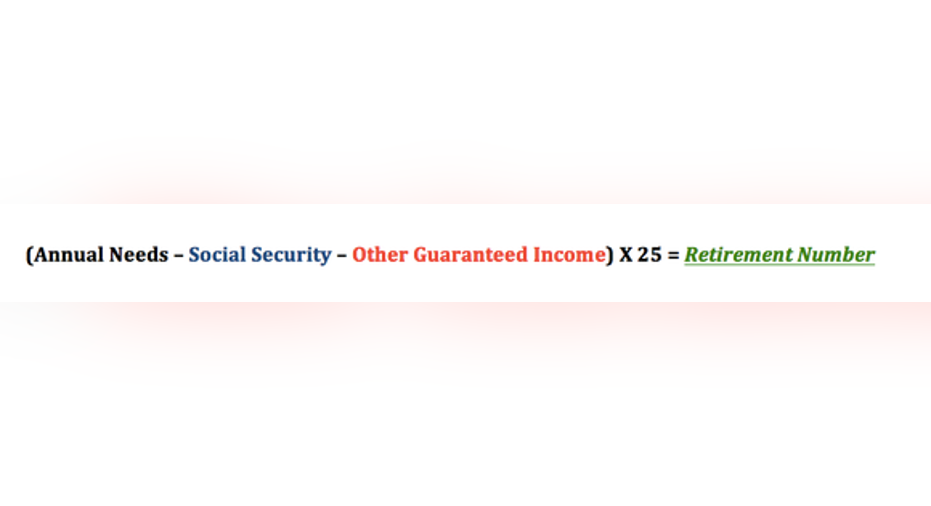

That being said, here's how it works:

Let's break it down piece by piece.

Annual needsThis is a huge variable under which you have enormous control. Some people can't imagine living a life without the height of luxury. Others are just fine knowing that their basic needs are being met and that they can pursue their own passions on their own time.

Where you fall will have an enormous influence on what your own retirement number is. If you're trying to figure out what your own needs in retirement will be, I suggest you consider a few things:

- Transportation and pension/Social Security spending (as in Social Security taxes) will -- on average -- fall precipitously.

- Housing costs will fall, but remain your biggest expense. Even if you own your home, upkeep and taxes will still exist.

- Healthcare will eat up a bigger portion of your spending, though probably not as much as you think.

Social SecurityEveryone's Social Security check will be different. If you'd like to get an up-close look at how much you'll be receiving from the program, I suggest you check out the page that the Social Security Administration has devoted to that question, available here.

There are two variables that you need to take into consideration. First, the age at which you'll start receiving benefits will play a big role in how large your monthly check will be. Second, if you believe that Social Security may be cut in the future, it would be wise to cut your benefit by 25% to give you a reasonable margin of safety.

Other guaranteed incomeUsually, such income is defined as a "defined benefit" package, and is more commonly known as a pension. Though pensions are less common in the private sector today among newer workers, there are still a number of (1) older workers, and (2) public employees who can be reasonably certain that their pensions will be around come retirement time.

As with Social Security, it may be worth investigating the solvency of your specific pension fund. Some have run into troubles and have had to ask beneficiaries to accept cuts to keep the programs alive. If you are worried that something along those lines might happen with you, it would again be wise to cut your assumptions by 25% to give yourself a margin of safety.

What you're left withIn the end, we multiply what is left -- what your nest egg will have to provide -- by 25. That's the inverse of taking 4% per year to help fund your retirement.

If you can hit this number, you are likely in good shape.

But I would be remiss if I didn't touch back on a point I made at the beginning. If there's one thing we humans are bad at doing, it is predicting our own level of happiness. The main reason for this is that we almost always under-appreciate our ability to adapt to our situations.

If you find that you will fall well below your retirement number, don't give up hope. It's important to save and invest what you can right now, but it's also important to know that if you have to downshift your lifestyle, it isn't the end of the world. Given a year to adjust, you'll likely find a new level of contentedness that's based on things that have nothing to do with your retirement income.

Achieving your "retirement number", in the end, is simply an effort to avoid such an adjustment.

The article The Simplest Way to Find Your Retirement Number originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.