The $94,000 Mistake the Average American Family Makes in Saving for Retirement

Don't make this retirement savings mistake if you don't have to. Photo: Tax Credits, via Flickr.

Retirement is a tricky subject to write about. On one hand, we Americans are woefully underprepared for our Golden Years compared to what "experts" say we need. On the other hand, the very idea of "retirement" -- and the associated decades of saving -- is an incredibly new idea for humans. We simply aren't wired for it.

It doesn't stop there: one person can live very happily on $25,000 per year, while another can't bear to think of spending under $1 million. You can see why a one-size-fits-all sound bite is just about impossible to come by.

This article is no exception -- but a nugget of truth recent studies have revealed is worth considering.

The effect of "leakages"No, we aren't talking about a broken septic tank, which might actually be worse. Instead, we're talking about a phenomenon that can occur when you decide to raid either your 401(k) or Individual Retirement Account for any reason that's not directly related to providing income in retirement.

Generally, there are three ways that retirement account leakage can happen:

- In-Service Withdrawals: hardship withdrawals and those made penalty-free after reaching 59 years old.

- Cash Outs: usually occur when someone changes jobs and, instead of rolling over their 401(k), chooses to cash out the balance and pay taxes and penalties on it.

- Loans: in order to avoid certain penalties, some individuals take out loans using their retirement accounts as collateral.

When you're young and retirement seems like a distant dream, deciding to pursue any one of these three strategies seems benign at worst. And on the surface, they don't look so bad. According to the study, in any given year, the nation's 401(k) and IRA plans suffer leakage equivalent to about 1.5% of all assets.

In truth, however, the effects can boggle the mind. Because a 30-year old worker still has over three decades of work before retiring, that's three decades of compounding growth that they miss out on completely.

What happens to your 401(k)?Using data provided by both Vanguard and the Census Bureau's Survey of Income and Program Participation (SIPP), researchers at Boston College's Center for Retirement Research were able to offer solid numbersto chew on -- and they are surprising, to say the least.

The researchers made the following assumptions:

- An individual saves from age 30 to 60, with a starting salary of $40,000, with inflation-adjusted increases of 1.1% per year.

- The individual contributes 6% of his/her salary each year, with a 50% employer match. These investments earn an inflation-adjusted return of 4.5% per year.

- These savings suffer an average leakage rate of 1.5% per year, with higher leakage occurring earlier in one's career.

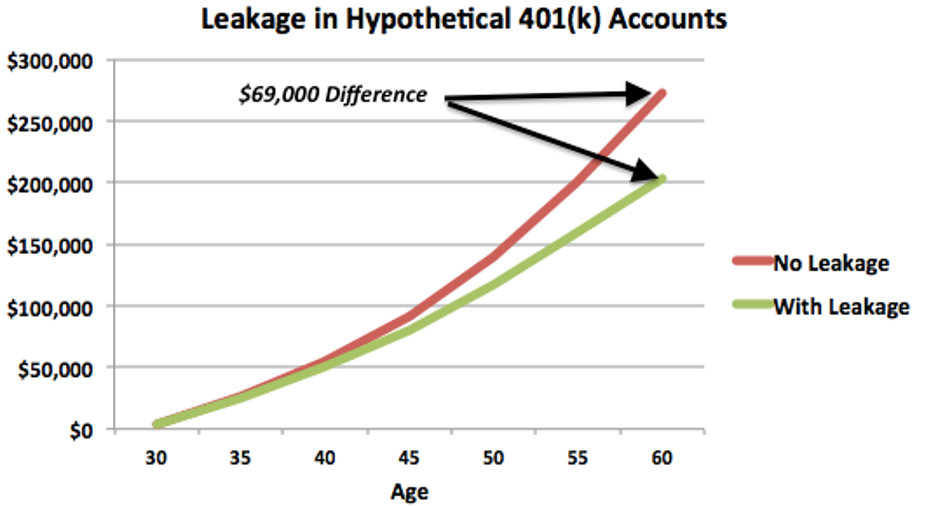

As you can see, the effects of time and compounding have a significant effect.

Author's calculations, based on Boston College researcher's assumptions.

The account that has no leakage at all reaches age 60 with a balance of $272,000. The one with leakage is a full $69,000 -- or 25% -- less: $203,000.

What happens to your IRA?Because very few people actually hold the same job throughout their entire life, researchers also created a hypothetical situation using data from Vanguard and SIPP. All of the above remained the same, only this time:

- The individual was assumed to have rolled over his/her 401(k) into a Roth three times, at ages 30, 40, and 50.

- Withdrawal rates were slightly different, and were based on the average IRA withdrawal rates for each given age range, according to the Survey of Consumer Finances.

Using these assumptions, the average IRA with no leakage was assumed to have a balance of $110,000 at age 60 -- while one with leakages posted a balance of $85,000, a 23% shortfall. That's $25,000 less.

Put the $69,000 from the 401(k) and the $25,000 from the IRA together, and you get the aforementioned $94,000 shortfall.

Is it really this bad?In reality, the average nest egg balance is far less than these assumptions project. That's in part because we aren't as good at saving as the hypothetical person, and because we failed to take into consideration the effect of fees for our investments.

Whether or not these trade-offs -- getting money now in return for less money in the future -- are worth it is an entirely personal question based on your value system.

That being said, the takeaway is clear: if you raid your retirement account for $1 today, you're losing far more than that -- even after adjusting for inflation -- when you decide to retire.

The article The $94,000 Mistake the Average American Family Makes in Saving for Retirement originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.