The 3 Dividend Stocks You'll Wish You'd Bought 10 Years From Now

Investing in dividend stocks can be a great wealth building tool, but it is the epitome of investing for the long term. Re-investing one's dividend payments can turn mediocre annual returns into double-digit annual gains if you invest in a stock and hold it for decades at a time.

Of course, the ideal way to get great results out of this kind of investing strategy is to buy exemplary companies that will have the ability to consistently raise their dividends for a decade or more. So we asked three of our Motley Fool investors to each highlight a stock they think fits this description. Here's why they picked Magellan Midstream Partners (NYSE: MMP), Marathon Petroleum (NYSE: MPC), and Universal Display Corporation (NASDAQ: OLED)

Low risk, moderate growth, high yield

John Bromels (Magellan Midstream Partners): When looking for a great dividend stock, it helps to not only look for high yield, but also low risk and reasonable capacity for price appreciation. And master limited partnership (MLP) Magellan Midstream Partners checks all those boxes.

Low risk? Check. Not only did it post a healthy 1.2 times coverage in 2017, but it is known for its conservative management style and has a balance sheet that's among the best in the industry. That said, owning an MLP isn't for everyone thanks to some complex tax rules; be sure to do your research before you buy.

High yield? Check. Its current yield of 5.7% may be small compared to some other MLPs, but it blows away most stock dividends. And that yield may creep even higher over time, since the partnership's distribution -- the MLP version of a dividend -- is expected to grow by 8% in 2018, replicating its 2017 distribution increase.

Moderate price growth? Check. Over the past five years, the company's unit price -- MLP-speak for share price -- has appreciated by more than 25%, even as many of its peers' have sunk by the same amount, or more.

Add to all this the company's long history of increasing its distribution nearly every quarter since going public in 2001 -- with the only exceptions during the 2009 financial crisis -- and you get a solid choice for continued outperformance.

Rewarding shareholders the best way it can

Tyler Crowe (Marathon Petroleum): Look, I get it, the oil refining business isn't the fastest growing business out there. In fact, you could argue that it is one of the slowest growing businesses in America (total refining capacity in the U.S. has barely changed in the past 30 years). So it's not as though Marathon Petroleum is rolling out massive new refineries and about to have an explosive growth phase. What it is going to do, though, is invest in a few smaller growth avenues and give the rest back to shareholders.

Chances are, we aren't going to see petroleum product consumption increase that much in the upcoming years thanks to increased vehicle efficiency and growth in electric vehicles. So the refining business isn't going to see much growth. It's Marathon's other business segments -- its retail filling stations and its investment in midstream pipeline and processing MLP MPLX LP that are driving the company. That's why even though these two businesses make up about 47% of operating income, management has committed 73% of its capital spending to grow them.

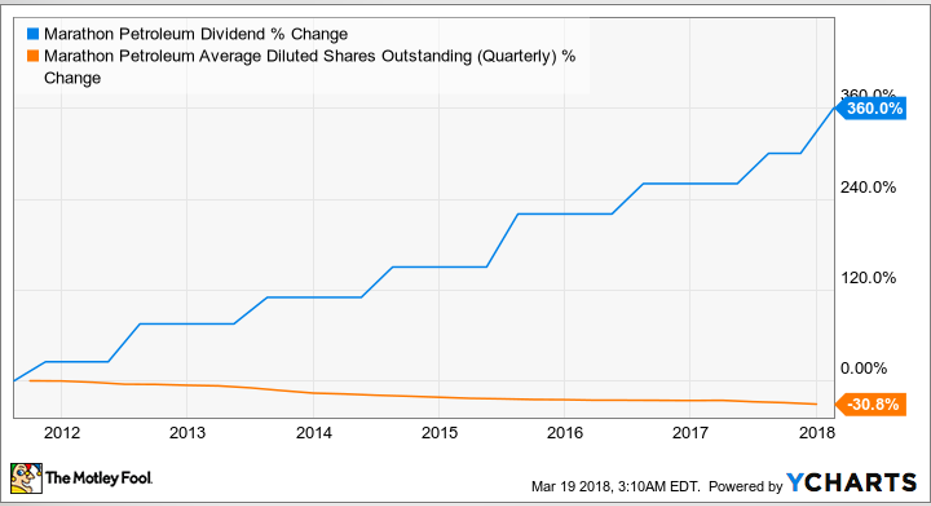

Since its largest cash-generating business doesn't require a lot of capital, that means management can return gobs of cash back to its shareholders in the form of generous dividends and share repurchases. Ever since the company went public back in 2011, management has already reduced its share count by 30% and more than tripled its dividend.

If management can continue this game plan of growing its non-refining business segments while giving the rest back to shareholders in the form of repurchases and increasing dividends, then an investment in Marathon Petroleum today could look pretty good a decade from now.

The future looks bright

Brian Feroldi (Universal Display Corporation): With a current dividend yield of just 0.2% you might be scratching your head at why I think that Universal Display is a great dividend stock to own for the next 10 years. However, I'm not interested in stock because of what its yield is today; instead, I'm excited about where the company's dividend and share price could land in the future.

Universal Display is a research company with a focus on organic light-emitting diode (OLED) technology. OLED boasts several advantages over liquid-crystal display (LCD) and light-emitting diode (LED) that has been driving higher adoption for years (OLED screens are thinner, lighter, more flexible, and consume less energy). Major screen manufacturers like Samsung and LG Display license Universal Display's technology and also purchase raw materials from it to churn out OLED products that are used in a variety of electronics.

While high costs have historically prevented OLED technology from being competitive with LCDs and LEDs there are ample signs that this is no longer the case. Apple recently joined the OLED party with the launch of the iPhone X and will likely use the technology in future versions of its products. Other manufacturers are following suit, so it is likely just a matter of time before all smartphones, TVs, tablets, and lighting products make the switch.

Wall Street currently projects that the gradual move to OLED will drive Universal Display's profits up 35% annually over the next five years. If that forecast is anywhere close to accurate then the company's dividend and share price will both be much, much higher in 10 years' time.

10 stocks we like better than Universal DisplayWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Universal Display wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of March 5, 2018

Brian Feroldi owns shares of Apple and Universal Display. John Bromels owns shares of Apple. Tyler Crowe owns shares of Apple, Magellan Midstream Partners, and MPLX LP. The Motley Fool owns shares of and recommends Apple and Universal Display. The Motley Fool has the following options: long January 2020 $150 calls on Apple and short January 2020 $155 calls on Apple. The Motley Fool recommends Magellan Midstream Partners. The Motley Fool has a disclosure policy.