Social Security COLAs Are Being Left in the Dust by Medical Care Inflation, and Seniors Should Be Upset

Image source: Getty Images.

Three weeks ago seniors received the news they've been waiting for all year from the Social Security Administration (SSA) -- whether they'd get a raise in 2017.

With the release of the Social Security Fact Sheet for 2017, seniors receiving Social Security income now know they'll be receiving a cost-of-living adjustment (COLA) of 0.3% in the upcoming year. Since the average retired worker took home $1,350.64 per month as of the August 2016 snapshot from the SSA, this works out to about a $4.05 per month increase for the typical senior. That's not exactly something to write home about, but it's certainly better than the 0% COLAs seniors were subjected to in 2009, 2010, and 2015.

How Social Security adjusts for inflation

Social Security's COLA is derived from movement in the Consumer Price Index for Urban Wage Earners and Clerical Workers, or more simply the CPI-W. The CPI-W takes into account what goods and services working class Americans buy and quantifies the level of inflation or deflation seen in those products or services on a year-to-year and month-to-month basis.

Social Security's COLA is determined by comparing the average CPI-W from the third quarter of the previous year (which serves as the baseline figure) to the average CPI-W from the third quarter of the current year. Any increase is rounded to the nearest tenth of a percent and constitutes the COLA that seniors receive beginning on Jan. 1 of the following year. A decline in prices (i.e., deflation) means no COLA since Social Security benefits cannot fall.

Image source: U.S. Bureau of Labor Statistics.

The CPI-W is believed to closely represent the inflation that a majority of Americans are dealing with. However, it may not accurately reflect the spending habits of retired workers, who make up two-thirds of all Social Security beneficiaries.

Compared to another measure, known as the Consumer Price Index for the Elderly, or CPI-E, the CPI-W tends to de-emphasize the cost of housing and medical care compared to what seniors typically pay each month for these categories. In fact, medical care expenditures as a percentage of monthly income are double for seniors what they are for the average working class American based on a Bureau of Labor Statistics (BLS) comparison of the CPI-W and CPI-E from Dec. 2011. The CPI-W also overemphasizes (compared to the CPI-E) expenditures for food, apparel, education, and entertainment. The result is that seniors are seeing their purchasing power decline as select costs rise at a much quicker pace than their Social Security benefits.

Seniors are getting hosed by medical care inflation

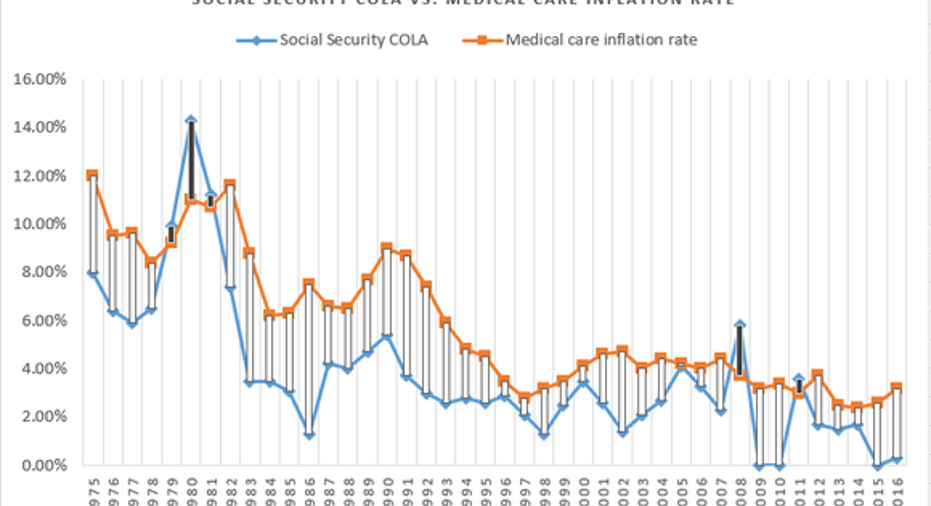

In particular, seniors are seeing their Social Security "raises" get left in the dust by medical care inflation, and they should rightly be upset by this fact. Below you'll see a chart based on data from the BLS and SSA that compares the medical care inflation rate since 1975 to Social Security's COLA.

Chart by author. Data source: Bureau of Labor Statistics, Social Security Administration. 2016 medical care inflation rate based on first-half BLS estimate.

As you can see, the difference between the two is night and day, especially over the past decade. Since 2005, Social Security benefits have risen by a cumulative 27%. This takes into account the aforementioned three years when there was no COLA. By comparison, medical care inflation since 2005 has jumped by 48.6%, which includes an estimate of 3.2% inflation through the first half of 2016. In fact, Social Security's COLA has outpaced medical care inflation in just a handful of years over the past two decades, as represented by the black lines on the above chart. Brand-name and specialty drug inflation, along with higher procedure service costs, are the most likely culprits pushing medical care inflation higher.

The argument for some seniors is that if the CPI-E were being used instead of the CPI-W, this 21.6% gap since 2005 would be significantly smaller, presumably allowing seniors to spend less of their monthly benefits on medical care expenses and putting them on better financial footing. Since the CPI-E focuses only on households with persons ages 62 and up, and Social Security benefits are being paid primarily to seniors ages 62 and up, moving the SSA's COLA measure to the CPI-E could have some merit.

The CPI-E may not offer a perfect solution

Unfortunately, nothing is ever this cut and dry when it comes to Social Security. While the CPI-E could possibly close the gap between medical care inflation and Social Security's COLA, it isn't a perfect solution.

Image source: Getty Images.

For instance, even though seniors make up the majority of Social Security recipients, the CPI-W may still be a better measure of broader inflation since it includes tens of millions of additional households in its formula than the CPI-E. As of 2014, the CPI-W included 156 million people, whereas the U.S. Census Bureau pegged the elderly population at just over 43 million in 2012. That's a big difference, and it's enough to persuade lawmakers to stick with the more encompassing measure of inflation, the CPI-W.

Additionally, the CPI-E doesn't factor in Medicare Part A expenses. Part A is the component of Medicare that covers inpatient surgical procedures and certain types of long-term skilled nursing care. Without these costs being factored into the equation, it's likely that the CPI-E would still trail the true rate of medical care inflation, even if Congress chose to make the switch from the CPI-W to the CPI-E.

There's no simple solution to fix Social Security's shortcomings when it comes to medical care inflation, which makes it all the more imperative that retirees stick to a detailed monthly budget to control their expenses during their golden years, and that pre-retirees ensure they have adequate sources of income beyond just Social Security when they retire.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

Sean Williamshas no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen nameTMFUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.

The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.