Self-Driving Cars Will Drive 1 Stock Higher and Cripple Another

Investors sifting through the automotive sector for stocks poised to thrive over the coming decades as the industry evolves toward driverless vehicles don't have many options. Arguably, the best autonomous-vehicle pure play was Mobileye, which develops camera-based vehicle vision systems for a multitude of major automakers, but the company recently agreed to be acquired by Intel.

For those looking at auto industry suppliers with their eyes on the future, here is one stock to seriously consider and one company that could face a slow death thanks to the rise of autonomous vehicles.

Turning into a loser?

Axalta Coating Systems (NYSE: AXTA) is coming off a decent first quarter, but you should likely avoid this stock over the long term. In 2016, this vehicle coatings manufacturer generated 59% of its sales from its performance coatings segment, which sells the finishes used at body shops, independent shops and light-vehicle dealerships, among other areas. The other 41% of its sales were generated from its transportation coatings segment, which focuses on OEMs, such as the Detroit automakers.

Here's the long-term problem for Axalta: Because between Axalta's two business segments roughly 60%of its business is reliant on cars needing refinished coats after crashes, its future is in jeopardy as the industry is marching toward driverless vehicles, which are expected to steeply reduce the number of car accidents. And that isn't a headwind that will turn up suddenly in 20 years once most vehicles become completely autonomous; it's a headwind that will have an immediate, albeit slowly increasing, negative impact.Vehicles are already being loaded with technology to make driving safer, such as lane control, blind-spot sensors, and driver assist.

Image source: Getty Images.

Another headwind that Axalta faces is simply the natural progression of driver behavior in larger markets all over the world. As larger markets become more developed, their car accident rates tend to consistently decline relative to the population, which would put pressure on the company's top-line growth in critical markets.Investors also should consider the behavior of global automakers broadly. Generally speaking, they're continuing to cut costs by consolidating their business among suppliers, giving the OEMs more leverage on pricing. It's already a common practice for OEMs to bring in multiple companies for a product, as a car often needs multiple coatings, to increase competition.

This company has a healthy business at the moment, and it has been around for over a century. However, the auto industry is poised to change more in the next two decades than it has over the past century, and businesses like Axalta will need to adapt or face a slow death from the shifts wrought by autonomous vehicles.

Turning into a winner?

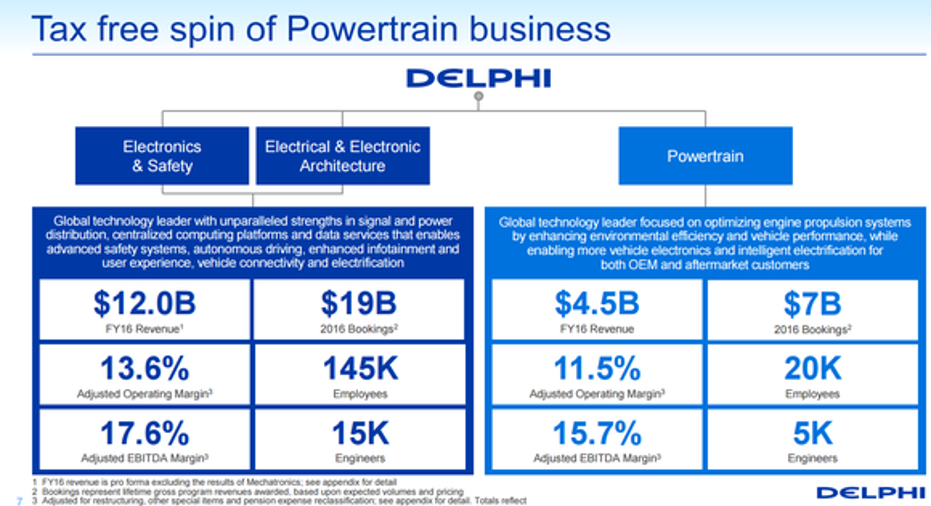

Delphi Automotive (NYSE: DLPH) gave investors a lesson in addition by subtraction this week after it announced it would be spinning off its powertrain business as a completely separate, publicly traded company -- a move that helped drive Delphi's stock more than 10% higher on the day it was announced.

In the press release regarding the plan, President and CEO Kevin Clark said:

Image source: Delphi Automotive's May 3, 2017, spin-off presentation.

While the powertrain business was a valuable one for Delphi, this spinoff will enable management of the remaining company to better focus on a future of driverless vehicles. This isn't a wildly new strategy for Delphi, either, as the company has been shedding its lower-margin segments for years. Since mid-2015, it has divested itself of its thermal, reception systems, and mechatronics businesses.

Once its powertrain business is spun off, it will leave a company focused on end-to-end solutions for smart mobility and autonomous driving. Delphi will focus on the "brains" of the vehicle, which will include active safety and autonomous systems, data and services, and infotainment systems; it'll also focus on the "nervous system," which includes power and signal distribution, sensing, and over-the-air (OTA) and vehicle connectivity.

With this spinoff, Delphi is going to increasingly become a popular investment for those looking to profit from the coming growth in autonomous vehicles and smart mobility. Management also estimates that between additional architecture, sensors, radar/lidar, and embedded controls and algorithms, as much as $5,000 content per vehicle could be added. That's a valuable chunk of a high-margin business, and Delphi seems poised to earn its fair share.

10 stocks we like better than Delphi AutomotiveWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Delphi Automotive wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of May 1, 2017

Daniel Miller has no position in any stocks mentioned. The Motley Fool recommends Intel. The Motley Fool has a disclosure policy.