Phillips 66 Has Bought Back 10 Million Shares So Far in 2016. Should Investors Be Happy?

Do Phillips 66's share buybacks measure up? Probably so. Image source: Getty Images.

When a public company generates a profit, it essentially has three things that it can do with that money:

- Invest it back into the business (growth, acquisitions, or improvements to the balance sheet).

- Pay a dividend.

- Repurchase shares.

In most cases, the first option is the one that makes the most sense. Very few companies don't have opportunities to invest in growing the business, whether it's developing new products, geographical expansion, or making an acquisition, putting profits back to work in ways to make even more profits is almost always the best thing to do, while paying out any leftover cash in dividends.

But in some cases -- particularly with large, well-established companies that generate very large, regular cash flows, it might also be a smart use of cash to repurchase shares. And it's pretty clear that the management of energy giantPhillips 66(NYSE: PSX) thinks share buybacks are a good thing. Through the first three quarters of 2016, the company has spent $812 million to repurchase 10.1 million shares of stock.

Should investors be happy about the company's aggressive share buybacks? Probably so, with the caveat that the company has taken on some debt to support all of its spending. Let's take a closer look at what the company has done, and what it means for shareholders.

An aggressive buyer of shares since going public

Since being spun out of its former parent company, ConocoPhillips(NYSE: COP), in 2012, Phillips 66 management has been an aggressive, regular buyer of its own stock. Since the inception of its share-buyback program in 2012, the company has repurchased 102.6 million shares of stock at a $7.2 billion cost. When we include a deal with (now largest shareholder)Berkshire Hathaway(NYSE: BRK-B) to exchange $1 billion in shares for part of its chemical business, and that's a 17% reduction in shares outstanding:

PSX Shares Outstanding data by YCharts

That works out to an average of $70.18 per share the company has paid, about a 20% discount to recent share prices.

A closer look at what Phillips 66 does with its cash

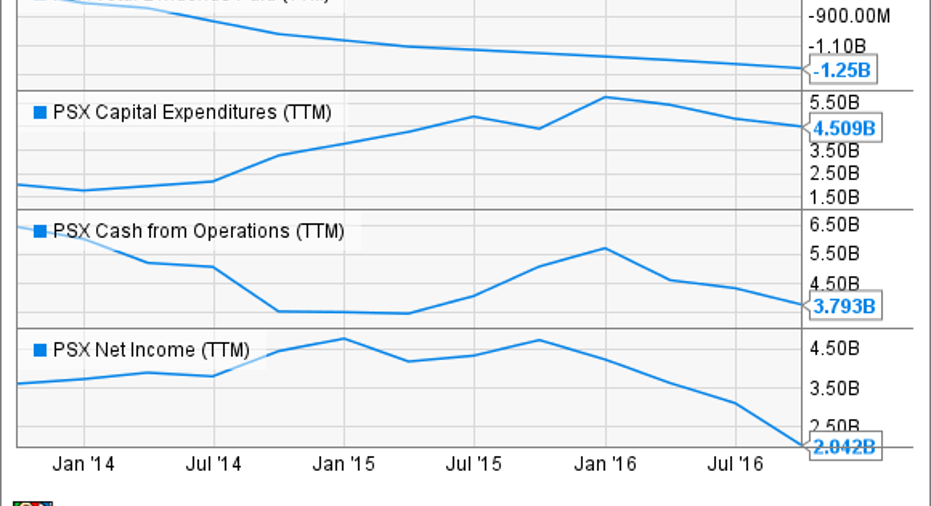

Phillips 66 certainly qualifies as a company with very large, consistent cash flows. Its primary businesses are oil refining and marketing of refined products, midstream oil and gas operations, and petrochemical manufacturing. These segments all have significant and fairly stable industrial and commercial demand, allowing Phillips 66 and its subsidiaries to produce a large amount of cash from operations:

PSX Cash from Operations (TTM) data by YCharts

And the company uses that cash for all three of the things noted at the top of this article. So far in 2016, Phillips 66 has paid $954 million in dividends, the aforementioned $812 million in share buybacks, and $2 billion on capital expenditures.So that's $3.8 billion spent, while the company has generated only $1.39 billion in net income, and $2.3 billion in operating cash flows.

So far in 2016, Phillips 66 has spent more money than it has made. That was also the case in both 2015 and 2014, with the company using about $2.3 billion more in cash than it generated, while also taking on nearly $3 billion in additional debt over that time.

Bottom line: Phillips 66 has historically spent more on capex, dividends, and share buybacks than it generates in profits or cash flows:

PSX Total Dividends Paid (TTM) data by YCharts

On balance, these share buybacks should make you happy -- with this caveat

There's no getting around the reality that Phillips 66's use of debt has allowed it to simultaneously invest in growing its midstream business, pay (and increase) a nice dividend, and aggressively repurchase shares, so it's not worth arguing whether the debt is technically funding capital growth, or propping up the dividend and share-repurchase program.

What really matters is whether management is pulling the right levers to generate a solid return on that spending. If the capital projects generate a better return than the cost of the capital, then the debt is worth it. And considering that Phillips 66 pays only about 3.5% on its long-term debt, the bar is relatively low to generate incremental per-share earnings growth from those investments.

When it comes to buybacks, the biggest measure of success is this: Did the company buy them back at a discount? So far in 2016, Phillips 66 has averaged $80.39 per share on the 10.1 million shares it has repurchased. That's about 8% below recent prices and should prove to be good value over time.

The caveat: The true "win or lose" result of these buybacks won't be apparent until we can measure the gains from the company's growth investments. If those capital projects don't deliver earnings growth that more than covers the cost of the debt associated with them, then the company would have been better off avoiding the debt and not repurchasing the stock, even factoring in the discount paid. Historically, Phillips 66 management has done an excellent job with capital allocation, but only time will tell if that remains the case.

10 stocks we like better than Phillips 66 When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Phillips 66 wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

Jason Hall owns shares of Phillips 66. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.