PDL BioPharma, Inc. Is Off 10% in 2016, and This Is a Big Reason Why

Image source: Getty Images.

What: Shares of PDL BioPharma , a small-cap biotech company that invests in patents and royalty-based biotechnology and pharmaceutical assets, has lost 10% of its value so far this year, according to data from S&P Global Market Intelligence. The reason for the plunge can be traced to one important decision in early February.

So what: This decision relates to PDL BioPharma's press release on Feb. 1, which stated that its management team was shifting its strategy on dividends to a quarter-by-quarter basis in an effort to preserve capital and open up long-term growth opportunities. In plainer English, PDL BioPharma slashed its dividend from $0.15 to just $0.05 per quarter. Additionally, the language of its press release suggests that its dividend will be reviewed quarterly, and is henceforth no longer a guarantee. This was clearly unwelcome news for a company that had, up to this point, been yielding well in excess of 10%.

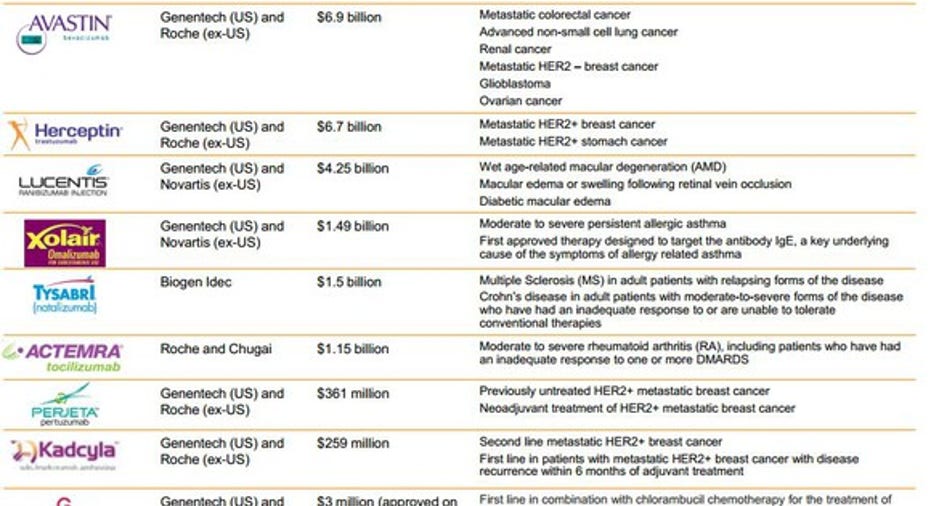

Why the dividend cut, you ask? PDL BioPharma's patents and royalty assets suffer the same fate as branded drugs do for drugmakers: They have a finite shelf life. More than 80% of PDL BioPharma's revenue in recent years was derived from its Queen et al. patents, which allowed it to reap royalties from blockbuster drugs like Avastin, Herceptin, Lucentis, and Tysabri, to name a few. However, PDL's Queen patents expired in Dec. 2014. The good news is that PDL BioPharma still had about a little over a year's worth of shelf life to generate strong revenue and cash flow beyond Dec. 2014 thanks to warehousing of these drugs. However, that revenue train has now vanished.

After recording $590.5 million in revenue last year, PDL's top line is expected to dip to $173 million in 2016 and just $68 million in 2017. Furthermore, profit per share is expected to plummet from the $2.04 it reported in 2015 to an estimated $0.06 per share in 2017.

Image source: PDL BioPharma.

Now what: On one hand, PDL BioPharma's minimal overhead is a positive for the company. Since it doesn't deal with the usually high expenses of research and development, it only employs a relatively small staff. This means it doesn't need an exceptionally high amount of sales to turn a profit. Unfortunately, there simply isn't an immediate fix for losing its Queen et al. patent revenue.

In May, PDL BioPharma announced an equity investment totaling 88% in Noden Pharma DAC, a privately held company that recently executed a purchasing agreement with Novartis for worldwide rights to Tektuma and Tektuma HCT (which is known as Rasilez and Rasilez HCT outside the U.S.). Per the press release, this drug targets hypertension, and 2015 sales totaled north of $150 million. Although this is a start, it's still a far cry from the Queen patent revenue shareholders have been used to.

My guess is that PDL's quarterly dividend will completely disappear or perhaps shrink to around $0.01 per share beginning in the upcoming quarter and thereafter. As a royalty company, shareholders expect a handsome income reward. But with PDL's bread-and-butter patents off the table, they're no longer going to receive an above-market dividend yield. My suggestion would be to keep your distance form PDL BioPharma until we see a marked resurgence in its top line and profits.

The article PDL BioPharma, Inc. Is Off 10% in 2016, and This Is a Big Reason Why originally appeared on Fool.com.

Sean Williamshas no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen nameTMFUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.