Paycom Software's Incredible Performance in 4 Charts

Paycom Software (NYSE: PAYC), the provider of workforce management and payroll software, reported its fourth-quarter and full-year 2016 earnings in February. Investors found plenty to celebrate, including yearly top-line gains of 47% and net-income growth of 109%, sending Paycom's stock to new all-time highs. With 2016 now in the books, let's take a look at just how remarkable the company's performance has been over the last five years.

Image source: Paycom Software.

Revenue keeps growing like a weed

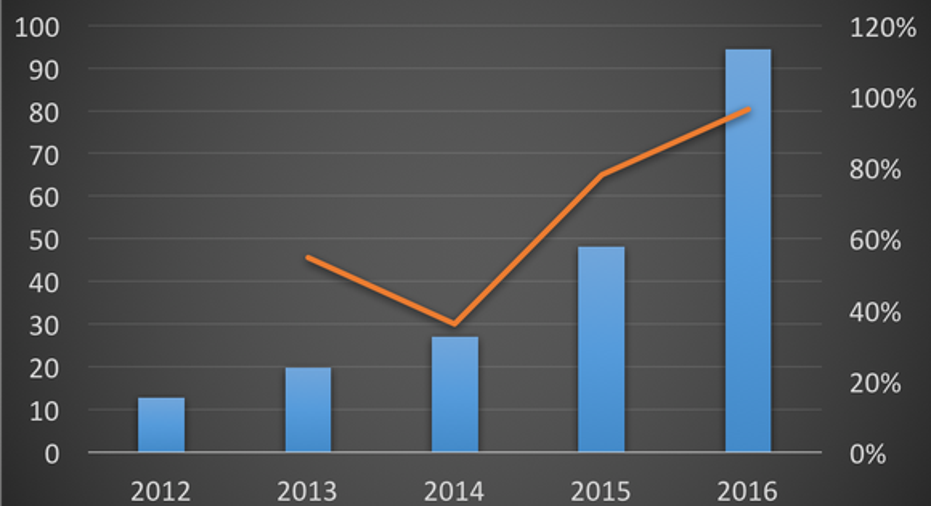

Data from Paycom Software 10-K. Chart by author.

Paycom's revenue growth is a thing of beauty, rising from $76.8 million in 2012 to $329.14 million in 2016. For the past four fiscal years, yearly revenue growth has been above 40%. While rates like that may not be sustainable for a whole lot longer, the company has guided for 2017 revenue of $422 million to $424 million, the midpoint of which represents 29% growth. And management has stated that they continue to target yearly top-line growth of 30% plus.

Retention rates -- the most boring chart in the world

Data from Paycom Software 10-K. Chart by author.

While the chart above may not be very exciting to look at, that's just how Paycom investors should want it. The company's revenue retention rate -- which is the percentage of revenue retained from existing clients -- is a good indicator of overall client satisfaction and a reliable predictor of future revenue. Paycom's retention rate has held steady at 91% for five consecutive years, and the company claims that it continues to lead the industry on this important measure.

Adjusted EBITDA margins have come a long way

Data from Paycom Software 10-K. Chart by author.

Adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) margin measures a company's operating profitability as a percentage of its revenue. As you can see, Paycom's adjusted EBITDA margin has risen fairly dramatically from 16.7% in 2012 to just under 29% in 2016. And there is likely even more room for improvement, as management has stated they are targeting long-term adjusted EBITDA margins of 30% to 33%. That said, the company is prioritizing top-line growth in the near term, which will boost expenses for sales, marketing and R&D in 2017. As a result of those strategic investments, management has issued guidance for adjusted EBITDA margin of 27% in 2017.

Adjusted EBITDA growth looks quite healthy

Data from Paycom Software 10-K. Chart by author.

In terms of the bottom line, Paycom's net income has grown at triple-digit annual growth rates for each of the past three years. However, since the company just turned profitable in 2014, the growth rate trend line doesn't make for a good chart. Instead, check out Paycom's adjusted EBITDA. You can see that this measure of "top-line" earnings grew from $12.83 million in 2012 to $94.46 million in 2016, with annual growth rates that exceeded 50% in three of the past four years. However, in line with my previous comments about 2017 being a kind of investment year, the company also issued adjusted EBITDA guidance of $113 million to $115 million, reflecting lower annual growth of 21% at the midpoint.

Paycom's business is generating solid results on the top line, the bottom line, and everywhere in between. And it hasn't been just one or two great quarters -- the company has been exceeding expectations now for several years running. Although 2017 may bring slightly lower margins and earnings growth, the company's continued strong top-line expansion and steady retention rates make me think Paycom's future will look a lot like its past.

10 stocks we like better than Grupo Aeroportuario del PacificoWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and Grupo Aeroportuario del Pacifico wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017.

Andy Gould owns shares of Paycom Software. Andy Gould has the following options: short May 2017 $50 puts on Paycom Software. The Motley Fool owns shares of and recommends Paycom Software. The Motley Fool has a disclosure policy.