Palo Alto Networks' $500 Million Buyback Won't Help Investors

Shares of Palo Alto Networks (NYSE: PANW) fell 7% on Aug. 31 after the cybersecurity firm followed up a decent fourth quarter report with weak guidance for the first quarter. Revenue rose 41% annually to $400.8 million, beating estimates by $11.1 million. However, that represented a slowdown from 48% growth in the previous quarter and 59% growth in the prior year quarter. Its non-GAAP net income rose 85% to $46.2 million, or $0.50 per share, which merely matched analyst expectations.

Image source: Getty Images.

But for the first quarter, Palo Alto sees revenues rising 33%-35% annually, which would represent its slowest growth rate since its public debut four years ago. Non-GAAP earnings are expected to rise 46%-51% annually, which also represents a dramatic slowdown in bottom line growth. These numbers indicate that Palo Alto is still growing, but perhaps not rapidly enough to justify its pricey P/S ratio of 8.6.

As a consolation prize to investors who endured the stock's 25% year-to-date decline, Palo Alto authorized a $500 million buyback plan which will last through Aug. 31, 2018. However, those buybacks are likely aimed at offsetting the company's massive stock dilution problem instead of helping out investors. Here's why investors should be upset with this strategy.

Palo Alto's stock-based compensation problem

Palo Alto's stock-based compensation (SBC) expenses rose 64% annually to $112.7 million last quarter, gobbling up 28% of the company's revenues. After factoring in those costs and other expenses, the company's GAAP net loss actually widened from $46 million a year ago to $54.5 million.

Palo Alto claims that its SBC is comparable to that of its industry peers, but that's simply not the case. Here's a comparison between Palo Alto's SBC and compensation at Check Point Software, Fortinet, FireEye (NASDAQ: FEYE), and CyberArk in their most recent quarters.

|

Palo Alto |

Check Point |

Fortinet |

FireEye |

CyberArk |

|

|

YOY SBC change |

64% |

17% |

46% |

2% |

248% |

|

As % of revenues |

28% |

5% |

19% |

33% |

8% |

Stock-based compensation (SBC) expenses. YOY = year-over-year. Source: Quarterly reports.

The only company with a comparable SBC ratio as Palo Alto's is FireEye, which recently announced that it would lay off staff to reduce its annual operating expenses.

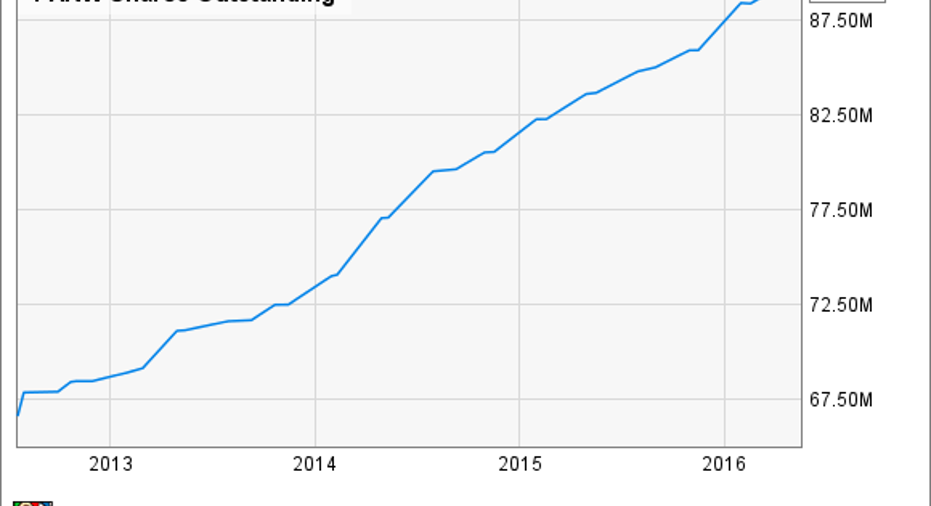

More stock bonuses, more outstanding shares

As I mentioned in a previous article, Palo Alto has done very little to narrow its GAAP losses. Instead, it asks investors and analysts to focus on the non-GAAP results, and CEO Mark McLaughlin notes that its liberal useof stock bonuses is necessary to retain talent in the "very, very competitive talent environment" of Silicon Valley. But that also means issuing a lot of new shares to pay employees.

Source:YCharts

As a result, Palo Alto must buy back stock to offset dilution. In previous years, Palo Alto's cash position wasn't strong enough to launch a major buyback program. It also didn't seem eager to take on more debt to finance buybacks, even with interest rates near historic lows.

But the company finished fiscal 2016 with $734.4 million in cash and equivalents -- a 95% increase from the previous year. Its full-year free cash flow also rose 85% to $585.6 million. That cash growth apparently gave Palo Alto the confidence to approve a $500 million buyback, which would be good for buying back nearly 4 million shares at current prices.

There are better ways to spend $500 million...

Instead of spending half a billion dollars on its own shares, it makes more sense for Palo Alto to gradually spend more cash than stock on employee salaries. This would narrow the widening gap between its non-GAAP and GAAP earnings, show that it's serious about eventually turning a profit, and throttle its soaring share count. Instead, Palo Alto's buyback will simply reduce its free cash flow, continue allowing it to rely heavily on big stock bonuses, and let it potentially overpay for its own shares.

Since Palo Alto faces tough competition in the firewall market from Check Point, Fortinet, and even Cisco, it seems wiser to set that cash aside for acquisitions to widen its competitive moat. Buying other companies is probably the only way Palo Alto can keep posting 30%-40% sales growth every quarter.

Therefore, investors shouldn't celebrate Palo Alto's big buyback. Instead, it indicates that the company isn't worried about narrowing its GAAP losses, and is more concerned with offsetting dilution from SBC than boosting shareholder value.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Leo Sun owns shares of Cisco Systems and CyberArk Software. The Motley Fool owns shares of and recommends Check Point Software Technologies and FireEye. The Motley Fool recommends Cisco Systems, CyberArk Software, and Palo Alto Networks. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.