Mining Gold Stocks: Is Barrick Gold More Precious Than Its Competition?

Image source: Getty Images.

Barrick Gold (NYSE: ABX) is a leader among gold-mining companies and the largest by market capitalization, but that's not reason enough to choose it as an investment. Let's take a look at some of its peers and evaluate its position among them.

The roundup

A pure-play on gold,Goldcorp(NYSE: GG)differs from both Barrick Gold in that it only operates mines in the Americas: four in Canada, two in Mexico, and four in Central and South America.

ABX Market Cap data by YCharts.

Like Goldcorp,Kinross Gold (NYSE: KGC) is also a pure-play on gold. Operating five mines in the Americas, Kinross Gold also maintains two mines in each West Africa and Russia as well.

Operating 10 mines on five continents -- North America, South America, Africa, Asia, and Australia --Newmont Mining (NYSE: NEM) is the only gold company included on the S&P 500 Index. The company, which is the closest to Barrick Gold by market cap, is also involved in the mining of copper.

Rounding out the peer group, Yamana Gold (NYSE: AUY) operates two mines in North America, where it has one in each Canada and Mexico; moreover, the company operates seven mines throughout South America. Unique in this peer group, Yamana Gold maintainsthe production of three metals: gold, silver, and copper.

Proving their mettle

At first blush, investors considering the gold industry may be attracted to Goldcorp, which currently sports the most attractive dividend yield among the peer group, or maybe Yamana Gold, which has a dividend yield greater than Barrick Gold. But the yield is only part of the story.

| Company | Dividend Yield | Payout Ratio |

|---|---|---|

| Goldcorp | 1.29% | (4.28%) |

| Yamana Gold | 0.78% | (2.47%) |

| Barrick Gold | 0.40% | (3.07%) |

| Newmont Mining | 0.23% | 140% |

Data source: YCharts. Both metrics on a trailing-12-month basis.

Absent from this list is Kinross Gold, which suspended its dividend in 2013. This raises an important point when considering dividend stocks: Is the company's dividend sustainable? Kinross Gold found that it wasn't, and it wouldn't be a surprise if other companies followed suit.

With a payout ratio above 100%, Newmont isthe only company reporting positive net income, but it's paying it all out -- then 40% more on top of it -- to shareholders. On the other hand, Goldcorp, Yamana Gold, and Barrick Gold all sport negative payout ratios. In other words, they're reportinglosseson their bottom lines, yet they continue to return cash to shareholders -- not a recipe for long-term success.

Think quick...and current

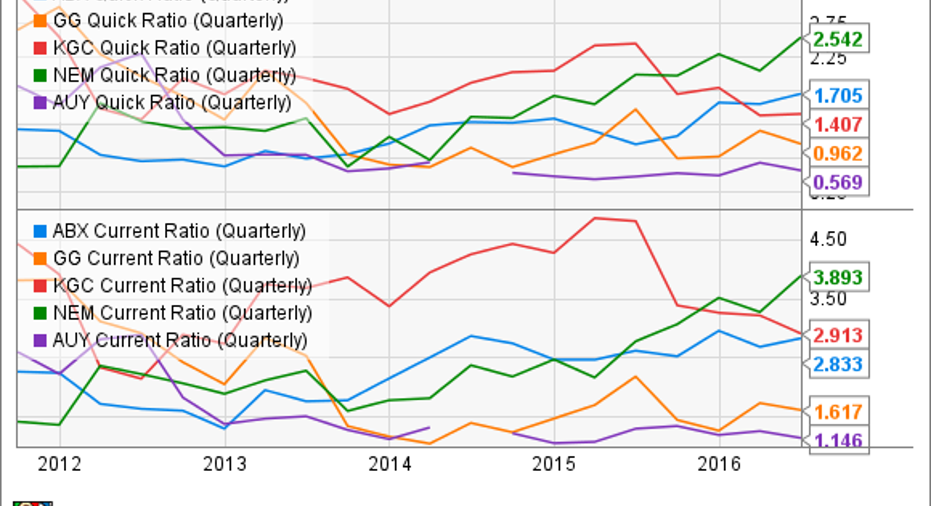

When evaluating mining companies, it's imperative to consider their liquidity. Producing millions of ounces of gold in a year doesn't come cheap, so mining companies rely heavily on debt to keep their operations running. But in order to service these massive debt loads, companies must deftly manage their liquidity. Finding millions of ounces of buried gold means little if the company is, likewise, finding itself buried under a mountain of debt.

Fortunately, there are two metrics we can use to assess a company's liquidity: the quick ratio and the current ratio. Used to calculate a company's ability to pay short-term obligations, the quick ratio subtracts the current inventories from a company's assets and divides it by the current liabilities. Adding back inventories to the equation, we arrive at the current ratio, which provides a sense of a company's ability to meet both short-term and long-term obligations. Suggesting a healthy position in terms of liquidity, a ratio over 1.0 means the company has more than $1.00 in assets for each $1.00 of debt.

ABX Quick Ratio (Quarterly) data by YCharts.

When we calculate the quick and current ratios, it becomes exceedingly clear that Newmont Mining is in the healthiest position liquidity-wise. These are far from the most important metrics in evaluating a stock -- there is no single, magic metric -- but they are valuable tools. And they may certainly pique the interest of more conservative investors. Newmont Mining's exceptional liquidity shouldn't subtract from Barrick Gold's position, which is also quite strong.In fact, kudos to management all around. Each company in the peer group appears to be in a safe position -- except for a question about Yamana Gold's quick ratio -- regarding liquidity.

What do you get in return?

Whether it's raising equity or issuing debt, management must demonstrate it can successfully use the tools at its disposal to grow the business and provide returns to investors. Although the gold industry has had its share of challenges over the past five years -- the price of gold is down nearly 17% -- it's still a worthwhile effort to look at the returns on equity and assets to ascertain how well managements have performed.

ABX Return on Equity (TTM) data by YCharts.

As it did regarding the liquidity ratios, Newmont Mining stands out prominently from its peers, being the only one to sport positive returns on both equity and assets. At the other end of the spectrum, Barrick Gold is the least successful among its peers at making use of equity to benefit shareholders.

The takeaway

Emerging as a leader in the gold mining industry doesn't come easily, and there are many reasons to strongly consider an investment in Barrick Gold. But one would be remiss to not also strongly consider Newmont Mining -- a company that, at a cursory glance, appears to be in better financial health and superior to its peers at making use of assets and shareholders' equity.

Furthermore, Kinross Gold, Goldcorp, and Yamana Gold also warrant consideration. Any interested investor would certainly need to dig deeper and mine the financial statements.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early, in-the-know investors! To be one of them, just click here.

Scott Levine has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.