Just 1 in 10 Seniors Is Making This Social Security Move -- And That's Worrisome

Image source: Pixabay.

Today, more than 60 million Americans count on Social Security checks each month, and about two-thirds of those recipients are retired workers who'd likely struggle without the financial foundation that Social Security income provides.

Based on a survey conducted in 2015 by national pollster Gallup, today's retirees rely heavily on Social Security to meet their monthly expenses. A whopping 59% of retired seniors responded that Social Security accounts for a "major source" of income, and another 31% affirmed that it's a "minor source" of retirement income. No matter how we rearrange the puzzle pieces, about 90% of seniors could have trouble meeting their monthly expenses without Social Security.

We saw a similar pattern when Gallup questioned pre-retirees on their expected reliance on the Social Security program. Combined, 84% of pre-retirees, or essentially six in seven, believe Social Security will be a "major source" of income (36%) or a "minor source" (48%) come retirement. In fact, over the past decade the number of pre-retirees expected to rely on Social Security as a major source of income has risen by 11% (25% to 36%).

Despite being such a critical financial foundation for most seniors, Social Security's long-term future is in flux. The latest Board of Trustees report suggests the program's excess cash reserves could be completely depleted by 2034, necessitating up to a 21% reduction in benefits to extend the life of the program through 2089. This doesn't mean Social Security is insolvent or won't be there for today's workers, but it does mean the program might look a lot different two decades from now.

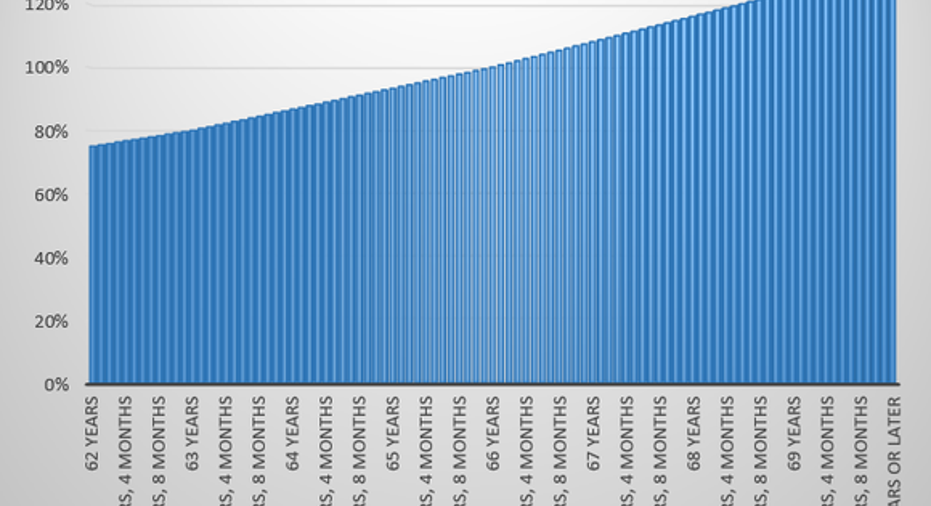

Too few seniors are making this decision -- and it's worrisome This means seniors' choice of when to file for benefits could be one of the most important decisions they make. Generally speaking, the longer a retired worker waits to file for benefits after turning 62 years old, the first age at which beneficiaries become eligible to file for benefits, the higher their benefit will be (up until age 70, when benefits max out). As you can see below, benefits increase with each successive month a senior holds off on filing for benefits, and the increases tend to average about 8% per year.

The Social Security retirement benefit schedule for people born between 1943 and 1954. Chart by author. Data source: Social Security Administration.

The magic, but dynamic, number that represents the so-called Social Security "finish line" is your full retirement age, or FRA. Your FRA is based on your birth year, and currently ranges between 65 years and 67 years. When you hit your FRA, you become eligible for 100% of your retirement benefit. If you retire prior to hitting your FRA, you'll receive a reduced rate that, based on today's retirees with birth years ranging from 1943 to 1954, could be as low as 75% of your FRA.

Conversely, waiting until after your FRA can pump up your benefits payment well beyond 100%. Retirees with an FRA of 66 years who hold off on claiming benefits until age 70 can receive a monthly benefit of up to 132% of their FRA. Yet, according to a study conducted by the Centers for Retirement Research at Boston College, just 10% of all seniors, as of 2013, were choosing a date beyond their FRA to file for Social Security benefits. That's a worrisomely low figure.

Why this is a worrisome trendThe reason this is particularly worrisome is that, based on data from the Center for Retirement Research at Boston College, more than half of seniors as of 2013 were claiming benefits before their FRA (and around a third right at their FRA). This means most beneficiaries are receiving less than 100% of the benefits they'd be due based on their income history -- even though, as noted above, more than a third of pre-retirees expect to be reliant on Social Security income in retirement. If you're going to be reliant on Social Security income, the last thing you'd want to do is minimize what the program is going to pay you monthly.

Chart by author. Data source: Centers for Retirement Research at Boston College. Data is from 2013.

There are of course understandable reasons for filing for benefits at age 62, or any age less than your FRA. For example, if you don't anticipate living into your 80s due to health reasons, then taking Social Security benefits early can be worthwhile. Also, if your retirement nest egg is in great shape with plenty to spare, and Social Security income is essentially "gravy," then using Social Security income to pay for travel or the pursuit of your passions might be a suitable move.

However, for the numerous baby boomers who are entering retirement without adequate savings, filing for benefits early could be a mistake they'll regret for the rest of their lives. While I fully understand the impetus in claiming benefits as early as possible to help with paying monthly bills and reducing your potential debts heading into retirement, filing early can also lock you into a substantially lower benefit payment for decades to come. If there's a group of individuals who should be waiting as long as possible to file for benefits, it's seniors who don't have an adequate nest egg. And according to a study from the Insured Retirement Institute, about 4-in-10 baby boomers don't have a cent saved toward their retirements.

Work more, save more might be your best option This means that individuals without an adequate nest egg should consider working well beyond the traditional retirement ages of 62 or 65, assuming their health permits. Working longer should allow you to use your wages to meet your monthly expenses, while at the same time allowing your Social Security benefit to grow.

Image source: Flickr user Scott Lewis.

Based on today's average Social Security payment of $1,345 for retired workers as of March 2016, waiting those extra four years beyond your FRA could mean an extra $430 in your pocket each month. Plus, working longer could help boost your earnings average, which the Social Security Administration uses to calculate your benefit, thus boosting your benefit even more. Finally, working more may help you save more for your retirement.

Additionally, seniors will need to learn how to live within a tight budget if they're reliant on Social Security. It's imperative they understand how their cash on hand is being spent so they can make it stretch even further. Plus, if a benefit cut is in the cards over the next two decades, as the Board of Trustees' report has implied, a budget could help seniors more easily transition to a lower income environment.

Working longer may not have been what you envisioned, but waiting to claim benefits until after your FRA is probably a smarter move than you realize.

The article Just 1 in 10 Seniors Is Making This Social Security Move -- And That's Worrisome originally appeared on Fool.com.

Sean Williamshas no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.