Is The Clorox Company Stock Too Expensive?

Image source: The Clorox Company.

The Clorox Company(NYSE: CLX) has been a great investment over the last few decades, and could continue to be due to its brand strength, impressive earnings growth, and increasing dividend. But at 25 times earnings, is the stock too expensive?

Clorox segment and brand strength

This century-old company is a lot more than just the home-cleaning brand its name suggests, offering nearly 20 brands such as Glad and Burt's Bees. Most of the company's growth comes through acquisitions, which is how it has diversified across so many different segments from home care to other lifestyle products like body care. According to Clorox'swebsite, more than 80% of the company's sales are generated by brands that hold first- or second-place market share in their respective categories.

Data source: Clorox's 2016 earnings call.

For thefiscal year 2016 ended June 30, Clorox reported 2% sales growth, to $5.8 billion. The company noted that international currency headwinds were largely to blame for lackluster sales growth, and that excluding the effects of these foreign exchange fluctuations, sales would be up 5%.Sales picked up slightly in the fourth quarter, to 3% growth year over year; perhaps more important is that volume increased by 7% over the fourth quarter of 2015, compared with 4% for the full year.

Clorox has an impressive history of developing products, both via internal development and by acquiring and growing new brands. Clorox is currently working on a "2020 strategy" which is meant to boost overall market share through improvements in each category. "We are very pleased with our fiscal year 2016 performance and the progress we are making against our Strategy 2020 accelerators," said CEO Benno Dorer during the earnings conference call, "which I believe will continue to create value and drive long-term profitable growth in the years to come."

Image source: The Clorox Company.

Impressive earnings growth

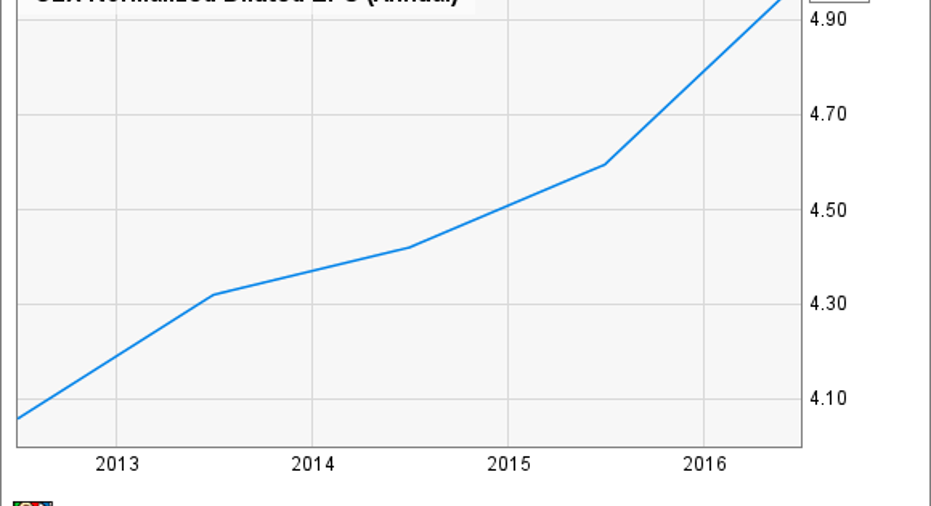

Earnings grew at a much faster rate than sales as earnings per share (EPS) climbed 12% year over year to $4.92. Clorox has continued to grow earnings impressively over each of the last five years.For fiscal year 2017, Clorox projects earnings per sharein the range of $5.38 to $5.58, which would be a 9% to 13% increase over 2016. That's substantial growth for a blue-chip stock like Clorox.

CLX Normalized Diluted EPS (Annual) data by YCharts.

Clorox's rising dividend

Clorox's dividend history is another reason the stock looks attractive. Its dividend is $3.20 per share ($0.80 per quarter), for a 2.5% yield at the current price. That dividend has nearly tripled in the last decade, though the yield has stayed relatively even because of share price growth at the same time. Clorox has shown itself to be an income generator, and is likely to continue growing this dividend for years to come:

CLX Dividend data by YCharts.

But is the stock too expensive?

Clorox stock has been a great investment in the past, especially in the last five years as the stock has more than doubled. But as the share price has grown, so has the stock's valuation, which is now around 25 times earnings. Compare that to its three biggest competitors,Colgate-Palmolive (NYSE: CL), Procter & Gamble (NYSE: PG), and Unilever (NYSE: UL):

Data sources: Company earnings releases, Yahoo! Finance. YOY = year over year; TTM = trailing twelve-month.

Clorox was the only company of those above to report rising earnings during the most recent quarter (in real dollars, not altering results to remove the effect of foreign currency swings) and also has the most impressive EPS growth. Its dividend is closely in line with its peers and has been growing substantially in the past decade.

Withthe promise of solid execution of the company's 2020 strategy,Clorox stock seems reasonably priced, and continues to look like a solid long-term holding.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Seth McNew has no position in any stocks mentioned. The Motley Fool recommends Procter and Gamble and Unilever. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.