Is NVIDIA a Future Blue Chip Stock?

The term "blue chip stock" carries a connotation of stability, safety, and often a laudable history of profit growth and steadily increasing dividends. If you were to ask someone for examples of a blue chip stock, you'd get names such asGeneral Electric, Coca-Cola, and Johnson & Johnson. However, these companies weren't always the gargantuan pillars of stability they are today. Even the most sainted of stock market names started out as small enterprises.

Enter NVIDIA Corp. (NASDAQ: NVIDIA), one of the best-performing stocks of the past 12 months and a burgeoning leader in not only high-performance graphics chips but also artificial intelligence. The stock is up more than 300% in the past 12 months and shows no signs of stopping. However, for NVIDIA's true long-term potential to be realized, it will have to become part of an elite group of companies in the upper echelons of corporate America, alongside the likes of Google and Microsoft.

Does NVIDIA have what it takes to become a future blue chip stock?

Image source: Getty Images.

Recent events

The past 13 or so months have been extremely good to NVIDIA shareholders. Since Jan. 1, 2016, shares are up some 268%, much of that gain coming in the last quarter of 2016 (fiscal third quarter of 2017), following a fantastic earnings release in October.Total sales exploded 54% to over $2 billion, fueled by gaming graphics cards, data-center applications, and potential developments in the automotive division. Earnings per share rocketed up some 90% year over year, to $0.83 per share.

Fourth-quarter results, released on Feb. 9, were even better. Revenue surged 55% year over year to $2.17 billion, gross margin came in at a healthy 60%, and earnings of $0.99 per share crushed Wall Street estimates of $0.85.

So investors have not only an extremely profitable and growing enterprise on their hands, but also one that has a great deal of future potential. That's a fantastic combination, should the company's management continue to implement on both its vision and the company's offerings. And under the leadership of CEO Jen-Hsun Huang,the company has a history of doing just that.

A history of excellence

NVIDIAwas founded in 1993 and went public in January 1999. The company quickly became a success as gaming in the home became more and more commonplace. Now, advanced graphics chips, of which NVIDIA is the No. 1 designer and manufacturer, are now found in most personal computers in the marketplace. NVIDIA's customers now include the biggest names around: Microsoft, HP, Dell, Sony, Apple, and scores of other computer system integrators.

But technology -- particularly hardware designing and manufacturing -- is a tough business to consistently make money in. Price deflation, fierce competition, and the constant need to stay ahead of the next innovation don't lend themselves to consistent profits for shareholders. In this regard, NVIDIA is a laudable outlier. Not only has it continued to grow both revenue and profit year in and year out for the past two decades, but it's also done so while consistently generating above-average returns on invested capital -- a rare thing in corporate America, let alone the technology industry.

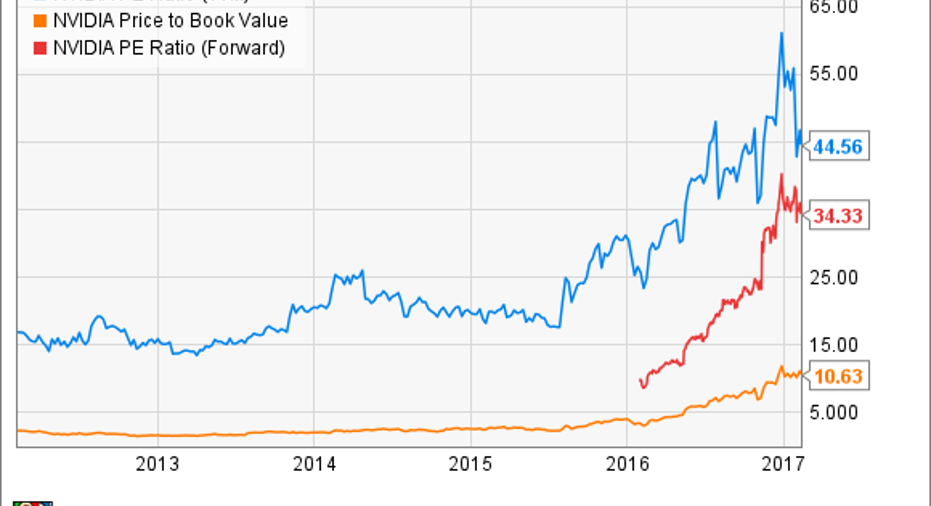

A valuation built on great expectations

NVIDIA's attractiveness as a stock begins to diminish somewhat when one casts an eye toward its current valuation.

NVIDIA PE Ratio (TTM) data by YCharts

In addition to a valuation that's priced to perfection, there are questions about NVIDIA's long-term competitive advantages. Does NVIDIA make the best products in the marketplace today? Absolutely. Does it have a unique offering in the burgeoning market of driverless-car computing? You bet.

However, for the company to truly become a blue chip stock, its business needs to become self-sustaining. Its products need to be so commonplace and necessary that it would be inconceivable for the company to not exist. Microsoft has 90% market share of operating systems, Alphabet'sGoogle search engine has a virtual search monopoly in the United States,Procter & Gamble'sTide laundry detergentis found in more laundry rooms in the world than can be counted, and there are scarcely any countries on Earth that don't have Coca-Colareadily available.

NVIDIA certainly has the best graphic chips available, and the demands of virtual-reality gaming alone may mean it has years of growth ahead of it, but consumers simply want their games to work flawlessly, no matter how that gets done. There's nothing to stop a new chip manufacturer to enter the market and steal away NVIDIA's bread and butter. It's simply the nature of the technology industry. Technology itself is forever changing -- and that means businesses need to constantly evolve or else face extinction. It seems that, at best, NVIDIA might become a future Intel (NASDAQ: INTC) -- a chipmaker with a brand name that commands respect and generates fantastic profit -- but one that has to always be on the lookout for competing products as it seeks to roll out new and better offeringsyear after year.

True blue?

NVIDIA is certainly a fantastic company and may very well continue to be a fantastic stock to own for years to come. Its management is top notch, and its participation in the burgeoning markets of driverlesscars and advanced gaming are intriguing. However, for the company to truly become a blue chip stock, it will need to build a business that's more recurring in nature, and not reliant on continued releases of newer and better products.

That doesn't mean NVIDIA isn't a stock to own; it just means that the odds of one day seeing it as a blue chip stock are low.

10 stocks we like better than NvidiaWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Nvidia wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fools board of directors. Teresa Kersten is an employee of LinkedIn and is a member of The Motley Fools Board of Directors. LinkedIn is owned by Microsoft. Sean O'Reilly has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Alphabet (A shares), Apple, and Nvidia. The Motley Fool owns shares of General Electric and has the following options: long January 2018 $90 calls on Apple and short January 2018 $95 calls on Apple. The Motley Fool recommends Coca-Cola, Intel, and Johnson and Johnson. The Motley Fool has a disclosure policy.