International Business Machines Corp. in 6 Charts

IBM (NYSE: IBM) is generally known as a slow-growth tech stock that provides a solid dividend but weak share price growth. To better understand Big Blue, here are six charts detailing the inner workings of its business.

Image source: IBM.

1. 17 quarters of revenue declines

IBM's biggest problem is its lack of top line growth. Sales fell 3% annually last quarter, marking the company's 17th consecutive quarter of year-over-year declines due to weak enterprise spending, currency headwinds, and tough competition in the IT, software, and hardware markets.

Data byYCharts.

Under CEO Ginni Rometty, who took the company reins in 2012, IBM divested units thatgenerated low-margin revenue, includingconsumer PCs, low-end servers, and its chip foundry, and acquired higher-growth businesses in the cloud, AI, mobile, social, and security markets.

2. The five strategic imperatives

IBM calls those five businesses its "strategic imperatives", and the combined sales from those units rose 12% annually lastquarter. This chart illustrates the revenue breakdown and growth rates of these key segments:

Image source: IBM investor presentation (aaS = as a service).

Over the past 12 months, those five businesses generated $31 billion in revenue and accounted for 38% of the top line. However, its "cloud as a service" annual run rate of $6.7 billion still trails far behind that of market leader Amazon, which posted an annual run rate of $11.5 billionfor its cloud platform, Amazon Web Services (AWS), last quarter.

3. Core businesses remain weak

While progress with the strategic imperatives looks encouraging, those five businesses are actually woven into IBM's other business units. This means that their growth looks a lot less impressive when we consider how these overall units are faring.

|

2Q revenue (billions) |

2Q YOY sales growth |

Strategic Imperatives growth (within the unit) |

% of sales from Strategic Imperatives |

|

|

Cognitive Solutions |

$4.7 |

4% |

9% |

64% |

|

Global Business Services |

$4.3 |

(3%) |

13% |

53% |

|

Technology Services and Cloud Platforms |

$8.9 |

0% |

35% |

22% |

|

Systems |

$2.0 |

(23%) |

(14%) |

45% |

Data source: IBM investor presentation (YOY = year-over-year).

This chart indicates that while revenue from strategic imperatives rose across all of the business units except for Systems, only the Cognitive Solutions unit (which includes the AI platform Watson) broke into positive territory overall. That's why IBM closed or announced the closure of ten different acquisitions to accelerate the growth of its strategic imperatives this year.

That said, sales growth is unlikely to return to positive territory anytime soon. Analysts currently expect the company's sales to dip 2.6% this year andanother 0.4% next year.

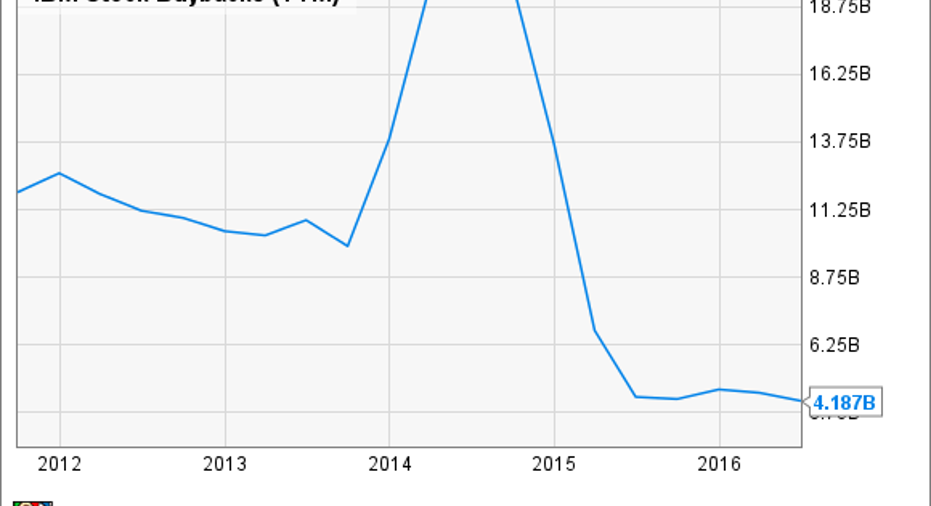

4. Reduced buybacks

Over the past two years, Rometty greatly reduced IBM's dependence on buybacks to inflate earnings without sales growth -- anunsustainable strategy her predecessor Sam Palmisano relied on.

Data byYCharts.

Previously, buybacks were funded by a combination of free cash flow and low-interest debt, so reducing them freed up more cash for investments, acquisitions, and dividends. It would also be logical to stop funding buybacks with debt as interest rates rise.

5. Free cash flow and dividend growth

If we look back at IBM's free cash flow growth over the past five years, we can see the positive impact of reduced share repurchases.

Data byYCharts.

Over the past 12 months, IBM spent just 36% of its free cash flow on dividends, which gives it plenty of room to continue its16 straight years of annual dividend hikes.

IBM currently pays a forward yield of 3.5%. That's higher than the yield of other "mature" tech plays like Microsoftand Intel, which respectively pay forward yields of 2.5% and 2.9%.

6. Empty calories and margin growth

Rometty frequently refers to IBM's divested businesses as "empty calories" which produced revenue without profits. However, the strategic imperatives aren't really high-margin businesses either.

Fierce competition has greatly reduced prices across the cloud and mobile markets. IBM's position as the underdog also doesn't give it the pricing power of bigger platforms such as AWS or Microsoft Azure. As a result, operating margins at IBM have gradually declined over the past two years.

Data byYCharts.

That decline has weakened its earnings per share, which fell 27% annually last quarter with less support from share buybacks. Analysts expect IBM's earnings to fall 9.5% this year but potentially rebound 4.4% in 2017.

The bottom line

IBM is still a company in transition. Its strategic imperatives are growing as a percentage of its top line, but their margins are questionable, and they continue to be weighed down by the company's legacy businesses. While the decision to reduce buybacks was wise, it also means that earnings growth will look ugly for the foreseeable future. All in all, IBM is a solid dividend stock with a fairly attractive valuation of less than 12 times full-year 2016 earnings, but I don't see it rallying anytime soon.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Leo Sun owns shares of Amazon.com. The Motley Fool owns shares of and recommends Amazon.com. The Motley Fool owns shares of Microsoft. The Motley Fool recommends Intel. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.