Intel Corporation Stock Surges to Multiyear High -- What's Next for Investors?

Murthy Renduchintala is responsible for Intel's PC and Internet of Things businesses. Image source: Intel.

During the Oct. 5 trading session, shares of microprocessor giant Intel (NASDAQ: INTC) hit $38.31 per share -- a high it hasn't seen since the dot-com bubble burst. At this point, current and potential Intel shareholders are probably asking themselves the following critical questions:

- What is driving the stock to these heights?

- Is the current price justified?

- Is there additional upside to be had?

In this column, I'd like to offer up some answers from the perspective of somebody who has held Intel stock for years now.

What's driving the stock?

Intel's business can largely be separated into three main categories: personal computer platform sales, data center platform sales, and everything else (Internet of Things, programmable logic, and non-volatile memory).

The bulk of Intel's revenue has historically come, and still comes, from the first group. In 2015, for example, Intel's client computing group (which consists primarily of personal computer chip sales) took in $32.22 billion in revenue -- approximately 58% of the company's top line for the year.

Even though Intel has made it clear that it's building its business to be able to deliver some level of growth even if the personal computer market continues to decline, the better this segment does, the better it is for Intel, its financial performance, and ultimately, its stock price.

I believe the momentum the stock is enjoying is driven in no small part by the company's positive earnings pre-announcement due to better-than-expected personal computer chip sales.

Is the current price justified?

As of this writing, Intel stock most recently closed at $38.07 -- just off of the new highs made earlier in the week. At that price, shares trade at about 18 times trailing 12-month earnings -- certainly at the high end of where it has traded over the last five years:

Data by YCharts.

However, it's not hard to argue that the company's prospects today are probably brighter than they've been in a long time.

To start, the personal computer market looks to be stabilizing after several years of steep unit declines. Moreover, the rest of Intel's businesses have grown significantly over that same period, particularly its data center group, which means Intel is less sensitive (though still quite exposed) to potential volatility in the personal computer market.

Image source: Intel 10-K filing.

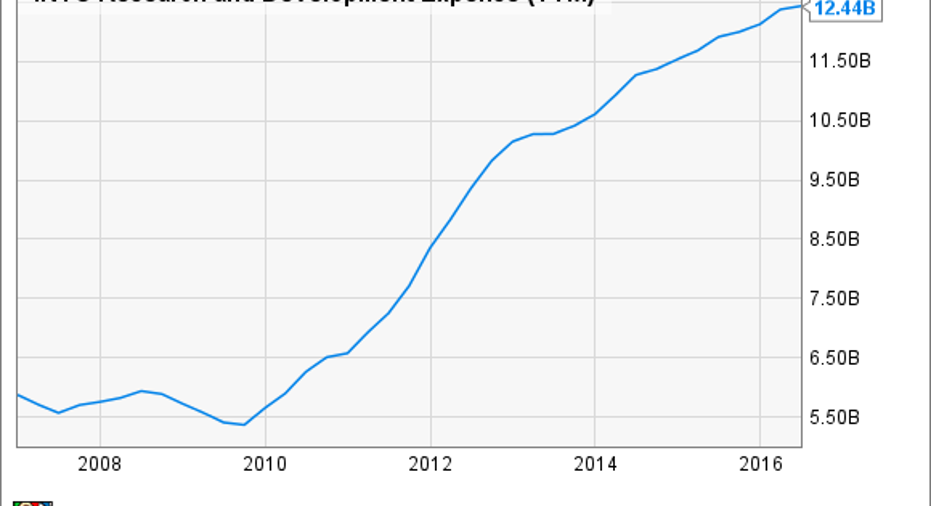

Intel has also ramped up its research and development spending quite substantially over the last five years in order to allow the company to better capitalize on new growth opportunities (though not all of them, such as smartphone/tablet platforms, have worked out) and to defend market share in its core operating segments.

Data by YCharts.

All told, I wouldn't hesitate to argue that Intel shares deserve the richer earnings multiple they command today.

What does the future hold?

At this point, current investors as well as potential investors are likely interested in the answer to our final question: How much, if any, upside is there left in the stock?

I suspect that how the shares perform over the next year or so will be largely governed by the following factors:

- Can the company deliver on double-digit growth in its lucrative data center business, as well as its other (albeit smaller) growth segments?

- Will personal computer sales continue to be "not terrible" throughout 2017?

I suspect the answer to the first point will be "yes". Intel's product portfolio in the data center market is currently strong, and I expect the company's 2017 product line will only strengthen that position -- helping to support both the unit growth and average selling price growth story that has driven this business segment for quite some time.

Perhaps the bigger unknown is how personal computer sales will hold up in 2017. Predicting this market has been tough in the past, and we've seen situations in which PC sales will do quite well in one year (Intel's PC business actually grew modestly in 2014) only to crater in the following year (it then contracted significantly in 2015).

If PC sales continue to hold up nicely, a share price of $43-plus (16 times the analyst consensus for Intel's earnings per share in 2017) wouldn't be out of the question. However, if PC sales start to reverse course, I'd expect the stock to stagnate, or perhaps even follow personal computer sales downward.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early, in-the-know investors! To be one of them, just click here.

Ashraf Eassa owns shares of Intel. The Motley Fool recommends Intel. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.