How Risky Is Procter & Gamble Co.?

Procter & Gamble (NYSE: PG) is considered one of the sturdiest stocks in the market -- and for good reason. The blue chip giant owns a broad portfolio of consumer brands, including blockbusters like Tide, Gillette, and Pampers. Its 60-year streak of annual dividend hikes is nearly unmatched.

Consumer staples, the category that P&G dominates, hold up well even through economic slowdowns. People continue to purchase razors, paper towels, and diapers, after all, even if budgetary concerns push them to cancel spending at restaurants or on vacations.

Image source: P&G.

However, a P&G investment isn't free of risks. In fact, the company is currently pursuing what management has called the biggest pivot in its 178-year history. That transformation, and the market stumbles that made it necessary, is the biggest concern for the business right now.

Market-share troubles

P&G has a serious market-share problem. Its expansion pace trailed that of the broader market in its main product categories last year, which led to its second straight year of disappointing organic growth. P&G's 1% uptick was well below the 4% to 5% gains that rivals Unilever (NYSE: UL) and Kimberly-Clark (NYSE: KMB) posted. Despite encouraging results from brands like Tide and Pampers, P&G failed to defend its turf against low-cost rivals, particularly in its grooming division. The company is also facing rising threats from in-store brands and online rivals.

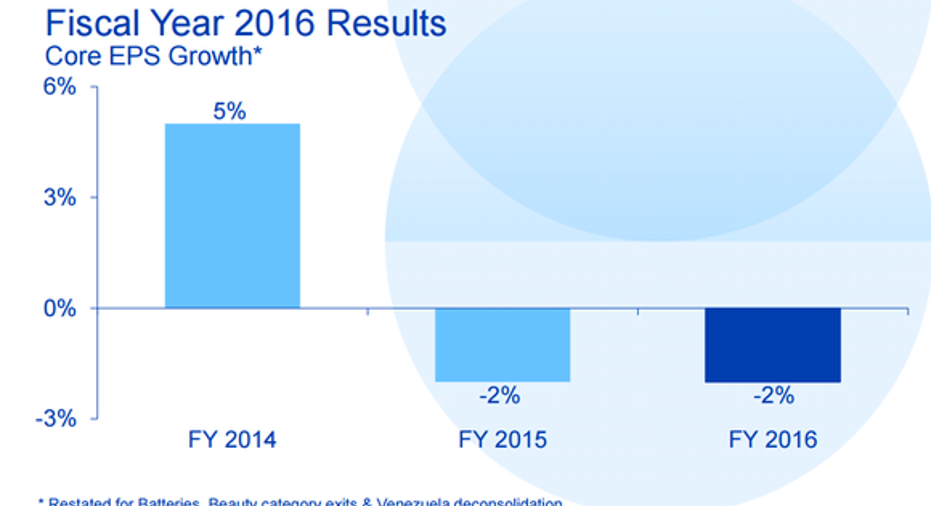

Earnings growth over the last three years. Image source: P&G investor presentation.

Market-share growth is fundamental to P&G's business model. Without it, the company can't produce at management's long-term goal of per-share earnings gains in the high single digits. Investors have seen firsthand how that breakdown plays out over the last two years. Core earnings fell from a positive 5% pace in fiscal 2014 to a negative 2% pace in each of the past two years. Yes, foreign-currency swings played a major role in that decline, but even after accounting for them, P&G's profit growth is half what it used to be.

Financial strength

The good news for investors is that P&G runs an incredibly efficient operation and management continues to find room to add to that efficiency. Executives have sliced billions of dollars out of cost of sales, overhead, and manufacturing spending. They plan to double down on those initiatives and remove a further $10 billion from the expense infrastructure over the next five years.

Costs are at an 11-year low.PG Cost of Goods Sold (TTM) data by YCharts.

Those cuts have helped preserve P&G's incredible cash flow production even in the face of declining revenue and profits. And, combined with the substantial windfall from selling off underperforming brands like Duracell batteries and Coty beauty products, the company is generating all the cash it needs to deliver increasing returns to shareholders -- at least through 2019.

Can P&G turn things around?

Cost cuts and brand divestments will only carry the company so far, though. P&G's most recent dividend boost, its smallest in recent memory, highlights the risk of continued market-share stumbles.

Looking ahead, the company aims to post a minor uptick in organic growth in the current fiscal year. Its latest results suggest that this rebound is likely. P&G recently managed an encouraging recovery in sales volume, after all.

Meanwhile, executives believe that their new, far more concentrated portfolio -- along with a much lower cost structure -- has laid the foundation for faster sales and profit growth over the next few years. If they're wrong, then shareholders are likely to see subpar stock appreciation matched with healthy cash returns, or roughly what they've witnessed over the past few years.

That's not an exciting prospect, but it's likely good enough for conservative investors who prize financial stability over the potential for outsize share-price gains.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Demitrios Kalogeropoulos has no position in any stocks mentioned. The Motley Fool recommends Kimberly-Clark, Procter and Gamble, and Unilever. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.