How Investors Should Think About Bank of America's Stock Right Now

Doing the math on Bank of America's stock. Image source: iStock/Thinkstock.

Bank of America (NYSE: BAC) is the largest holding in both my and my wife's retirement accounts. As such, it doesn't give me any satisfaction to share my opinion with you that there's probably little near-term upside left in its stock at this point.

Bank of America's soaring stock

Shares of Bank of America have soared since the presidential election one month ago. Going into November, they traded for less than $17 a share. Fast-forward to today and the price has risen to $22.57 a share, as of Wednesday's close.

That amounts to a 30% gain over the course of a month. They're now trading at a 52-week high. The last time Bank of America's shares were priced above $22 a share was in the fourth quarter of 2008.

Data source: YCharts.com. Chart by author.

I'm not saying that Bank of America's shares are expensive. They're not. At Wednesday's closing price, they trade for a 32% premium to the bank's tangible book value. That isn't cheap, and it may be a little on the high side when you factor in Bank of America's lagging profitability, but its valuation certainly isn't unreasonably high or low.

Bank stock valuations

Bank stocks tend to fluctuate in valuedepending on where we're at in the credit cycle -- which largely overlaps with the business cycle.

When times are good, as they were in the lead-up to the financial crisis, banks make a lot of money and their stocks trade for two or more times tangible book value. When times are bad, as they were in the wake of the crisis, banks make much less money and often lose money, and their stocks will trade for half of tangible book value, if not less.

The question of whether a particular bank is over- or undervalued thus depends on its profitability, both in terms of where it is today and in terms of the direction in which the bank's earnings are headed.

A good rule of thumb is that a bank will (and should) generally trade for a premium to its tangible book value if it's creating value for shareholders. That makes sense, right? If a bank is creating value, then investors should be willing to pay more for its stock than the static value of the bank's shareholders' equity.

To determine whether a bank is creating value, you look at its return on tangible common equity. Generally speaking, if a bank's return on tangible common equity exceeds 10%, then it's most likely creating shareholder value. And the more that a bank's return on tangible common equity exceeds the 10% threshold, the higher its valuation is likely to be.

Bank of America's profitability

In Bank of America's case, it has struggled since the 2008 crisis to exceed this threshold on a consistent basis. It did so in the second and third quarters of 2015, but then slipped below the mark for two quarters until exceeding it again in the second and third quarters of this year. Its return on tangible common equity in the latest quarter, the third quarter, was only 10.28%.

By way of comparison, many of Bank of America's competitors consistently earn much more than that. Wells Fargo's return on tangible common equity last quarter was 13.96%, JPMorgan Chase's was 13%, and U.S. Bancorp's was 13.5%.

Based on this alone, then, it'd be tempting to conclude that Bank of America's shares are overvalued. If it's only barely creating value for shareholders by narrowly exceeding its cost of capital, then its shares should probably be valued only slightly above its tangible book value.

An upward trajectory

As I mentioned earlier, however, it's not only how profitable a bank is today that matters but also how profitable it's likely to be going forward. Bank of America performs much better on this note.

After spending years under constant bombardment from unconscionably high loan losses, regulatory fines, and legal settlements, Bank of America has finally emerged into the clear and is starting to see its earnings improve on a sustainable basis.

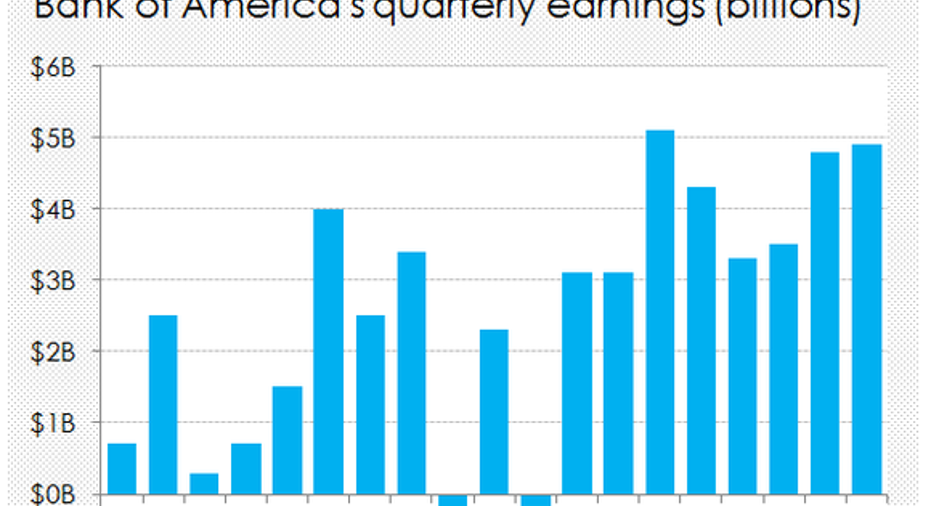

Data source: Bank of America's quarterly earnings. Chart by author.

Last year was its best since the financial crisis by far in terms of its bottom-line earnings, reporting $15.9 billion worth of net income. That was more than three times its 2014 earnings or $4.9 billion. And 2016 is shaping up to be even better than 2015.

In other words, when you look at the cold, hard facts, there's reason to be optimistic that Bank of America's profitability will continue to head higher. And because stocks tend to be priced with the next year's performance in mind, it makes sense that its current valuation seems to be outpacing its current performance.

The Trump bump

Added to this are expectations that the incoming Trump administration, together with a Republican-controlled Congress, will dramatically improve the operating environment for banks, making it easier for the industry to earn more money. I've discussed Trump's proposals in this regard ad nauseam over the past month, so I won't delve into them here, but the reasons revolve around the growing likelihood of fiscal stimulus, higher interest rates, and a lighter regulatory environment. (To dig into these, just click on the links.)

I can't emphasize enough how significant this could be for Bank of America. Not only would it allow the bank to generate more revenue and cut regulatory and compliance costs, but it'd also give the bank more leeway in terms of increasing its dividend and buying back more stock. All of these things would be good for Bank of America's profitability and thereby its stock valuation.

When you combine these expectations with the upward trajectory of Bank of America's earnings, it's easy to see why its shares trade for a 30% premium to book value even though it's only narrowly exceeding its cost of capital and thereby only marginally creating value for shareholders.

But here's the catch: It's my opinion that essentially all of these things are now baked into Bank of America's stock. Additionally, while I may be wrong, it's also my opinion that for Bank of America's stock to maintain its current valuation, most of these things will have to play out in its favor. This may happen, but there's also the risk that it won't.

Thus, while Bank of America's stock may continue to go up marginally from here, there certainly doesn't seem to be much upside left in it. Again, I may be wrong on this, and hope that I am given that it's the biggest holding in both my and my wife's retirement accounts. That said, at the very least, I don't think buying in now is an overly prudent bet.

10 stocks we like better than Bank of America When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Bank of America wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

Feel free to email John at jmaxfield@foolcontractors.comor connect with him on Twitter or on LinkedIn.John Maxfield owns shares of Bank of America, U.S. Bancorp, and Wells Fargo. The Motley Fool owns shares of Wells Fargo. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.