Honeywell International Earnings: What to Look Out For

Earnings season has kicked off, and industrial bellwether is set to join the party on Friday. Following its aborted bid for , investors will be eagerly following Honeywell's results to see if its ongoing plans are on track. Let's take a look at three key things to look out for in the results.

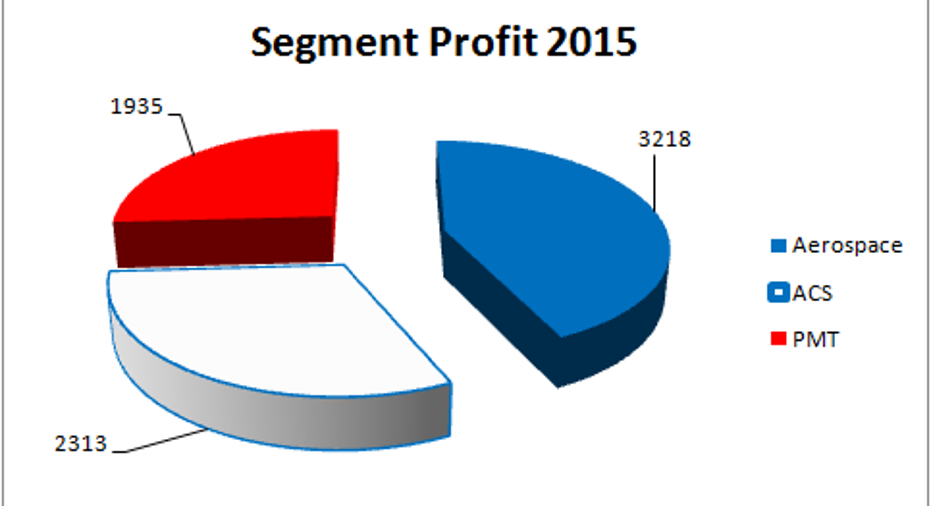

Honeywell reports out of three segments, the relative importance of which can be seen by looking at last year's segment profits. (ACS stands for Automation and Control Solutions, and PMT for Performance, Materials, and Technologies.)

DATA SOURCE: HONEYWELL INTERNATIONAL PRESENTATIONS.

Will aerospace get hit in the first quarter? It's early on in earnings season, but two companies have already come out and spoken of some softness in 2016. First, industrial supply company 'smanagement spoke of weakness in March because of a "push out in orders of commercial aircraft." Meanwhile, aluminum supplier reduced its guidance for aerospace growth in 2016, with CEO Klaus Kleinfeld outlining howan "unprecedented level" of new aircraft platforms was causing lower orders for legacy models, and ''careful ramping" of production on the newer platforms.

These issues could prove especially problematic for aerospace suppliers such as Honeywell and United Technologies. Both companies are already prepared for sales and earnings headwinds from aerospace in 2016 because of the newer aircraft platforms.For example, Honeywell is granting incentives to establish itself on newer platforms -- all the better to generate future recurring revenues. According to management's guidance, the incentives will reduce commercial aerospace original equipment sales from low single digits to a decline in the mid-single digits.

Similarly, United Technologies' management is forecasting a negative $225 million impact from the changes in volume and mix on the newer platforms. Sales on legacy platforms tend to be higher margin, as the company has reduced production costs over time.

With both companies already forecasting aerospace headwinds in 2016, any kind of additional issues -- such as slower production on new aircraft platforms, or a push-out of legacy plane orders -- will hurt Honeywell in the near term. Look out for management's commentary on the issue.

Oil and gas outlook Honeywell isn't often thought of as an energy-related company, but oil and gas-related solutions contributed 13% of 2015 revenue. However, more than three-quarters of its oil and gas sales are in the midstream (transportation and wholesaling) and downstream (refining and processing) end markets. In theory, these markets should do well when oil prices fall, because volumes should pick up as economic growth receives a fillip from lower fuel prices.

It didn't work out like that in 2015, and as Honeywell CEO Dave Cote outlined at the recent investor conference, management got it wrongwith its previousforecast that lower energy prices would have little effect on its oil and gas business. Looking at current guidance, Cote expects sales for UOP -- Honeywell's oil and gas-focused business in PMT -- to bottom out in 2016 and then increase by $200 million in 2017.

However, given that the International Monetary Fund recently cut its 2016 global growth forecast to 3.2% from a forecast of 3.4% in January, and oil prices remain around $40, hurting Honeywell's upstream oil and gas business, will Honeywell be forced to reduce its PMT outlook?

ACS set for a good quarter The ACS segment generates 22% of its revenue from homes, 44% from commercial buildings, and 34% from industrial solutions. Products range from fire alarm systems and CCTV to industrial safety products and energy management solutions to smart metering and heating controls.

Going into 2016, building and construction, alongside aerospace and automotive, was widely expected to be one of the relatively strong sectors of the industrial economy. However, it's hard to guess exactly how conditions are faring. For example, the Dodge Momentum Index -- a widely respected leading indicator of nonresidential construction -- was positive from December to February, only to decline 7% in March.

On the other hand, Alcoa kept intact its full-year expectation for 4% to 6% global growth in its building and construction end markets intact, and MSC Industrial's non-manufacturing (construction-heavy) sales increased 2.6% in the first quarter compared with 1.3% in the fourth quarter of 2015.

Looking aheadHoneywell achieved core sales growth of 1% in 2015, and although management forecasts just 1% to 2% for 2016, it expects an "organic growth inflection" to begin at the end of 2016, leading to core organic growth of 4% to 5% in 2017. It's fair to say this optimism is now baked into the stock price. The thing is, Honeywell will need to deliver in 2016 first, and the upcoming results should tell investors a lot about the company's prospects to do so.

The article Honeywell International Earnings: What to Look Out For originally appeared on Fool.com.

Lee Samaha has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.