Holly Energy Partners Earnings Hit a Small Bump, but It Expects to Recover Quickly

This third quarter, we saw something that is a bit of a rarity with Holly Energy Partners' (NYSE: HEP) earnings: A decline in distributable cash flow. The company's business model and contracts are supposed to be completely commodity-risk-free, so what the heck is going on here? Let's take a look at the Holly Energy Partners' most recent results and see if this slight dip is cause for concern.

Image source: Getty Images.

By the numbers

Data source: Holly Energy Partners earnings releases.

This is a funky quarter for Holly Energy Partners. On Sept. 19, the company completed the dropdown of several assets totaling $275 million that were funded in part with the issuance of debt back in July. As a result, interest expenses increased 52% compared to the same quarter last year to $14.4 million. Since those assets weren't dropped down until later in the quarter, Holly Energy Partners operational profits didn't increase enough to offset these higher interest expenses. This is a large part of the reason why there was a decline in distributable cash flow.

Management expects that next quarter this issue will be alleviated as a full quarter of those assets operating will generate more than enough cash to make up the difference and boost distributable cash flow.

The highlights

Those assets that Holly Energy Partners received from parent company HollyFrontier (NYSE: HFC) were several refinery units at its Woods Cross facility. If this comes as a bit of a surprise, that's because it is. Even in the company's most recent investor presentation in August, it didn't have any plans of acquiring these refining units. Nor did management give any indication that it was planning to do this deal on the company's previous earnings conference call.

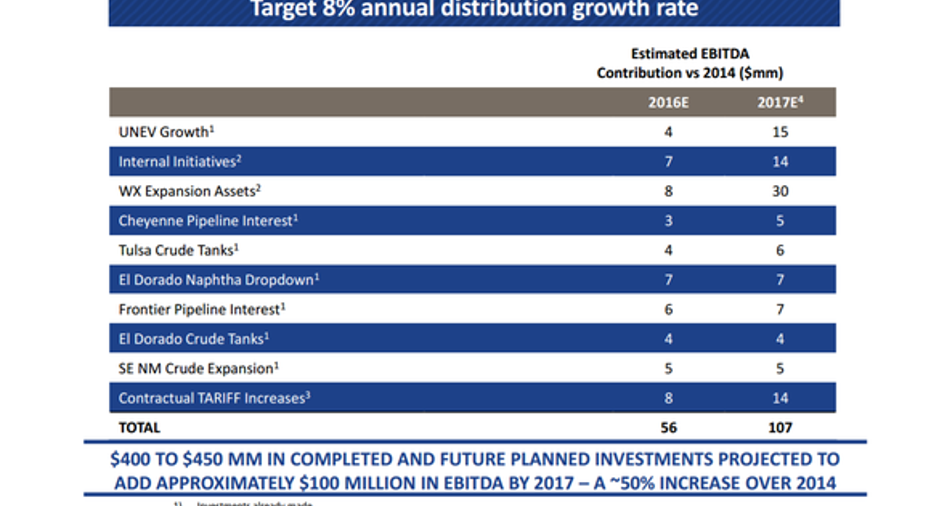

Data source: Holly Energy Partners investor presentation.

One concern that investors might have with this kind of deal is that refining is a much more cyclical business than traditional midstream businesses. While it's hard to say without seeing these assets in action if that variability is going to cause any headaches in the future, one thing that this deal does have going for it is that Holly Energy Partners signed a 15-year tolling agreement with HollyFrontier with these assets, which is very similar to the tolling agreement it has with some assets at HollyFrontier's El Dorado facility. These agreements have minimum volume commitments and no commodity risk. That should help to ensure that these refining units remain profitable for Holly Energy Partners.

What management had to say

CEO George Damiris used the press release to ensure investors that this dip in cash flow was a temporary issue because of the Woods Cross dropdown and it should be resolved shortly.

What a Fool believes

Aside from the small blip from the Woods Cross acquisition, Holly Energy Partners' earnings were solid. The only lingering question is whether the addition of Woods Cross is going to give the company as much of a cash flow uplift as management hopes. We'll have to wait next quarter to see how this dynamic plays out. In the meantime, it's probably best to sit tight and not make any significant changes to your investing thesis.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Tyler Crowe has no position in any stocks mentioned. You can follow him at Fool.comor on Twitter@TylerCroweFool.

The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.