Here's How Retirement Saving Changed in 2015

Photo: www.TaxCredits.net via Flickr.

In 2015, there were a few notable changes to the ways you can save for retirement. A new type of retirement account was created, many savers are allowed to contribute more to their retirement accounts, and certain retirement-related income thresholds were increased. Here's what changed in 2015, and what we can expect in 2016.

The MyRA account is a new optionPerhaps the most significant change to retirement saving that took place in 2015 was the implementation of the MyRA account, which the U.S. Treasury introduced as a retirement savings option for individuals without access to employer-sponsored retirement plans.

Structured like a Roth IRA, MyRA offers contributions that aren't deductible, but qualified withdrawals are tax-free. Contributions are limited to $5,500 per year ($6,500 if you're over 50) and are guaranteed not to lose money.

While this sounds good in principle, there are a few major drawbacks. For one thing, account holders can contribute to a MyRA account only until the balance reaches $15,000, at which point they must be rolled over or transferred to a Roth IRA. And the sole investment option is a Treasury bond fund, which has averaged a low 3.2% annual total return over the past decade.

Basically, while the MyRA isn't a bad idea, there are better retirement accounts. For more about the MyRA account, here's a more in-depth discussion, as well as some alternatives to start saving.

Retirement savings contribution limits have increasedSome of the contribution limits for various retirement savings accounts increased from 2014 to 2015, along with the catch-up contributions allowed for savers over age 50. Here's what changed:

It's also worth mentioning that the 2015 limits will carry over into 2016. For example, if you have an IRA, you'll be allowed to contribute up to $5,500 ($6,500 if you're over 50) for both the 2015 and 2016 tax years.

Income thresholds are higherAnother aspect of retirement saving that changed in 2015 is the various income thresholds used to qualify for certain account types and tax benefits.

For starters, the maximum adjusted gross income to contribute directly to a Roth IRA increased by $2,000 for both single and joint filers. Married taxpayers who choose to file separately remain ineligible for Roth contributions if they earn over $10,000. If you want to contribute to a Roth IRA in 2015, here's what you need to know about the AGI limits.

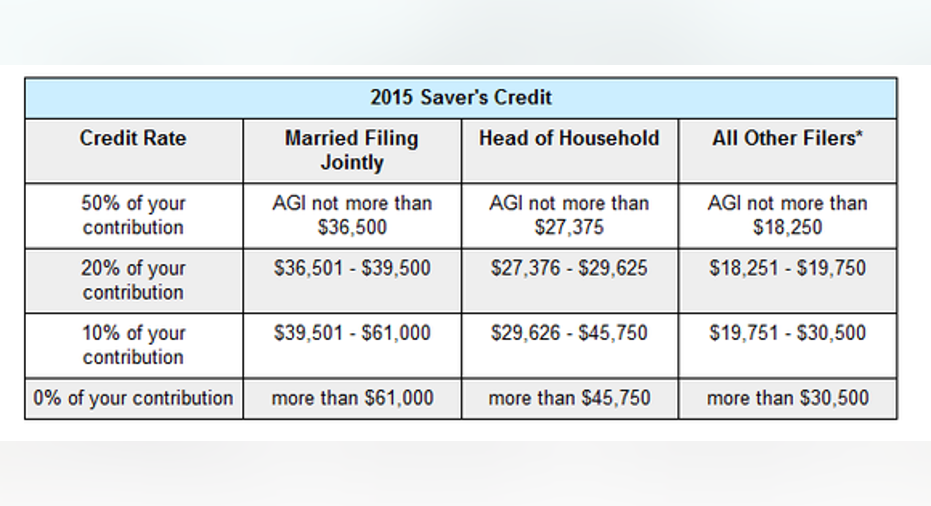

The income thresholds to qualify for the Retirement Savings Contributions Credit, also known as the saver's credit, increased slightly for 2015. Here's the 2015 qualification information based on income and filing status for the 10%, 20%, and 50% tax credits, all of which have been adjusted upward by 1.5% to 3% from 2014.

Source: IRS.

Finally, the income thresholds to deduct traditional IRA contributions on a 2015 tax return are slightly higher than they were in 2014. If you're not eligible to participate in an employer's plan but your spouse is, you can deduct traditional IRA contributions as long as your joint AGI is below $193,000, up from $191,000 in 2014. For those who are covered by an employer's plan, contributions can still be deducted with AGI below $71,000 and $118,000 for single and joint filers, respectively, up from $70,000 and $116,000 in 2014.

Other changesThere were a couple of other changes to retirement savings in 2015 that are worth mentioning.

A new rule regarding IRA rollovers went into effect in January limiting IRA rollovers to one per year between accounts of the same type. In other words, if you want to combine two traditional IRA accounts by rolling one into another, you won't be allowed to roll over another traditional IRA for another year. Here's a table from the IRS that clarifies the rollover rules.

Source: IRS (link opens PDF).

Finally, the amount of income subject to Social Security tax increased from $117,000 in 2014 to $118,500 in 2015. This change affects high-income individuals and can result in a maximum of $93 in additional Social Security tax for employees and $186 for self-employed individuals.

2016 will be a year of fewer changesWhile there's no way to predict with absolute certainty what will happen in the coming year, all signs so far indicate a quiet 2016 in terms of changes to retirement savings. Thanks to stagnant inflation in 2015, the retirement savings contribution limits remained the same, and slight adjustments were made to certain income thresholds.

The article Here's How Retirement Saving Changed in 2015 originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.