Form SSA-1099: What Everyone on Social Security Should Know

Retirees often think that they don't need to worry too much about their taxes, largely because their lack of wage income means they don't have to pay Uncle Sam very much every April. But every year during tax season, the Social Security Administration sends out information on Form SSA-1099 to anyone who receives Social Security benefits, and it's important to know what you're supposed to do with this tax form and how it can affect what you owe the IRS. Let's take a closer look at Form SSA-1099 and the key facts you need to know.

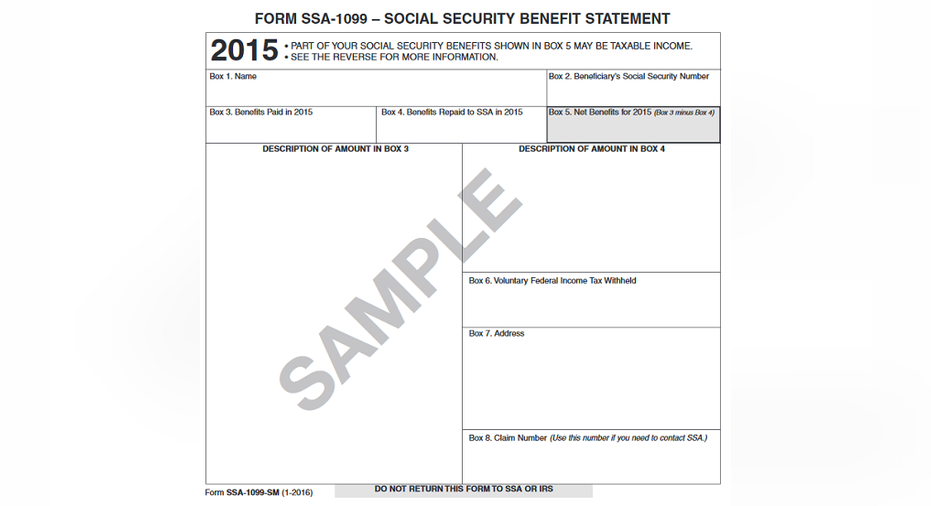

What you'll find on Form SSA-1099 The information you'll find on Form SSA-1099 couldn't be simpler. In addition to identifying information like your name and Social Security number, you'll find the total benefits that were paid to you during the year in Box 3. If you repaid any benefits back to the SSA, they'll show up in Box 4 on the form, and the net figure will appear in Box 5. If you elect to have tax withheld from your Social Security checks, that will be reflected in Box 6.

Image: IRS.

Form SSA-1099 can also include supplemental information. For instance, if you're on Medicare, then your monthly Part B premiums will typically get deducted directly from your benefits. A description of that withholding will appear in the box marked Description of Amount in Box 3. In addition, if any money was attributable to benefits from a prior year that you received in a lump sum, those details will be broken out by year in that box.

How Form SSA-1099 can affect your taxesThe reason why Social Security recipients need to look closely at Form SSA-1099 is that it plays a key role in letting the IRS know whether your benefits will be subject to tax. In particular, the IRS calculates a figure it calls "combined income," which adds up any wage or salary income you have, as well as investment income, business income, or other reportable income. It then adds in one-half of the Social Security benefits reported on Form SSA-1099.

Most Social Security recipients don't have to pay any tax on their benefits because their combined income doesn't exceed the threshold amounts in the tax laws. If you're single and the number is less than $25,000, then none of your Social Security will get taxed. For joint filers, the threshold number is $32,000.

Above those amounts, however, some of your benefits will be added to taxable income. For singles with combined income between $25,000 and $34,000, as much as one-half of your benefits can be subject to income tax, although many will pay lesser amounts. Above $34,000, the maximum amount rises to 85% of the benefits reported on Form SSA-1099. The corresponding figures for joint filers are $32,000 to $44,000 for the 50% limit and above $44,000 for the 85% limit.

It's important to understand that even if your income is above the relevant thresholds, you won't necessarily have to include the full 50% or 85% in your taxable income. This IRS worksheethas all the details, and you can tell from its 19 lines that there's a lot that goes into it. The gist of it, though, is that taxpayers who have significant outside income from other sources will typically see more of their benefits taxed.

Planning to reduce taxable Social Security incomeBy the time you get Form SSA-1099, it's usually too late to do anything to reduce the amount of Social Security income that you'll pay tax on. But for future years, keep in mind that your outside income sources help determine taxation. Timing of investment sales that generate taxable gain and retirement account distributions that boost your taxable income can lead to a heavier tax burden on your Social Security benefits as well. By being smart about other taxable events, you can control the tax on your benefits.

Form SSA-1099 might seem like just another information return, but it actually contains some critical information. Making sure you have the form available when you prepare your tax return is essential in order to avoid mistakes that could lead to an audit.

The article Form SSA-1099: What Everyone on Social Security Should Know originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.