Does Freeport-McMoran's Oil and Gas Restructuring Finally Signal The Bottom For Oil Prices?

Source: Freeport-McMoran website.

At the very end of 2012, world-class minerals producer Freeport-McMoran (NYSE: FCX) announced that it was aggressively diversifying into the oil and gas business with not one but two acquisitions. The companies acquired were both focused on offshore production in the Gulf of Mexico.

Those acquisitions have turned out to be an absolute disaster for FCX, given the subsequent collapse in oil and gas prices.

Now just a few years later, Freeport-McMoran has announced that it is completely restructuring its oil and gas businesses and is looking to monetize those assets.

Nobody knows if we are near the bottom for oil prices, but there is certainly no doubt that we are a long way from the top where Freeport acquired these properties. Selling at this point into a market with limited buyers, loads of sellers and a dismal oil price isn't going to fetch anything other than a disappointing price.

Jumped in to oil and gas with both feet at a terrible timeThey didn't buy at the very top, but they came very, very close. In late 2012, Freeport-McMoran paid $9 billion through a combination of cash and shares for Plains Exploration and McMoran Exploration.

For many shareholders, the move was a head-scratcher. For many others it was a reason to get angry. The subsequent collapse in oil and gas prices hasn't done anything to improve shareholders' view of the deal.

The head-scratching came from the fact that 18 years prior, one of the companies being acquired, McMoran Exploration, had been spun out of Freeport-McMoran. The deal would undo that spin-out and in the process cost shareholders a great deal of money via investment banking fees.

The anger came from the fact that it was nearly impossible to see how combining a mineral mining company and an offshore oil and gas explorer would create cost synergies for anyone. Even more anger stemmed from the fact that McMoran Exploration shares had been plummeting because of struggles the company was having with its hugely expensive ultra-deep Davy Jones exploration well.

More than a few people wondered if this deal wasn't motivated by the desire to save McMoran Exploration. At the time of the deal, Freeport and McMoran Exploration had six shared board members, which raised more than a few eyebrows. Freeport McMoran also controlled 36% of the shares of McMoran (including those that Plains Exploration held) so the company did have a vested interest in providing a lifeline.

A lifeline may have been understandable, I'm not sure about paying a premium for the entire company.

Now already oil and gas seems to be just an afterthought ...I'm always amazed at how so many management teams can't use the cyclical nature of this business to their advantage. When commodity prices are high and cash flows strong, many teams get aggressive on the acquisition front. Then when commodity prices are low and cash flows crimped, they start selling assets to save their balance sheets.

They have it backwards, in my opinion.

Freeport-McMoran paid premium prices to buy these oil and gas assets in late 2012. Last fall they announced that they were trying to sell them to improve the corporate balance sheet.The demand for offshore oil and gas assets couldn't be lower than it is now, with oil and gas prices both at the lowest point in recent memory.

Simultaneous with this situation, Freeport is firing all of its top oil and gas executives in an effort to reduce corporate overhead and plans to significantly curtail oil and gas spending in 2016.The company is undertaking a near-term deferral of exploration and development activities by idling the three deepwater drillships it has under contract. That's another bitter pill for shareholders to swallow as Freeport expects to incur idle rig costs tied to those drillships of $600 million in 2016 and another $400 million in 2017.

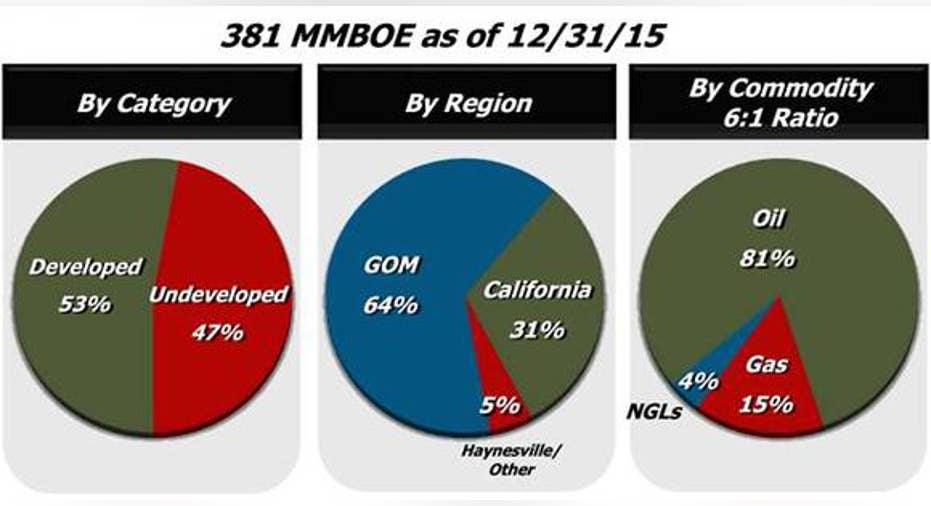

The company's view of the oil and gas business has dampened to the point where a single slide in the entire company presentation is now allocated to the oil and gas business.

Source: Freeport Corporate presentation.

This company got very bullish on the oil and gas business at exactly the wrong time and shelled out $9 billion because of it. How much do you want to bet that it's trying to exit the business also at exactly the wrong time?

Investor takeaway: good contrarian signal, but not the stock to profit from itMy opinion is that oil is bottoming out and that we'll see a recovery through the second half of 2016. I believe Freeport's turning its back on it oil and gas business is a true contrarian indicator.

I wouldn't, however, be interested in owning Freeport-McMoran to take advantage of an oil recovery. To own Freeport you need to be bullish on copper prices.

Source: Freeport corporate presentation.

For Freeport, each 10-cent change in the price of copper in 2016 will cause a $550 million change in EBITDA. Despite its spending $9 billion on oil and gas assets in 20121, it will be copper and not oil that determines the success of this company going forward.

The article Does Freeport-McMoran's Oil and Gas Restructuring Finally Signal The Bottom For Oil Prices? originally appeared on Fool.com.

TMFWolfpack has no position in any stocks mentioned. The Motley Fool owns shares of Freeport-McMoRan Copper & Gold,. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.