Does Enterprise Products Partners LP's Interest in Williams Companies Inc. Make Sense?

Image source: Getty Images.

According to some reports last week, Enterprise Products Partners (NYSE: EPD) is interested in acquiring Williams Companies (NYSE: WMB). Enterprise's initial bid came shortly after Williams' merger with Energy Transfer Equity (NYSE: ETE) was terminated, following a bitterly fought court battle. While Williams reportedly rejected that initial bid and developed a new go-forward strategy, that has not diminished Enterprise Products Partners' interest in pursuing a merger. That said, while the deal has merits, it has several obstacles to overcome.

Why Williams Companies?

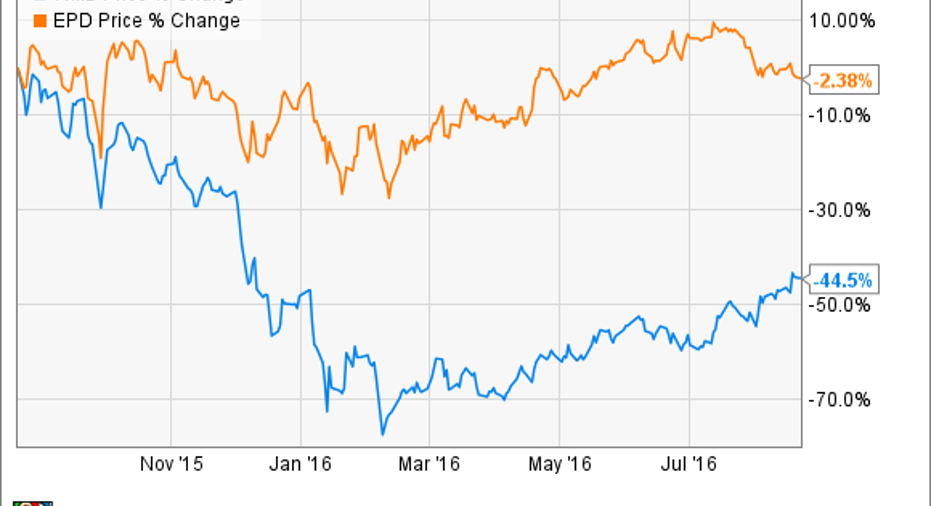

Enterprise Products Partners' interest in Williams Companies is about three things: value, optimization, and growth. Regarding value, Williams Companies' stock is down roughly 45% over the past year, as a result of its merger debacle with Energy Transfer Equity and the impact of the energy market downturn on its business. Meanwhile, Enterprise's unit price is roughly flat over that same time:

Because of that value gap, the acquisition would likely be meaningfully accretive on a per-unit basis.

Second, Williams' MLP Williams Partners (NYSE: WPZ) operates an excellent natural gas liquids (NGL) business in the Northeast, thanks to its prime position in the Marcellus shale. Not only is that an area where Enterprise Products Partners lacks scale, but it also controls the ATEX pipeline, which takes NGLs from the Northeast to the Gulf Coast marketplace. It could generate significant revenue and cost synergies by linking those two businesses.

Finally, Williams Companies and Williams Partners have more growth opportunities than they can fund at the moment. That is why Williams Companies cut its dividend and redirected that cash flow into its MLP, to provide it with some of the money it needs to fund its growth projects. Currently, Williams Partners has $5 billion in growth capital expenditure requirements through next year, which is just slightly less than the $5.6 billion that Enterprise Products Partners has under construction. That is worth noting because Williams Partners is about half the size of Enterprise Products Partners. Further, before the energy market downturn, Williams Companies estimated that it had over $30 billion of growth projects in its pipeline, which included potential projects and those under negotiation. That is a huge growth backlog that Enterprise Products Partners would love to have to itself.

The potential dealbreaker

While there are three compelling reasons why Enterprise Products Partners would want to acquire Williams Companies, there are two big red flags that could make this pursuit end just as badly as Energy Transfer Equity's ill-fated attempt. First, Enterprise Products Partners prides itself on having one of the highest credit ratings among MLPs, at Baa1/BBB+. That strong credit rating could be at risk if Enterprise bid for Williams Companies because the latter company's BB/Ba1 credit rating is below investment grade, while Williams Partners' credit rating of BBB-/Baa3 is at the lowest level of investment grade.

Having its credit rating downgraded could significantly increase Enterprise Products Partners' borrowing costs. For perspective, earlier this year it was able to borrow $1.25 billion, including pricing $575 million of 10-year debt at 3.95%. Williams Partners, on the other hand, issued $1 billion of 10-year debt earlier this year at a 7.85% interest rate. Enterprise Products Partners' stronger credit rating is a clear competitive advantage right now, and one it would not want to lose by acquiring Williams Companies.

The second hurdle to overcome is the fact that Williams Companies is structured as a C Corporation, while Enterprise Products Partners is an MLP. That was an issue that MLP Energy Transfer Equity tried to address by creating a C-Corp entity to merge with Williams. However, Energy Transfer Equity's lawyers did not find that the deal structure freed investors from tax liabilities. As a result, a judge ruled that Energy Transfer Equity could terminate the merger.

This suggests that Enterprise would need to take a different path, such as the one it made when it bought its general partner in 2010. However, such a deal structure would likely trigger taxes for Williams' investors, which might not be a palatable solution given what they have gone through over the past year. In other words, Enterprisemight need to pay up to convince Williams Companies' investors agree to a merger, but it needs to avoid taking on debt to do so, which was Energy Transfer Equity's downfall.

Investor takeaway

While Enterprise Products Partners' interest in Williams Companies certainly makes sense from a strategic and value standpoint, the proposed combination still raises questions. Most pressing is whether Enterprise can structure a transaction to win the support of Williams' investors without tarnishing its prized credit rating. If it can figure out a way to appease everyone, then this combination could really pay off in both the short and long term.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Matt DiLallo owns shares of Enterprise Products Partners. The Motley Fool recommends Enterprise Products Partners. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.