Diamond Offshore's Big Asset Impairment Sends Second Quarter Earnings to a Deep Loss

Image source: Getty Images

Diamond Offshore's (NYSE: DO) per share loss of $4.30 this past quarter stands in pretty stark contrast with the company's more recent earnings, but that's because the company took some pretty large non-cash charges to the income statement. Without those charges, the company's earnings looked surprisingly healthy considering how tough the offshore rig market is these days. However, management is still warning investors that things will likely get much worse before they get better. Here's a quick snapshot of the company's recent results and why management is giving investors ample warnings about the near term future.

By the numbers

| Results (in millions, except per share data) | Q2 2016 | Q1 2016 | Q2 2015 |

| Revenue | $388.7 | $470.5 | $634.0 |

| Operating income | ($626.7) | $111.6 | $134.1 |

| Net income | ($589.9) | $87.4 | $90.3 |

| EPS | ($4.30) | $0.64 | $0.66 |

Source: Diamond Offshore earnings release

As you might have guessed looking at those results for the most recent quarter, there were some pretty large charges and impairments that impacted earnings results. For the second quarter, Diamond took a pre-tax $678 million asset impairment for 8 of Diamond's semi submersible rigs. According to management, this resulted in a $4.46 after-tax per share impact on net income. So on a pure operations standpoint, the company is still making money.

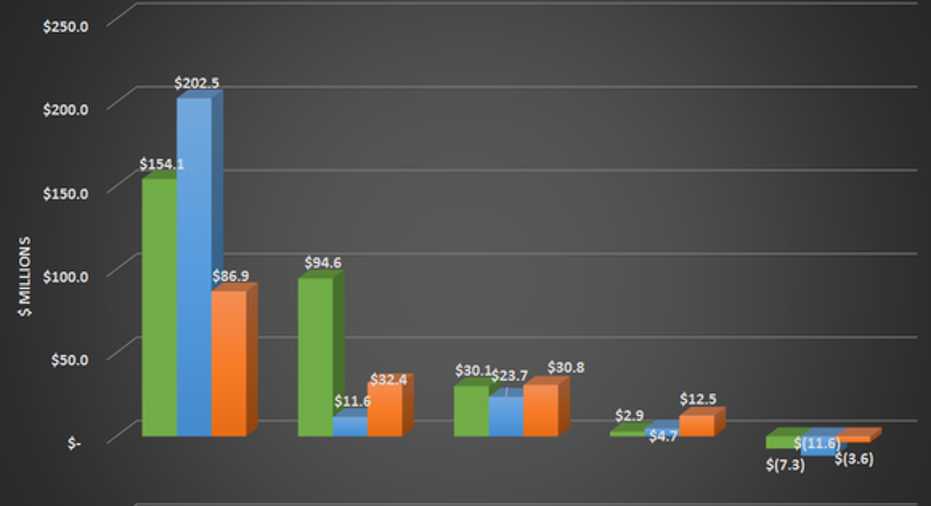

The largest declines in profitability came from the company's ultra-deepwater segment. In fact, the rest of the company's segments saw an increase in operational profits thanks to either higher revenue or lower operational costs.

Source: Diamond Offshore earnings release, author's chart

One thing that management did note is that results were significantly impacted because of unplanned downtime related to unplanned maintenance on blow out preventors on four of its ultra deepwater rigs. These blow out preventors were part of the deal that Diamond signed with General Electric earlier this year. As we head into the next quarter, we should expect earnings from its ultra deepwater segment to increase.

The highlights

- Management decided to cold stack two of its rigs -- Ocean Endeavor and Ocean Scepter -- in order to cut costs while demand for offshore rigs remains weak

- Diamond decided to also intend to scrap two rigs -- Ocean Quest and Ocean Star.

- The deepwater rig Ocean Apex began an 18 month contract with Woodside Petroleum at $285,000 per day. That new contract is a large part of the reason we saw deepwater earnings increase in the quarter.

- In a move similar to its General Electric deal in the first quarter, Diamond signed a joint development project with Trelleborg to develop itsHelical Buoyancy riser technology. This technology reduces vibrations for offshore drilling applications, which helps to reducemaintenancerequirements.

- CFO Gary Krenek retired in May and was replaced by Kelly Youngblood, who spent 28 years at Halliburton before hand.

From the mouth of management

There were some upticks in Diamond's operations this past quarter. Before investors get too excited about the recent quarter, though, CEO Marc Edwards threw a giant bucket of cold water at them as he described what he foresees as a brutal market for offshore drilling in the next couple years.

What a Fool believes

Diamond Offshore is pulling the right levers in this downturn. It's cutting costs and doesn't have a whole lot of capital obligations in the coming quarters to finish building out its fleet. It also has one of the better looking balance sheets in the business that will help it get through this downturn in relatively decent shape. We have yet to see its new equipment deal with General Electric bear fruit, but once that unplanned maintenance is taken care of we should see a decline in operational costs for its ultra deepwater fleet.

As Edwards put it, the market for offshore rigs is absolutely brutal today. For the company, that means batten down the hatches and ride out the storm for a couple more years. For investors, we have the luxury of looking elsewhere for our investments. Perhaps in a couple years when this market rebounds it will be worth taking a look at Diamond as a potential investment. In the meantime, though, it's probably best to wait this one out.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Tyler Crowe owns shares of General Electric.You can follow him at Fool.comor on Twitter@TylerCroweFool.

The Motley Fool owns shares of General Electric and Halliburton. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.