Decoding Blackstone's Dividend

Income investors don't have it easy these days. Bond yields remain low, and many dividend stocks trade at high multiples. One opportunity income-oriented investors may wish to look at is Blackstone (NYSE: BX). In the March 12issue of Barron's, writer Jack Hough wrote that he expects Blackstone units to yield 8% this year with a fair value of $40 per share. This would be an almost 33% increase from today's price of $30.

Why would Blackstone, the leading private equity firm, be undervalued? Barron's suspects public shareholders are turned off by Blackstone's complex operating structure, tax consequences, and hard-to-understand financials. Let's go through these concerns point-by-point. At the end, you'll have a better picture of this high-yielding stock.

One business, four asset classes

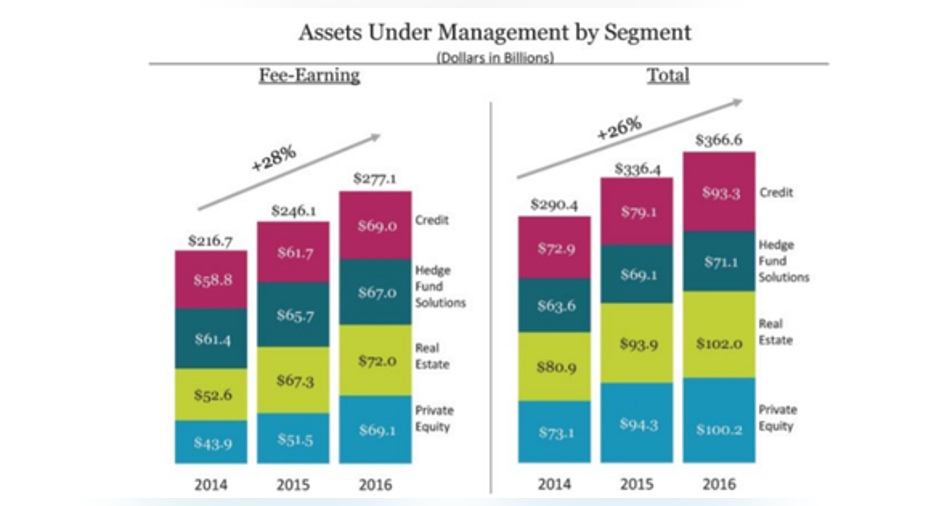

Blackstone is the largest and arguably most successful alternative asset manager in the world. It manages $366 billion in assets under management (AUM) across private equity, real estate funds, hedge funds, and credit funds.

Image source: Blackstone.

Blackstone raises money from limited partners (pension funds, endowments, wealthy family offices), then invests on their behalf in each asset class. Blackstone manages the investments as the general partner over a multi-year period. When you invest in Blackstone's stock, you are investing in this general partner, which takes a management fee (usually 1-2% of assets), plus a cut of the profits (usually 15-20%). Blackstone's general partner can also invest alongside its limited partners, but this is usually under 5% of each fund.

The dividend is robust, but unreliable

Blackstone is run by Steve Schwartzman. Schwartzman had a very tough year in 2016 as his salary was almost cut in half...to only $425 million! Obviously feeling melancholy about his pay cut, he tried to cheer himself up with a birthday party featuring acrobats, Mongolian soldiers, and camels.

Kidding aside, what was the reason for Schwartzman's diminished pay? As founder, Schwartzman owns a large part of the company, and is paid the same way Blackstone unitholders are: in dividends. Dividends of publicly traded alternative managers can vary from quarter to quarter depending on when the company sells its holdings (though rival firm KKR (NYSE: KKR) recently switched to a lower, fixed dividend). This vacillating dividend can turn investors off.

.

Blackstone distributions per unit. Data source: Blackstone SEC filing. Table by author.

2016 had the lowest number of IPOs since the financial crisis, and IPOs are a common "exit strategy" for private equity. Lower exits mean lower distributions, and private equity firms don't have to sell holdings until they get the right price. While this is good for Foolish long-term investors, those hoping for steady income are likely to be turned off.

You are a "unit" holder, not a stockholder

Blackstone equity owners are not stockholders, but unit-holders in a partnership. While income is shielded from most taxes at the company level, distributions require filing a K-1, and may be taxed as ordinary income. Often, the distribution is a combination of interest income, capital gains, and return of capital. Thus, for people in a high tax bracket, or those wishing to avoid tax-preparation headaches and costs, Blackstone may appear to be more trouble than it's worth.

Valuation

With all these moving parts, how does one value Blackstone? While the company must report GAAP income, many analysts use a measure of earnings called economic income, which adjusts for equity compensation to employees (who are paid in Blackstone units for performance)and transaction costs related to acquisitions/disposals. That gives a and idea of how the company is doing purely from an investing perspective. Still, others wish to use distributable earnings, which is essentially valuing the company its current dividend. Finally, others monitor Blackstone's fee-related earnings, which are earnings it makes solely from management fees, which, if the company maintains its assets under management, gives a good baseline for a minimum dividend. The company provides a guide to each measure:

Image source: Blackstone SEC filing.

One can see what each measure translates to in terms of a price to earnings multiple in the table below, based on Blackstone's market cap of $36 billion:

Data source: Blackstone. Table by author.

Blackstone's fee-earnings yield is almost 2.8%. That's pretty strong, considering the 10-year treasury is under 2.5%. Moreover, Blackstone has been a fund-raising machine, increasing its fee-earning assets under management by 12.5% in 2016. If the trend continues, that baseline dividend should keep growing.

Given the performance of the markets since the presidential election, it's also likely that Blackstone will realize more IPO exits than it did in 2016.According to Yahoo! Finance, the average analyst estimate for 2017 earnings is $2.87 per unit. If Blackstone achieves that amount in distributable earnings (some years distributable earnings are greater, some years they are less), and pays 85% out as dividends, which is the company's policy, that would increase the yield to roughly $2.43, per unit, or 8%, as Barron's describes.

That hefty payout, along with Blackstone's leading brand and fundraising prowess, may make it worth the tax headache for yield-hungry investors.

10 stocks we like better than The Blackstone GroupWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and The Blackstone Group wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Billy Duberstein owns shares of The Blackstone Group. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.