Colgate-Palmolive Stock in 5 Charts

Image source: Motley Fool.

Colgate-Palmolive (NYSE: CL) doesn't sound like the most exciting growth stock around. After all, the company makes most of its sales and profits by selling mundane products such as toothpaste, soap, and pet food. Nevertheless, slow and steady sometimes wins the race: Colgate-Palmolive has produced impressive returns for investors over the years, and it still has a lot to offer going forward.

A global market leader

Colgate-Palmolive operates in multiple consumer staples segments, such as shampoo, shower gels, deodorants, and pet food, among several others. However, the lion's share of the business comes from oral care, where Colgate-Palmolive is an undisputed leader on a global scale.

According to management, the company owns 43.9% of the toothpaste market around the world, with a special focus on emerging markets: Colgate-Palmolive has a market share of 73.3% in the Brazilian toothpaste market, 79.9% in Mexico, and it owns 53.4% of the market in India.

Image source: Colgate-Palmolive.

The company is a pioneer when it comes to international expansion. Colgate-Palmolive entered Mexico in 1925, Brazil in 1927, and India in 1937. This first-mover advantage has been enormously beneficial for shareholders; Colgate-Palmolive now has a presence in 223 countries, with more than 75% of sales coming from international markets and over 50% of revenue produced in emerging markets.

Image source: Colgate-Palmolive.

The company has built long-standing relationships with dental care professionals around the world -- Colgate is recommended by 47% of dentists worldwide. This is a major advantage when it comes to brand recognition. Besides, specialized toothpaste generally carries premium prices and above-average profit margins, so Colgate-Palmolive's relationship with dentists has positive implications in terms of profitability, too.

Translating competitive strength into profitability

Solid competitive strengths are the key to sustained profitability over the long term. In addition to brand differentiation, Colgate-Palmolive enjoys cost advantages due to its massive scale and wide geographical reach. Besides, the company has abundant financial resources to invest in key areas such as marketing and advertising or research and development, which sets it apart from smaller competitors trying to steal market share away.

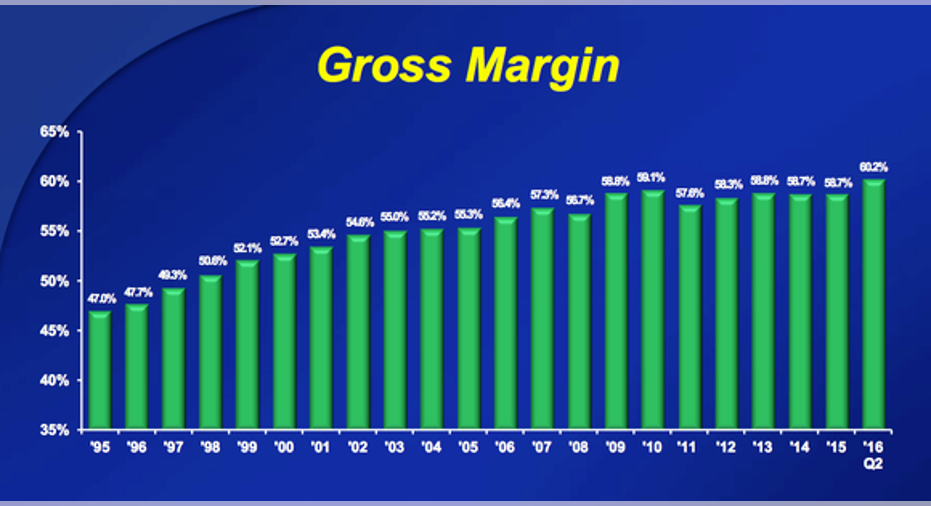

The company is facing economic headwinds in many of the main emerging markets where it operates, but financial performance remains solid as of the second quarter of 2016. Colgate-Palmolive reported a 5.4% increase in organic sales during the period, while adjusted gross profit margin grew 190 basis points year over year, to 60.2% of revenue.

Management is doing a sound job at generating increasing profitability for investors, as gross profit margin is consistently moving in the right direction over the last couple of decades.

Image source: Colgate-Palmolive.

On the back of solid competitive strength and attractive financial performance, the stock has downright crushed the market over time. Over the 20-year period ended in 2015, Colgate-Palmolive has delivered an accumulated total return, meaning dividends plus capital appreciation, of 1,021%, considerably beating both the S&P 500 index and the return offered by companies in its peer group.

Image source: Colgate-Palmolive.

Positioned for dividend growth

High-quality companies in the consumer staples sector typically generate big and consistent cash flows, so they tend to pay generous dividends. In fact, dividends are one of the main reasons why many investors gravitate toward market leaders in different consumer staples categories.

Colgate-Palmolive pays a dividend yield of 2.3% at current prices, which is not particularly high by industry standards. For example, Procter & Gamble (NYSE: PG) is paying almost 3% in dividends, while Kimberly-Clark (NYSE: KMB) offers a dividend yield of 2.9%.

On the other hand, the company has a pristine track record of dividend payments over the long term. Colgate-Palmolive has paid uninterrupted dividends for 122 years in a row, and it has increased dividends in every year over the last 54 consecutive years. Even better, Colgate-Palmolive has outperformed both Procter & Gamble and Kimberly-Clark in terms of dividend growth over the last decade.

CL Dividend data by YCharts.

Wall Street analysts are on average expecting Colgate-Palmolive to make $2.87 in earnings per share during 2016. This puts the dividend payout ratio at nearly 54% versus earnings forecasts for the current year, which is quite a sustainable ratio. As a reference, Procter & Gamble has a dividend payout ratio of 68% of earnings, while Kimberly-Clark offers a dividend payout ratio around 61% versus earnings expectations for 2016.

While Colgate-Palmolive is not the highest-yielding dividend stock in the consumer staples sector, the company doesn't leave much to be desired in terms of dividend growth. Financial performance has been remarkably solid over the long term, and the dividend payout ratio is still comfortably safe. This means that Colgate-Palmolive is in a strong position to continue rewarding investors with consistent dividend growth over the years ahead.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Andrs Cardenal has no position in any stocks mentioned. The Motley Fool recommends Kimberly-Clark and Procter and Gamble. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.