Chevron's Management Just Dropped a Bombshell About Its Future

This has been an interesting time for integrated oil and gas companies lately. These oil behemoths were the ones that had the capital to take on massive projects that take years to develop. With lower prices into their third year and shale emerging as a cheaper source, it is going to significantly change the investment decisions for these companies.

Perhaps it was by accident, but Chevron (NYSE: CVX)CEO John Watson made a small comment during the company's recent conference call that could have huge implications for the oil giant in the coming years. Here's a look at that and several other statements Watson made during the call investors should know more about.

Image source: Chevron.

Shale will play a huge role

Let's cut to the chase here. For a while now, Chevron has been talking about how shale drilling will play a larger role in the company's overall production mix. Almost all of its recent investor presentations have talked about how shale production specifically in the Permian would grow to about 250,000 to 350,000 barrels per day by 2020 depending on oil prices and rates of return.

When asked about Chevron's plans for capital spending in the Permian for the year, Watson talked about Chevron's advantages in the field and its slower approach to figure out the best way to attack this oil patch. What was really surprising was how much he foresees shale adding to the portfolio. Watson said, "In an overall sense, it wouldn't surprise me to see our unconventional activity be 25% of our production by the middle of the next decade."

Based on Chevron's total production of 2.6 million barrels of oil equivalent per day, we're talking about 670,000 barrels of shale production today. We can also assume that many other companies are thinking the same way as Chevron in this regard. If that is the case, then shale is going to be really big for those integrated companies with assets in the right place.

Spending levels stay tight

Part of that large push into shale will shorten the payback period for Chevron's investments. Just a few years back, Chevron was heavily invested in long-term oil and gas projects. So much so that at one point, 40% of its invested capital was in non-producing assets. According to Waston, this will change in the next few years:

Big production bumps coming soon

Also, it's worth noting that many of those decade-long projects are finally coming to fruition in the next year or so. Watson said that means we can expect a pretty large uptick in production for the coming year:

Production growth of 4% to 9% doesn't sound like much, but keep in mind that Chevron produces 2.6 million barrels per day. That means it needs to come up with 130,000 to 260,000 barrels per day of new production on top of the hundreds of thousands of barrels per day that will be lost to natural decline.

Meeting its cash goals

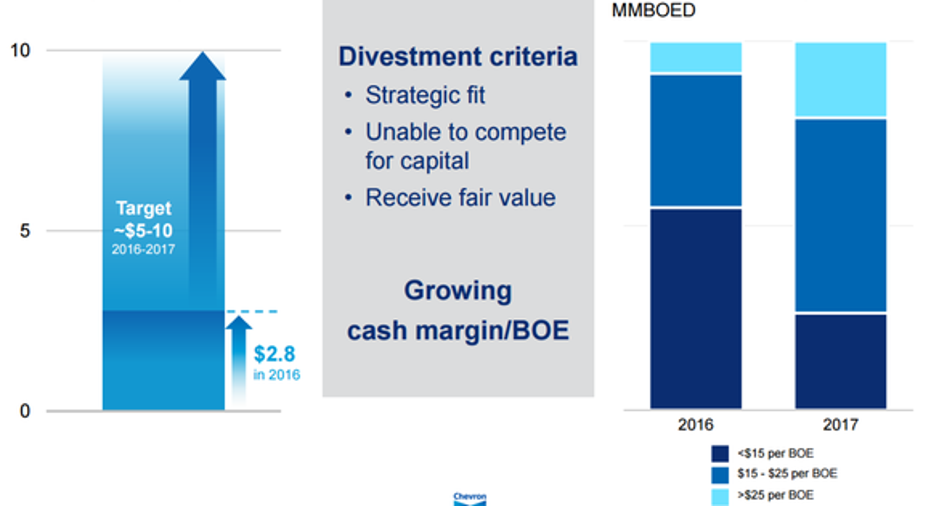

For the past couple years, management has been saying that 2017 would be the year Chevron would generate enough cash flow from operations to cover its capital spending and dividend -- a feat it hasn't achieved in many years. That will involve improving per-barrel cash margins. Part of achieving that goal will be through some asset sales, which Watson said will be $5 billion to $10 billion between 2016 and 2017:

Image source: Chevron investor presentation.

The lack of decline isn't just shale

As oil prices declined, there was an assumption in the industry that production would decline. While we have seen some declines, they haven't been as much as many had expected. The obvious reason for this muted decline is that shale has been able to fill in where others are dropping off. According to Waston, though, it's closer to the truth to look at how much companies have been able to manage the decline at existing conventional assets.

10 stocks we like better than Chevron When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Chevron wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Tyler Crowe has no position in any stocks mentioned. The Motley Fool recommends Chevron. The Motley Fool has a disclosure policy.