Can Advance Auto Parts Really Catch Up to O'Reilly and AutoZone?

The investment idea behind buyingAdvance Auto Parts is based on the belief that the company can play catch-up with rivals such asAutoZone andO'Reilly Automotive . It's an attractive proposition because Advance currently trades at a substantial discount to its peers. In my view, closing the gap could result in a near doubling of the stock price. But can Advance really achieve its aims? Here is what you need to know before buying the stock.

Really, O'ReillyIn a nutshell, Advance's aim should be to replicate O'Reilly Automotive's improvements of the past few years. O'Reilly is a good benchmark because it has a far higher proportion of do-it-for-me (DIFM) sales compared with, say, AutoZone. In addition, O'Reilly built up its DIFM business following the acquisition of CSK Automotive in 2008. CSK wasn't an established DIFM retailer -- on the contrary, its primary end market was DIY, but O'Reilly built out a distribution network allowing the purchased stores to pursue a dual DIY and DIFM market strategy.

In comparison, Advance's early 2014 acquisition of General Parts International, owner of Carquest and Worldpac, immediately gave the company more DIFM sales -- General Parts had 80% of its sales in the DIFM market. The key point is that Advance is following O'Reilly's dual-market strategy, reaching the same endpoint from a different angle.

A breakout of each company's sales:

SOURCE: COMPANY PRESENTATIONS.

There are three key distinctions between DIFM and do-it-yourself (DIY).

- Advance's management believes that DIFM is growing three times faster than DIY.

- Advance is moving toward the mixed-model (DIFM and DIY from the same store) that O'Reilly did a few years ago.

- DIFM is likely to be more capital intensive as commercial customers require parts immediately, meaning that Advance could need to invest in distribution centers to ensure daily replenishment of parts.

Where O'Reilly leadsTo understand what Advance needs to do, let's look at what O'Reilly has done and, in passing, look at where Advance has been left behind in recent years. First, I'll start with the EBITDA margin.

O'Reilly's margin took a hit after the 2008 acquisition of CSK, and similarly Advance's has come under pressure as it integrates Carquest and Worldpac. Clearly, creating a dual-market model doesn't come without teething problems. However, O'Reilly's margin has improved dramatically from 2010, and Advance's management is aiming for an operating margin equivalent to 15% EBITDA margin by 2017.

AAP EBITDA Margin (TTM) data by YCharts.

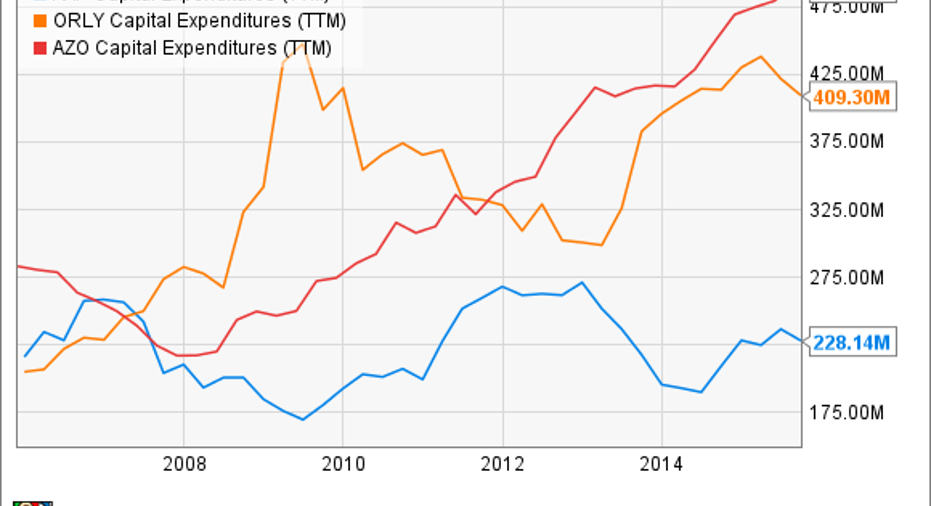

Second, there's no doubt that O'Reilly's purchase of CSK led to increased capital spending -- partly on building out a distribution network.

AAP Capital Expenditures (TTM) data by YCharts.

However, the extra investment was worthwhile, as O'Reilly's return on invested capital (ROIC, which is net operating profit less taxes, divided by invested capital) has increased markedly, while Advance's has floundered. AutoZone's ROIC increased because of the post-recession popularity of DIY.

AAP Return on Invested Capital (TTM) data by YCharts.

Working capital managementThird, Advance needs to improve its working capital management. For example, let's take a look at receivables turnover (net receivable sales divided by average net receivables). It's a measure of how well a company is collecting cash from sales made, and a high number is good. Again, note O'Reilly's improvement while Advance has floundered.

AAP Receivables Turnover (TTM) data by YCharts.

Valuation mattersThe preceding analysis goes some of the way toward demonstrating the feasibility that Advance can improve its operational metrics in building out a dual-market model -- not least because O'Reilly already did it. Moreover, if Advance hits its 12% EBIT margin target (around 15% EBITDA margin), the stock will look cheap.

Analysts have revenue coming in at $9.94 billion in 2016, and a 15% EBITDA margin would generate $1.49 billion in earnings before interest, taxes, depreciation, and amortization. Based on the current enterprise value (EV, which is market cap plus net debt) of $13.14 billion, the stock would then trade at a forward EV/EBITDA multiple of 8.8 -- O'Reilly currently trades on a multiple of almost 1.9 times this figure, suggesting Advance's stock could perhaps double in the future.

AAP EV to EBITDA (TTM) data by YCharts.

All told, there's no guarantee that Advance will hit its targets, and recent results have demonstrated its difficulty in integrating Carquest. However, the case for the stock is attractive, and O'Reilly's experience suggests Advance could achieve its aims.

The article Can Advance Auto Parts Really Catch Up to O'Reilly and AutoZone? originally appeared on Fool.com.

Lee Samaha has no position in any stocks mentioned. The Motley Fool owns shares of O'Reilly Automotive. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.