Better Buy: Silver Wheaton Corp. vs. Barrick Gold Corp.

Should you buy a gold-focused stock or a silver-focused stock? Image Source: Getty Images

I don't remember the last time metals and mining stocks were this alluring. Companies like Barrick Gold (NYSE: ABX) and Silver Wheaton (NYSE: SLW) have seen share prices shoot through the roof, more than doubling year to date. The Fed's decisions to keep interest rates low and steady gave precious metals a shot in the arm even as uncertainty in China and Europe continue to add to the appeal of gold and silver as safe-haven investments.

While those factors might push Barrick and Silver Wheaton still higher, which stock is a better buy today? It's a tough, yet an intriguing comparison.

Similar, yet so different

You know that Barrick and Silver Wheaton both make money by selling precious metals, but do you know how different their businesses models are? While Barrick is a traditional miner that extracts metals to sell later. Silver Wheaton buys bullion streams other from miners at low prices instead of extracting its own metals. Why would a miner sell its produce to Silver Wheaton, you may ask? Good question!

The mining business is extremelycapital intensive. Silver Wheaton finances miners' projects up front, and in return, secures the right to purchase silver and gold from them at a lower fixed price.

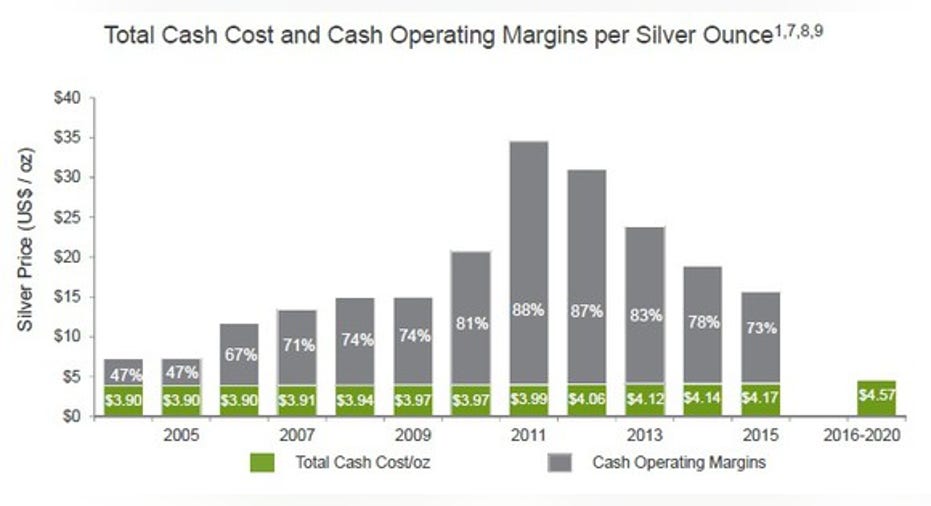

This unique business model leverages Silver Wheaton to metal prices like Barrick, but at much lower risks and costs, as it doesn't have to incur the humongous expenses associated with exploration, operation, and maintenance of mines. Moreover, as silver these days is essentially a byproduct of mining other minerals (primarily copper, zinc, lead and gold), Silver Wheaton can procure the metal from miners as insanely low costs. Its average purchase cost is only about $5 per ounce of silver. Comparatively, a silver miner like Coeur Mining (NYSE: CDE) spent $10.15 per ounce of silver in cost of sales last quarter. Not surprisingly, Silver Wheaton's margins are mind-boggling.

Source: Silver Wheaton's August 2016 Investor presentation.

Silver Wheaton wins with gold too; its purchase cost averages only about $400 per ounce. Barrick's all-in sustaining costs (AISC) came in at around $782 per ounce last quarter. No prizes for guessing which company enjoys higher margins.

SLW Operating Margin (Annual) data by YCharts

Barrick is no less

That's not to say Barrick is a loser. On the contrary, Barrick is a top choice if you're seeking exposure to gold, thanks to its solid cost advantage: With an AISC below $800 per ounce, Barrick is at the lowest end of the industry cost curve. Rivals like Goldcorp (NYSE: GG) have a lot of catching up to do: Goldcorp's AISC was above $1,000 per ounce in the second quarter.

Barrick isn't resting on its laurels, though. It has set a goal of getting its AISC below $700 per ounce by 2019, backed by aggressive restructuring, deleveraging of its balance sheet, and prioritizing of capital projects. If gold continues to rally as Barrick brings down costs, it should be able to grow its operating profits and cash flows substantially in coming years. In fact, Barrick has absolutely crushed Silver Wheaton when it comes to free cash flow growth.

ABX Free Cash Flow (TTM) data by YCharts

2015 was a remarkable year for Barrick as it cut losses and lowered capital expenditures to boost cash flows. Barrick is confident of staying FCF positive if gold stays above $1,000 per ounce, which, in current scenarios, should rule out the possibility of further dividend cuts. Barrick's annual dividend is down almost 80% since 2013.

Silver Wheaton's annual dividend has also almost halved since 2013, but it's important to note that the company doesn't pay out a fixed amount every quarter. Instead, its quarterly dividend equals 20% of the average operating cash flows generated in the last four quarters. So while Silver Wheaton's dividends can fluctuate, it doesn't pinch as much as a steep dividend cut like Barrick's, making the latter a riskier stock.Their current yields are nothing to write home about, but Silver Wheaton's 0.72% yield still beats Barrick's barely there 0.4% yield.

And the winner is...

Of course, I wouldn't dig for dividends in the mining industry given the volatile nature of the business, but if I had to choose between Barrick and Silver Wheaton, I'd bank on the latter in the long run, given its low-risk business model. While Barrick is trying hard to break its streak of losses since 2012, Silver Wheaton has been profitable in four out of past five years. That closes the case for me: I'd choose Silver Wheaton over Barrick today to play along with rising precious metals prices.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Neha Chamaria has no position in any stocks mentioned. The Motley Fool owns shares of Silver Wheaton. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.