Better Buy: Chuy's Holdings Inc vs. Zoe's Kitchen Inc

Image source: Chuy's Holdings

Full-service Tex-Mex restaurant chain Chuy's Holdings (NASDAQ: CHUY) and fast-casual Mediterranean chainZoe's Kitchen (NYSE: ZOES) share many characteristics. Both are in rapid expansion mode, attempting to double their store counts by 2020. Both boast solid restaurant-level profits. And both have impressive same-store-sales growth streaks of more than six years that have been immune (so far) to falling traffic at restaurants across the U.S.

Let's take a closer look at how the two companies compare and see which one is more deserving of your investment dollars today.

Image source: Zoe's Kitchen

Store expansion will provide impressive growth

Chuy's currently operates 80 restaurant units, while Zoe's has just over 200. And, as mentioned, both companies have committed to doubling their number of locations by the end of 2020. (For Chuy's, this goal was announced at the end of 2015, when it had 69 locations.) This should lead to significant revenue growth in the years ahead.

| Metric | Chuy's | Zoe's |

|---|---|---|

| Projected total stores (end of 2020) | 138 | 400 |

| Average revenue/store (annual) | $4.7 million | $1.6 million |

| Projected 2020 revenue | $649 million | $624 million |

| 2015 revenue | $287 million | $226 million |

| Projected 2015 to 2020 revenue CAGR | 18% | 23% |

CAGR = compound annual growth rate. Data sources: company information. Projections and table by author. Data source: Company presentations.

Please note that the above table assumes that average revenue per store remains constant and does not account for any further comparable sales growth. One additional consideration here is that Chuy's has left open the possibility that it will reach its store doubling goal as early as the end of 2018. If the company were able to pull that off, its three-year compound annual growth rate (CAGR) for revenue would be around 31%. For additional context, from 2011 through 2015, Chuy's CAGR for revenue was 22%, while Zoe's clocked in at a 47% CAGR over the same period. For the purpose of discussion, though, I'm sticking with the original projections from the table. It seems fairly clear that Zoe's has been on a faster growth trajectory, and will likely remain a faster grower for now.

Advantage: Zoe's Kitchen.

Attractive restaurant-level metrics

Building new restaurants figures to be highly profitable for both chains. Here is a comparison of each company's long-term targets for new stores:

| Company target | Chuy's | Zoe's |

|---|---|---|

| Revenue/store (annual) | $3.75 million | $1.5 million |

| EBITDA margin | 15.75% | 18% |

| EBITDA/store (annual) | $0.6 million | $0.27 million |

| Cash investment | $2 million | $0.75 million |

| Cash-on-cash return | 30% | 30% |

EBITDA = earnings before interest, taxes, depreciation, and amortization. Data source: company presentations. Table by author.

New stores for Chuy's cost an average of $2 million to build, while for Zoe's they cost $750,000. And while Zoe's has higher EBITDA margin targets, Chuy's model makes up the difference with much higher estimated revenue per store, resulting in roughly equal cash-on-cash returns for both companies. (Cash-on-cash return is restaurant-level EBITDA divided by net cash investment excluding pre-opening expense.)

We should note that both Chuy's and Zoe's regularly see established restaurants outperform these targets, but going strictly by the targets themselves, I'm going to call this a draw.

Advantage: None.

Comparing valuations is not so clear

Chuy's total market cap is around $490 million. The company has roughly $14 million in cash and no debt, and plans to fund all of its own expansion for the foreseeable future.

Zoe's market cap is $423 million. It has $10 million in cash, with around $28 million in long-term debt.

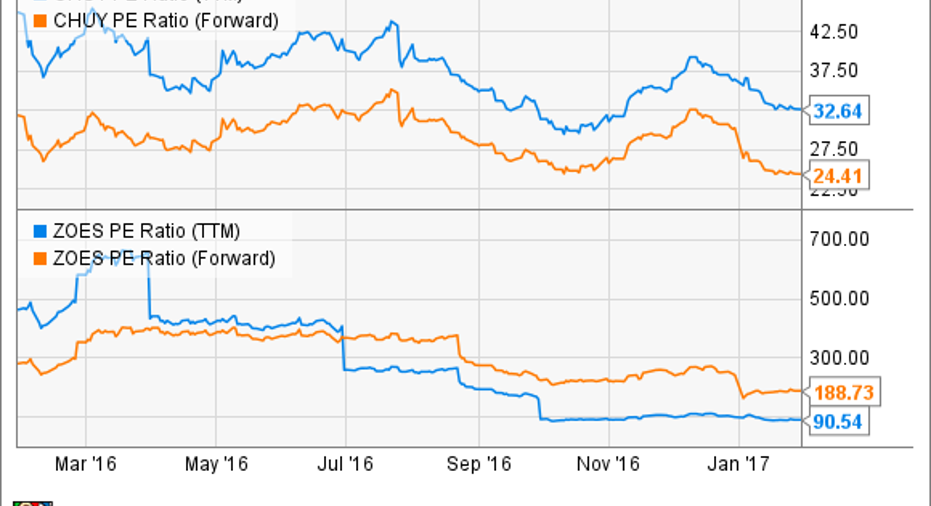

Here's where the comparison starts to get a little trickier. Restaurant companies are normally fairly easy to value using basic price/earnings ratios. And Chuy's P/E ratio of around 32 (and forward P/E of around 24) look pretty reasonable to me for a company I expect to continue growing both revenue and EBITDA by 20% or more per year.

CHUY PE Ratio (TTM) data by YCharts

However, Zoe's is in a bit of a strange position as it it still transitioning from negative to positive earnings growth, causing the stock to look quite expensive on a P/E basis. (Zoe's P/E is around 90.) But with a rapidly increasing store count, plus the company's belief that it can achieve 2% to 4% yearly comparable sales growth and more than 20% annual EBITDA growth, the company appears to be on the path to sustained -- and increasing -- profits. This should have the effect of pulling Zoe's valuation into a more moderate range soon.

When P/Es are not useful, it can be more helpful to look at price/sales ratios. Chuy's P/S ratio is around 1.5, while Zoe's is 1.6. On a forward P/S basis, both companies are on near-equal footing.

CHUY PS Ratio (TTM) data by YCharts

This is almost too close to call. But based on a better cash/debt situation, a slightly lower P/S ratio and a forward P/E ratio that's looking pretty darned appetizing, I'm going with Chuy's this round.

Advantage: Chuy's.

The winner: Chuy's, by a nose

Given the multiyear runways for growth and increasing profits at both companies, this is a tough decision. However, while I believe that both restaurant chains make for compelling long-term investments, I'm giving the slight edge to Chuy's as the better stock to buy right now.

10 stocks we like better than Chuy's Holdings When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Chuy's Holdings wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Andy Gould owns shares of Chuy's Holdings and Zoe's Kitchen. Andy Gould has the following options: short April 2017 $30 puts on Chuy's Holdings, short January 2018 $30 puts on Zoe's Kitchen, and long January 2018 $30 calls on Zoe's Kitchen. The Motley Fool owns shares of and recommends Chuy's Holdings and Zoe's Kitchen. The Motley Fool has the following options: long April 2017 $28 puts on Chuy's Holdings. The Motley Fool has a disclosure policy.