Apache Corporation in 6 Charts

Image source: Apache Corporation.

Apache (NYSE: APA) has undergone a dramatic shift over the past few years going from a somewhat bloated global oil giant to a lean and focused company. That is evident by looking at the progress it made in several key areas. As a result, Apache is in a solid position to weather the current oil market downturn and capture opportunities when market conditions improve.

The evolution of Apache

A couple of years ago Apache made the strategic decision to pivot its portfolio away from riskier projects to improve its returns. That transition resulted in the company jettisoning $10.5 billion in assets primarily consisting of long-cycle projects such as deepwater and LNG assets as well as some of its international assets:

Source: Apache Corporation Investor Presentation.

Its intention was to reduce its overall risk, in particular by cutting out projects that had a higher probability of cost overruns or of drilling dry holes. Instead, the company wanted to focus its investments on shorter cycle projects that have a high likelihood of success, such as unconventional shale plays. As a result, the company now has strong positions in the Permian Basin and Mid-continent that will be the focus of its investments going forward.

Removing the weight of debt

In addition to reinvesting a portion of its asset sale proceeds to grow production out of its North American shale plays, Apache paid down a substantial amount of debt in recent years:

Source: Apache Corporation Investor Presentation.

As that chart shows, Apache's net debt is down 36% over the past year. That put the company on very solid ground, enabling it to manage through the downturn without having to worry about managing its balance sheet. This turned out to be a critical competitive advantage. For example, rival Anadarko Petroleum (NYSE: APC) had to issue $3 billion of new bonds in the second quarter to refinance debt maturing in 2016 and 2017. Anadarko Petroleum did so to remove "received uncertainty" that it would not be able to refinance debt when it came due. Given that Apache has no near-term debt maturities, there is no uncertainty surrounding its balance sheet.

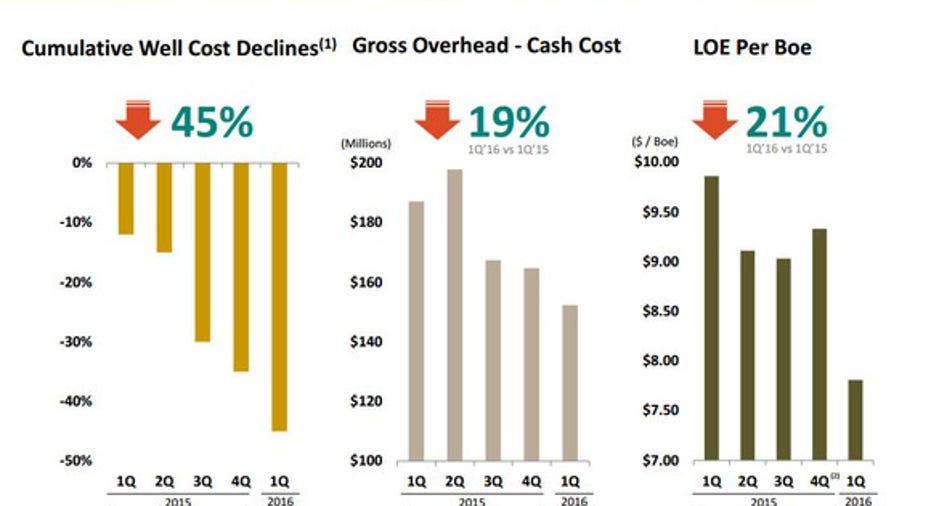

The dramatic drop in costs

Because Apache did not have to focus any attention on bolstering its balance sheet, it was able to focus entirely on reducing its costs. As these next three charts show, the company's cost structure has dramatically improved over the past year.

Source: Apache Corporation Investor Presentation.

Gross overhead cash-cost and LOE per BOE are both production costs. Driving these costs down are important because it mutes some of the impact of low oil prices on cash flow. While the company was not able to completely mitigate that impact, dropping its production costs by roughly 20% did offset a portion of the oil price impact.

Just as importantly, the company was able to push its completed well costs down by a stunning 45%. Because of that, the company can drill more wells with the same amount of money. The three factors driving down well costs are in the following chart:

Source: Apache Corporation Investor Presentation.

What's worth noting is that, unlike the decline in production costs, which are most likely temporary, about 45% of Apache's well cost savings are structural in nature. What that means is that these cost reductions are immune to the inflationary cost pressures of rising oil prices. In other words, when oil rebounds in the future it will allow oil-field service companies to start raising prices for their services. However, even if service costs went back to their 2014 level, it would only result in Apache's well costs rising slightly because it permanently removed costs through efficiency gains and design changes. What that means is that when oil prices improve, Apache's drilling returns will zoom higher because of these permanent changes to its cost structure.

Investor takeaway

Apache is not the same company it was a couple of years ago. Instead of being a diversified global giant like Anadarko Petroleum, Apache's focus is shifting toward U.S. shale. That focus puts it in the position to thrive because it has ample financial capacity and a much-improved cost structure to drive high return production growth once oil prices improve.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Matt DiLallo has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.