An Overview of Bank of America's First-Quarter Earnings

Image source: iStock/Thinkstock.

Revenue and earnings fell at Bank of America in the first quarter, as depressed trading activity overpowered lower expenses and an improved performance in its consumer bank. The nation's second-biggest bank by assets nevertheless exceeded analyst expectations, sending its shares higher for a second day in a row.

For the three months ended March 31, Bank of America reported $19.5 billion in revenue and earnings applicable to common shareholders of $2.2 billion. That compared to revenue of $20.9 billion and earnings of $2.7 billion in the year-ago period.

Multiple banks made it clear over a month ago that revenue and earnings were likely to be down in the first three months of the year. Concerns about China, as well as the upcoming vote in the United Kingdom to part ways with the European Union, led to heightened volatility in global markets and depressed trading profits.

Citigroup had estimated that trading revenue would be down by 15%, while JPMorgan Chase expected it to drop by 20%. The results thus far haven't been as dire. JPMorgan Chase said yesterday that its trading revenue was 11% lower on a year-over-year basis, though Bank of America's trading profits dropped by 16%.

Low oil and gas prices are also contributing to increased losses from energy-related loans. You can see this by looking at banks' loan loss provisions, which reflect funds set aside in anticipation of future loan losses. Bank of America reserved $997 million in the first quarter of the year compared to $765 million in the same period in 2015. This was driven by a $457 million increase in energy-related loan loss provisions, partially offset by lower credit expenses in its consumer bank.

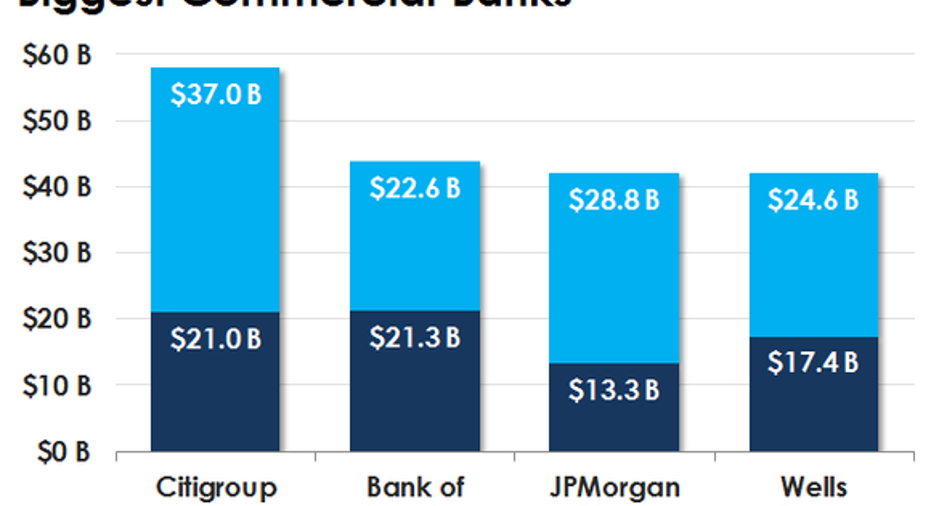

Data source: JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup. As of Dec. 31, 2015.

Low interest rates also continue to weigh on bank earnings. Bank of America's net interest margin, which measures how much a bank earns on its portfolio of loans and securities, fell to 2.05% from 2.16% last year. That alone equates to a year-over-year decrease of roughly $500 million in pre-tax earnings. To put the significance of low interest rates into perspective, if Wells Fargo generated the same net interest margin last year that it did in 2007, the California bank would earn upwards up $20 billion more a year in after-tax net interest income.

These factors caused analysts to continually drop their forecasts for Bank of America's earnings over the past year. Three months ago, analysts expected the $2.2 trillion bank to earn $0.32 per share. That had fallen to only $0.20 per share on the eve of earnings season. Like JPMorgan Chase yesterday, Bank of America narrowly beat this, producing earnings of $0.21 per share. The market responded positively in both cases, sending shares of Bank of America and JPMorgan Chase higher after they reported their respective results.

You can get a sense for Bank of America's strengths and weaknesses in the first quarter by looking at the performance of its various business segments, which are included in the table below.

|

Segment |

Q1 2016 Net Revenue |

Q1 2015 Net Revenue |

Change (YOY) |

|---|---|---|---|

|

Consumer Banking |

$7.65 billion |

$7.41 billion |

3.2% |

|

Wealth Management |

$4.45 billion |

$4.52 billion |

(1.5%) |

|

Global Banking |

$4.39 billion |

$4.40 billion |

(0.2%) |

|

Global Markets |

$3.95 billion |

$4.19 billion |

(5.7%) |

|

Legacy Assets & Servicing |

$679 million |

$914 million |

(25.7%) |

Data source: Bank of America's Q1 2016 financial supplement, page 15.

As you can see, Bank of America's biggest division, its consumer bank, saw revenue rise on a year-over-year basis thanks in large part to loan and deposit growth. "As always, we are focused on loan and deposit growth and managing expenses," said chairman and CEO Brian Moynihan in prepared remarks. "By doing that, we continue to improve on what we do best: helping consumers live their financial lives and helping businesses grow and employ more people."

The decline in trading revenue is contained in the 5.7% revenue decrease in Bank of America's global markets segment. And the drop in wealth management revenue stemmed similarly from heightened volatility in global markets, which weighed on transactional activity.

There's no getting around the fact that it was a tough quarter for Bank of America, as well as the nation's other big banks. It produced a return on average assets of only 0.50%, which is half that of the standard industry benchmark of 1%. At the same time, however, its shares trade for a 40% discount to book value, which is substantial by any measure and, in my opinion, more than offsets the profitability issues that the North Carolina-based bank will continue to face until interest rates move higher.

The article An Overview of Bank of America's First-Quarter Earnings originally appeared on Fool.com.

John Maxfield owns shares of Bank of America and Wells Fargo. The Motley Fool owns shares of and recommends Wells Fargo. The Motley Fool has the following options: short May 2016 $52 puts on Wells Fargo. The Motley Fool recommends Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.