A Strong Case for Buying Bank of America and Citigroup Stock

Bank of America's headquarters in Charlotte, North Carolina. Image source: iStock/Thinkstock.

If you're in the market for a bank stock, then I encourage you to take a look at Bank of America and, to a lesser extent, Citigroup . I've argued this multiple times in the past, but a recent analysis by Richard Bove of Rafferty Capital Markets does a particularly good job illustrating the bull case for these stocks.

Bove's thesis is that there is a strong correlation between a bank's valuation and whether or not its return on equity, which is a popular profitability metric in the bank industry, exceeds its cost of capital, which measures how much it costs a bank to issue equity. If a bank's return on equity exceeds its cost of capital, then it's creating value for shareholders. And if a bank is creating value for shareholders, then it's much more likely that its shares will trade for a premium to book value.

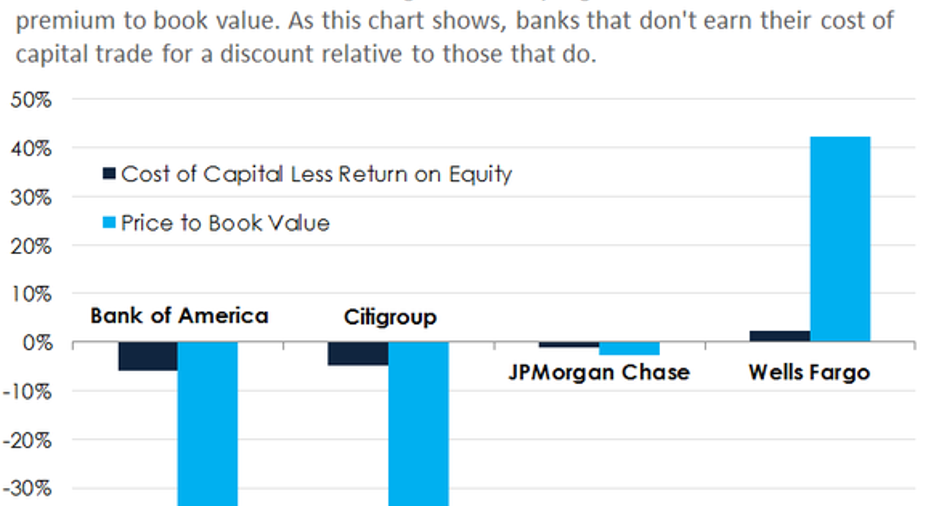

You can see this in the chart below, which shows the difference between the cost of capital and the return on equity relative to the price to book value ratio of the nation's four biggest banks: JPMorgan Chase , Bank of America, Wells Fargo , and Citigroup.

Data source: Dick Bove, Rafferty Capital Markets.

This chart shows us that the cost of capital at Bank of America, Citigroup, and JPMorgan Chase exceeds their returns on equity. In Bank of America's case, its cost of capital is 12.2% while its return on equity is only 6.3%. Its cost of capital thereby exceeds its return on equity by 5.9 percentage points. In Citigroup's case, its cost of capital exceeds its return on equity by 4.9 percentage points. The margin at JPMorgan Chase is smaller -- only 1.2 percentage points -- but the deficit is still present.

Meanwhile, shares of all three banks currently trade for discounts to book value. And, importantly, the size of the discount is proportional to the difference between cost of capital and return on equity. Bank of America has the biggest gap between capital costs and profitability, and it also trades for the biggest discount to book value. Alternatively, JPMorgan Chase has the smallest gap and the smallest valuation discount.

The situation with respect to Wells Fargo is the opposite. It consistently generates a return on equity figure that exceeds its cost of capital, and its share consistently trade for a premium to book value. According to Bove's math, Wells Fargo's return on equity exceeds its cost of capital by 2.3 percentage points, while its shares are priced at a 42.3% premium to book value.

Here's what this shows us: Once Bank of America and Citigroup's profitability improves to the point at which they exceed their respective costs of capital, it's safe to assume that their shares will also, like Wells Fargo's, trade for a premium to book value. Call me nave, but I believe we'll see this happen at some point in the next two or three years. And when you consider the size of the valuation discounts, it certainly seems like there's a lot of upside associated with owning shares of Bank of America and, based on valuation alone, Citigroup.

The article A Strong Case for Buying Bank of America and Citigroup Stock originally appeared on Fool.com.

John Maxfield owns shares of Bank of America and Wells Fargo. The Motley Fool owns shares of and recommends Wells Fargo. The Motley Fool has the following options: short May 2016 $52 puts on Wells Fargo. The Motley Fool recommends Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.