A Serious Risk for Apple Supplier InvenSense Inc

InvenSense provides the motion processor for the iPhone SE. Image credit: Apple.

Shares of motion processor specialist InvenSense hit a new all-time low in the May 13 trading session, extending its post-earnings losing streak. Although the company's near-term financial performance has been quite disappointing (and this is putting it mildly), a longer-term risk looms.

A note on operating expenses

Generally speaking, companies tend to try to find an "optimal" operating expense point. Companies, particularly technology companies in fast-paced industries, need to constantly invest today in developing new products and technologies in order to have things to sell tomorrow.

However, at the same time, companies also need to make sure that their businesses can deliver solid, and growing, profits to stockholders.

A good way to do things is to scale up operating expenses with revenues; if revenues are surging and management has reasonable confidence that growth will continue, then investing more is probably the right thing to do. If revenues are on the decline, then it may make more sense for companies to focus on a few, high-priority projects with the best chance of out-sized returns on investment.

With that background in place, let's take a look at InvenSense's "problem."

Operating expense scaled up with revenue, but revenues now on the decline

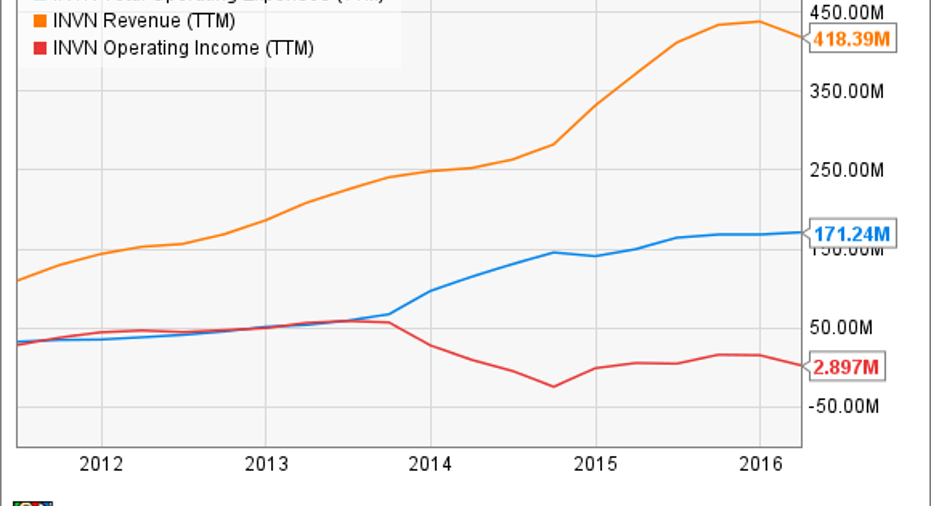

Take a look at the following chart, which includes InvenSense's trailing twelve month revenue, operating expenses, and operating income over the last several years:

Image credit: YCharts.

Notice that early on, InvenSense was able to scale operating expenses nicely with revenue and was ultimately able to generate reasonable amounts of operating income. However, in late 2013/early 2014, InvenSense's operating expenses turned sharply upwards -- likely bolstered by the confidence that management had in the impending Apple -related revenue ramp that it would enjoy during the second half of 2014 and throughout 2015.

InvenSense's operating income did contract significantly, though, as the Apple-related revenue was at materially lower gross profit margins than its other revenue (not unexpected for volume purchases).

At any rate, InvenSense is now at a much higher operating expense run rate than it was just a couple of years ago. This would be fine if revenue continued to grow, but the company is seeing the exact opposite: revenue contraction.

Last quarter, InvenSense reported a year-over-year revenue decline of nearly 20% and, based on its guidance, it could see somewhere close to a 40% year-over-year decline in the current quarter. The decline seems to be based on significant cutbacks from Apple, severe share loss at Samsung , and a generally weak high-end smartphone market (to which InvenSense is quite exposed).

As far as operating expenses go, InvenSense is guiding to a $2 million decline from the prior quarter, which CFO Mark Dentinger says is "in part because [the fourth quarter] contains an extra week and [the first quarter] does not."

In other words, InvenSense isn't guiding to materially lower operating expenses even as its business contracts significantly.

Revenues need to grow again ... or operating expenses need to come down

InvenSense doesn't face any near-term liquidity issues; it has around $284 million in cash, cash equivalents, and short term investments against $151 million in long term debt for a net cash position of about $133 million.

InvenSense can withstand a good deal of cash burn before things get too ugly. However, I don't think that investors are going to be all that happy if InvenSense doesn't act fairly quickly to adjust its operating expenses to what the business environment over the next couple of years could very well look like.

The article A Serious Risk for Apple Supplier InvenSense Inc originally appeared on Fool.com.

Ashraf Eassa has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Apple and InvenSense. The Motley Fool has the following options: long January 2018 $90 calls on Apple and short January 2018 $95 calls on Apple. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.