A Closer Look at Kimberly-Clark Corp.'s Dividend

Kimberly-Clark (NYSE: KMB) shareholders underperformed the market last year as the consumer products giant missed its growth targets. The owner of hit global brands like Huggies and Kleenex kept up its market-thumping dividend, though, and in fact boosted its payout at a faster rate than in the previous year.

Below, we'll look at the key metrics supporting Kimberly-Clark's dividend to see what income investors can expect from the company in the years ahead.

Longevity

With 45 consecutive years of hikes under its belt, Kimberly-Clark has one of the longest-running dividends on the market. Rival Procter & Gamble (NYSE: PG) is the sector leader on this score thanks to its 60 straight years of raises. That's really a testament to the incredible operating stability that comes from owning a diverse group of popular consumer staples.

Image source: Getty Images.

The past year was an unusually rough one for the industry. The sales environment was marked by near-zero growth in developed markets and economic disruption in many developing areas around the world. Yet Kimberly-Clark's organic revenue still ticked up by 2% as earnings rose 5% to $6.03 per share. Shareholders would have preferred to see more robust gains, but they were at least reassured that their company can generate profit growth even in less-than-ideal business conditions.

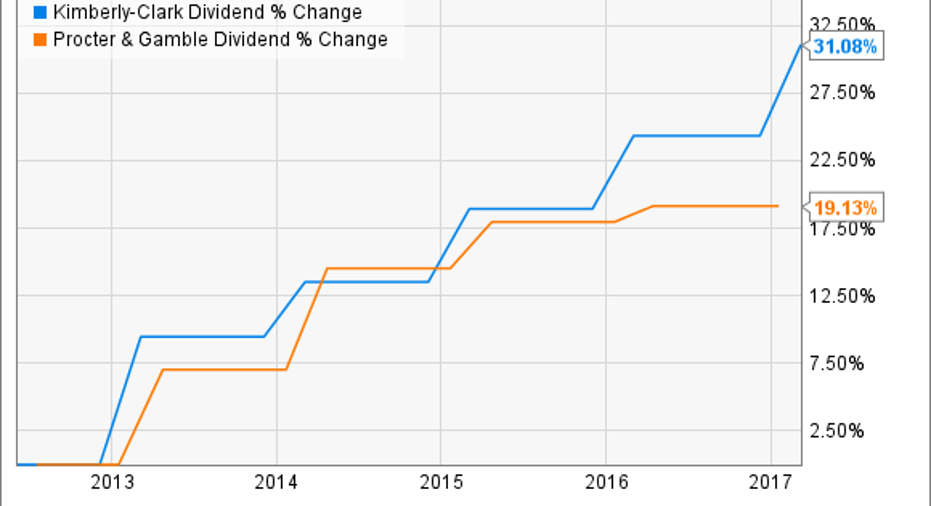

Generosity

In January, Kimberly-Clark boosted its dividend by 5.4% for 2017. Its prior three raises were 4.5%, 8.1%, and 4.8%.

KMB Dividend data by YCharts.

In contrast, P&G has been less generous to income investors, choosing to raise its dividend by just 1% last year, 3% in 2015, and by 7% in each of the prior two years. The two companies currently pay about the same 2.9% annual yield.

Kimberly-Clark prizes dividend payments over stock repurchase spending, while its larger rival does the opposite. It spent twice as much on dividends last year as it did on buybacks. Over the longer term, Kimberly-Clark has delivered at least $2 billion to shareholders in each of the last six years, with just over half of that total going to dividend payments.

Outlook

P&G could start closing the dividend growth gap with Kimberly-Clark now that its brand-shedding initiative has pushed its payout ratio back down below 50% of trailing earnings. Kimberly-Clark doesn't currently plan to raise cash by selling off big pieces of its business, and so the size of its future dividend raises will be driven by two factors: sales growth and efficiency gains.

Image source: Getty Images.

It's impossible to predict whether the industry will slink along at near-zero overall growth, slow further, or speed back up to a robust pace. Shareholders have good visibility into Kimberly-Clark's cost-cutting programs, though.

The company slashed expenses last year and made solid improvements to its working capital, which contributed to impressive gains in key efficiency metrics. Return on invested capital jumped to 23.9% of sales from 22.7%, adjusted operating profit rose by more than a full percentage point to 18.4%, and cash flow surged by 40% to $3.2 billion.

These factors point to steady profit growth over the next few years, but shareholders aren't likely to see the same aggressive gains they witnessed last year. Cash flow will just barely tick higher, the company has forecast, and earnings should rise by 4% at the midpoint of guidance, compared to last year's 5% gain.

Thus, at least until the industry begins expanding rapidly again, Kimberly-Clark's dividend increases are likely to stay in the 3% to 5% range, representing above-average growth that's just a bit below what income investors have seen from the company in recent years.

10 stocks we like better than Kimberly-ClarkWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Kimberly-Clark wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Demitrios Kalogeropoulos has no position in any stocks mentioned. The Motley Fool recommends Kimberly-Clark. The Motley Fool has a disclosure policy.