7 Top Stocks Long-Term Investors Should Buy Next

Image source: Getty Images

If one of your resolutions for 2016 was to be a better investor and outperform the stock market, it's likely you fell short of expectations. Last year, the S&P 500 provided investors a 12% return, with a significant percentage of gains coming after the Nov. 8 presidential election. However, a report from investing-based social media network Openfolio found the average investor significantly underperformed the broader markets, achieving only a 5% gain.

Here at The Motley Fool, we have a mission to help investors find stocks that will help them beat the market -- because if you can't, you're better off in index funds. With that in mind, we asked seven Motley Fool contributors for their best stock recommendation -- not just to get your portfolio in shape for the upcoming year, but for the next decade. Their picks are First Solar (NASDAQ: FSLR), Concho Resources (NYSE: CXO), Under Armour (NYSE: UA) (NYSE: UAA)Mastercard (NYSE: MA)General Electric (NYSE: GE),Boston Beer Company (NYSE: SAM), and Chart Industries (NASDAQ: GTLS). They explain the rationales below:

It's time to flip the switch

Sean Williams (First Solar): Patient investors who have time on their side would be wise to not overlook solar panel manufacturer First Solar (NASDAQ: FSLR), though it had an abysmal 2016.

The solar industry tends to benefit when crude oil and natural gas prices are high, because it provides a sense of urgency for utilities, businesses, and consumers to switch to solar. However, lower fossil fuel prices in recent years have reduced that urgency and hampered demand. By a similar token, Donald Trump's winning the presidency was viewed as a negative for the renewable energy industry. Trump has plans to promote domestic oil and gas production, which is naturally viewed as a knock against alternative energy.

Despite these concerns, First Solar looks poised for a strong rebound in 2017 and beyond. To begin with, it has the strongest balance sheet of all publicly traded solar companies. It's on track to end the year with roughly $1.4 billion in net cash, which would represent about 40% of its current market value, while most of its peers are buried under mountains of debt. The greater flexibility that provides First Solar will allow it to better adapt to changing market conditions and survive downtrends.

Though the company's recently announced restructuring -- which will cost around $600 million at the midpoint and see a quarter of its workforce laid off -- wasn't well-received by Wall Street, the actual details behind its plans make perfect sense. Its choice to abandon its Series 5 products before their rollout -- they wouldn't have made much sense given falling photovoltaic pricing -- means the company can go all-in on its more cost-efficient Series 6 products. Analysts estimate that costs to produce the Series 6 products could be about 40% lower, meaning better margins for First Solar. The Series 6 products won't deploy until 2018, meaning investors will have to be a bit patient to reap the rewards of First Solar's more efficient technology, but those investors who buy in ahead of the curve are liable to be the ones netting the best returns.

The next great oil stock

Matt DiLallo (Concho Resources): Concho Resourcesjust might be the best-kept secret in the oil market. The oil and gas producer controls a vast land position inTexas and New Mexico's Permian Basin, which is one of the top oil plays in the world. In fact, Concho estimates that there are 5 billion barrels of oil equivalent resource potential underneath its acreage position. That resource base could fuel decades of growth for investors.

In fact, over just the next three years, Concho Resources expects to deliver 20% compound annual production growth while living within cash flow at current oil prices. While oil prices are volatile, it is confident in its ability to hit that growth target because it has chosen to lock in a significant portion of cash flow over the next two years with commodity price hedges, which will protect it against another oil price plunge. Meanwhile, if prices rise sharply, the company has the balance sheet strength and resource position to ramp up production and capture that upside.

Concho Resources is about to embark on a lucrative long-term expansion as it exploits the tremendous resource position it built up over the past few years. It's a ride that investors will not want to miss.

Short-term pain, long-term gain

Brian Feroldi(Under Armour): It is not often that investors can buy a founder-led business that holds massive long-term growth potential at a bargain price, but I think that's exactly the opportunity they have today with Under Armour.

Shares of the fast-growing apparel and footwear company have been under pressure for months after management took a hatchet to their long-term earnings guidance. They had previously told investors that the company would produce $800 million of operating income by 2018, but dialed back on that target because they've chosen to invest more in the business. The company believes that its investments will lead to substantial growth over the long term, but they warned that it would cause their short-term margins to remain under pressure.

Traders didn't take the news well. The company's shares have fallen by nearly a third over the last six months. That has pulled theprice-to-sales ratio of its class A shares below that of its key rival,Nike.

UA PS Ratio (TTM) data by YCharts

I can't help but feel that the relentless selling pressure is overdone. After all, Under Armour has put up 26 quarters in a row of 20%-plus revenue growth, which is an especially impressively accomplishment when you remember that its recent results were impacted by bankruptcy of The Sports Authority.Looking ahead, the company'sinvestments in footwear,digital fitness, and its international business should help the trend to continue.

If you are a long-term believer in this company's management team -- as I am -- then I think right now is a terrific time to consider joining me as a shareholder.

This stock should soar as the world goes digital

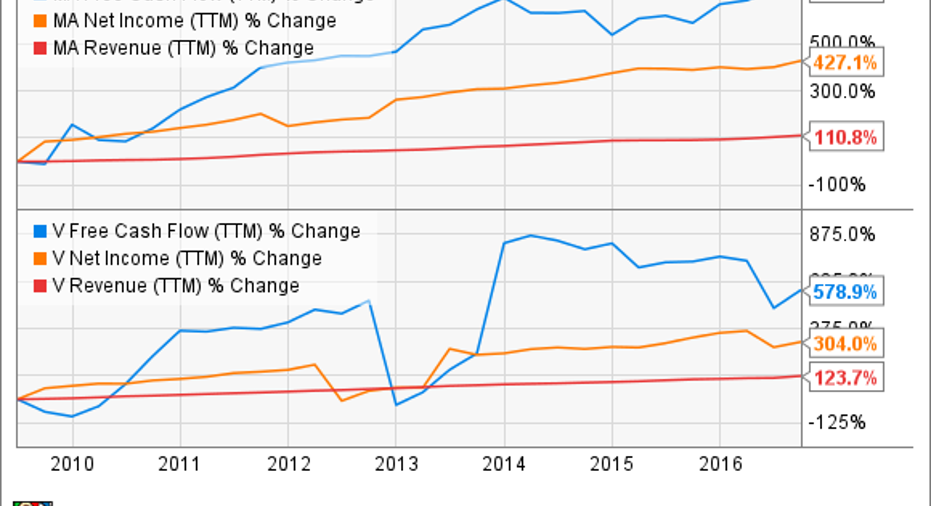

Neha Chamaria(Mastercard):As long-term investors, you want to own durable businesses with a wide economic moat, solid track record, and significant growth potential. Credit card behemoth Mastercard fits the bill. First things first: Check out the growth in Mastercard's revenue, net income, and free cash flow in the past decade. I've shown it next to rival Visa's (NYSE: V) statistics to give you a better idea.

MA Free Cash Flow (TTM) data by YCharts

That steady FCF growth particularly stands out, as FCF matters the most when it comes to shareholder returns. Mastercard doesn't disappoint: It has earned returns well above40% on invested capital as well as equity since 2012, and has raised its dividend every year since. Let's not forget the $4 billion share buyback authorization that the company announced last month.

As one of the world's leading payment-processing companies, Mastercard is staring at a massive opportunity: the ongoing shift from cash to plastic. According to Mastercard's financial arm, a staggering 85%of all transactions across the globe are still made in cash, and therein lies Mastercard's growth potential. India's recent demonetization drive, followed by an aggressive "go digital" campaign, is a fine example, one that the company is rightfully exploiting.

Despite a strong run in 2016, Mastercard is cheaper than Visa at 29 times trailing earnings. That's still a bargain for long-term investors given Mastercard's growth catalysts.

It's not your father's General Electric

Jamal Carnette, CFA: (General Electric). General Electric has always been plagued by investor misperceptions. Under prior CEO Jack Welch, shares rallied 4,000%. However, Welch's tenure was marked by mission creep as the industrial giant ventured into real estate, media, and financial services. After the Great Recession hit in late 2007, many long-term investors were surprised to find out that General Electric was classified as a "too big to fail" financial institution.

Current CEO Jeff Immelt has reoriented General Electric back to its manufacturing roots. In the short run, the company could benefit from President-elect Donald Trump's infrastructure spending plans. But even if Trump's proposals never come to fruition -- and there's considerable opposition to his plans even among his own party -- General Electric unveiled its future this month at the Consumer Electronics Show in Las Vegas.

For the past few years, General Electric has been showcasing its contributions to the consumer Internet of Things with connected appliances like refrigerators and stoves at the tech-focused trade show. A bigger opportunity for GE is in the industrial Internet of Things -- bringing connectivity and data analysis to industrial applications like electrical grids and water utilities. A 2011 white paper from the company says the Industrial Internet could benefit 46% of the global economy, a figure in excess of $32 trillion.

General Electric will be a major player in the industrial IoT as a traditional manufacturer and as the company behind the leading operating system of the industrial internet, Predix. The tremendous opportunity of the industrial IoT is why long-term investors would be wise to add the stock to their portfolios.

Cheers to this buying opportunity

Steve Symington (Boston Beer Company): Boston Beer stock had a rough 2016, falling nearly 16% as it lost market share in each of the past four quarters. Competition is bearing down as larger brewers muscle their way into the craft category, and as smaller brewers continue to expand regional distribution. And the craft-brewing industry overall has suffered decelerating growth in recent quarters.

However, shareholders of the leading American craft brewer have also enjoyed a modest rebound since late October, when the company's third-quarter 2016 report revealed signs of progress. Boston Beer founder and Chairman Jim Koch noted the company is finally at the "end of a long phase of constantly increasing shelf space," which means retailers are opting to "remove some of the confusion from the category" by reducing the number of SKUs in the beer aisle. As a result, Koch says, more established names like Boston Beer should be poised to benefit.

In the meantime -- and given its long runway for growth with less than 2% of the U.S. beer market -- Boston Beer continues to take an admirable long-term view.

"We remain prepared to forsake short-term earnings, as we invest to return to long-term profitable growth," said CEO Martin Roper, "commensurate with the opportunities and the increased competition that we see."

I don't know about you, but as a long-term investor Boston Beer is exactly the kind of company I want to see in my portfolio.

A great business at a reasonable price

Jason Hall(Chart Industries, Inc.): If you're looking for a successful long-term investment, Warren Buffett's advice to find a "great business trading at a reasonable price" is a far better strategy than a "fair business at a great price." And whileChart Industries isn't trading at the fire-sale prices it was available for about a year ago, it's still relatively cheap, based on how much it has traded for in the past.

GTLS EV to EBITDA (TTM) data by YCharts

Furthermore, it is a great business, with more than a century of success in the gas-processing equipment business (though it only recently became a standalone, publicly traded company).

And while the company's exposure to the oil and gas industry has caused it to struggle a bit over the past couple of years -- and even led to it reporting GAAP losses in recent quarters -- its cash flows have remained steadily positive while management worked to reduce overhead and better position the business to ride out the downturn in the oil and gas industry.

But while the cyclical energy downturn has been painful, Chart is positioned to emerge from it even stronger. The company launched a service-and-support operation over the past year that has already started generating steady, recurring cash flow. This should reduce cyclical impacts in the future, while also providing a new source of long-term profits. And while the company did shutter some facilities and lay off employees, management prioritized retaining key engineering and customer-support personnel, making sure Chart was well-positioned to handle the expected influx of new orders when the energy cycle returns to growth.

Bottom line: Don't let the irrational exuberance of a few years ago mask the quality nature of Chart's business. Now's a great time to buy this company for the long term.

10 stocks we like better than General Electric When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now and General Electric wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Brian Feroldi owns shares of Boston Beer, Mastercard, Nike, Under Armour (A Shares), Under Armour (C Shares), and Visa. Jamal Carnette owns shares of General Electric. Jason Hall owns shares of Chart Industries, Mastercard, Under Armour (A Shares), and Under Armour (C Shares). Matt DiLallo owns shares of Chart Industries, Mastercard, Under Armour (A Shares), Under Armour (C Shares), and Visa. Matt DiLallo has the following options: long January 2018 $45 calls on Nike and short April 2017 $55 calls on Nike. Neha Chamaria has no position in any stocks mentioned. Sean Williams has no position in any stocks mentioned. Steve Symington owns shares of Under Armour (A Shares) and Under Armour (C Shares). The Motley Fool owns shares of and recommends Boston Beer, Chart Industries, Mastercard, Nike, Under Armour (A Shares), Under Armour (C Shares), and Visa. The Motley Fool owns shares of General Electric. The Motley Fool has a disclosure policy.