7 Reasons to Use a Roth IRA to Save for Retirement

The Roth IRA is one of the best, but least understood, ways for Americans to save and invest for their retirement. There are several things most people don't realize about Roth IRAs -- for example, did you know that you can withdraw your Roth contributions whenever you want, without penalty? Here's what you need to know about the benefits of investing with a Roth IRA.

Image source: Getty Images.

1. Tax benefits in retirement

The most obvious benefit of a Roth IRA is that it can provide you with tax-free retirement income. Traditional IRA contributions can qualify for a tax deduction, but eventual withdrawals in retirement will be subject to income taxes. Roth IRAs, on the other hand, do not qualify for an immediate tax break. Instead, qualified withdrawals from your Roth IRA will be 100% tax-free.

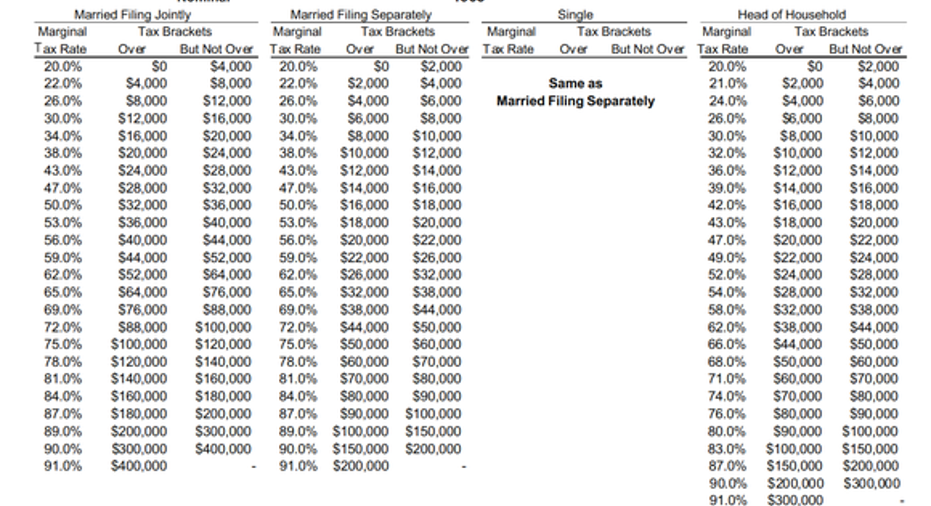

This can be an excellent hedge against future tax rates. Sure, President-elect Donald Trump has promised to simplify and lower the tax brackets, but there's simply no way of knowing what could happen beyond that time. In fact, the top tax bracket was 70% every year from 1965 through 1981, and the only reason it wasn't higher was because taxes were cut in the Tax Reform Act of 1964. Check out the U.S. tax rates from 1963 -- could you imagine paying Federal taxes on up to 91% of your income?

Image source: Tax Foundation.

While I don't see rates anywhere near that high coming back anytime soon, the point is that nobody knows. It's entirely possible that tax rates when you retire will be significantly higher than they are today, but if you set some of your retirement savings aside in an IRA, you don't need to worry about it.

2. Tax benefits before retirement

This benefit applies to traditional IRAs and other types of retirement accounts as well, but it's worth mentioning. After you contribute to your Roth IRA, your investments can grow tax-free over the years.

In other words, when your stocks pay dividends, you won't get a bill for taxes on that income -- you can use all of your dividends to reinvest, allowing your money to compound faster. The same can be said about capital gains taxes. If you sell an investment in your Roth IRA at a profit, you won't have to pay a penny in capital gains tax, even if you earned a million dollars. This leaves you free to reinvest your entire profit, maximizing the long-term power of compound gains.

3. No required minimum distributions

Traditional IRAs, as well as other tax-deferred retirement accounts such as most 401(k) and 403(b) plans, require the account holder to start taking required minimum distributionsat age 70-1/2. Essentially, the IRS puts a time limit on the tax-deferral benefits of these accounts.

Since a Roth IRA is an after-tax retirement account, there is no such requirement. It makes sense -- since Roth withdrawals are generally tax-free, the IRS doesn't really care when you take the money out. If you don't need the money, and want to let your account grow until you're 90 years old, go for it. In fact, this feature is one reason Roth IRAs can be great estate-planning tools, as I'll discuss in more detail later.

4. Your money isn't tied up

One common reason my friends often give for not saving more for retirement is, "I don't want that much of my money tied up until I'm retired."

With a Roth IRA, this isn't the case. Because you've already paid income taxes on the money you contribute, you are free to withdraw your contributions, but not your investment gains, without penalty. In other words, let's say that you contribute $5,000 to a Roth IRA. If you need funds in an emergency, you can withdraw that money -- no questions asked.

For this reason, a Roth IRA is a fairly common choice for a college savings vehicle or for creating an emergency fund. Not only can you withdraw your contributions when your child goes to college, but there is a special provision that says all IRA funds can be withdrawn penalty-free for higher education costs. If your child doesn't go to college, you can leave the money invested for your own retirement, in contrast to other college savings plans such as the 529, which assess a penalty for non-educational withdrawals.

5. A Roth IRA can be a great complement to other retirement accounts

If you have multiple retirement accounts, such as a Roth IRA and a 401(k) plan at work, you'll have tremendous tax flexibility in retirement. For example, you can withdraw from your 401(k) up to the threshold for a low tax bracket, and then use your Roth IRA's tax-free withdrawals for any income you need beyond that. If you're in a higher tax bracket in retirement, you could choose to use your Roth IRA first, to avoid adding any more taxable income.

6. You can contribute as late or as early as you want

With traditional IRAs, you cannot make contributions after you reach age 70 1/2. Roth IRAs have no such restriction. You can contribute to your Roth IRA for as long as you have earned income. For example, if you work part-time well into your retirement, you're free to stash some of your earnings in your Roth IRA.

7. Roth IRAs are great for estate planning

Not only can a Roth IRA allow you to produce tax-free retirement income for you, but it can be a great tool to leave a source of tax-free income to your heirs. Effectively, by using a Roth IRA to build up an inheritance for your loved ones, you're "pre-paying" the taxes for future generations.

Once inherited, the account cannot just grow indefinitely. Your heirs will have to take minimum annual distributions based on their life expectancy, as per the IRS' actuarial tables. They can also choose to take it all at once, but the best use of an inherited Roth IRA is to create tax-free income that lasts for the rest of your loved ones' lives.

How to get started

One (sort-of) negative factor I should mention is that the ability to contribute directly to a Roth IRA is subject to income limits -- you can find 2017's here.

However, there is a "backdoor" method of contributing that essentially consists of contributing to a traditional IRA and then immediately converting the account into a Roth IRA. The point is, even if you earn a high income, with an additional step you can take advantage of all the benefits I mentioned.

Once you've decided that a Roth IRA is right for you, check out The Motley Fool's IRA center, which can help guide you through the process from choosing a broker to investing your Roth contributions wisely.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

The Motley Fool has a disclosure policy.