5 Things to Know Before You Buy Under Armour Inc Stock

Image source: Under Armour.

Under Armour (NYSE: UAA) (NYSE: UA) was one of the worst performers in the S&P 500 last year, declining 28% as the broader market rose 10%. Thanks to that gap, the sports apparel giant might seem like a no-brainer purchase to prospective shareholders.

It is, after all, one of the fastest-growing companies on the market and is staring at a massive global sales opportunity in categories like footwear, active wear, and connected fitness.

Before pulling the trigger on this stock, though, here are a few key facts for investors to consider.

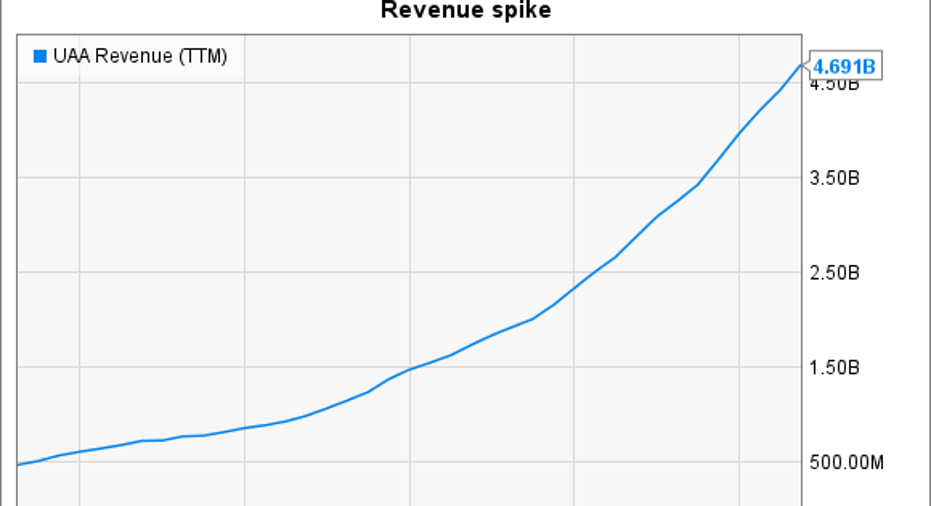

Long-term sales growth

Under Armour's sales base is approaching $5 billion per year, from just $1.5 billion in 2011. It has boosted revenue by 20% or better in each of the last 26 quarters and doubled its revenue base over the last three fiscal years.

UAA Revenue (TTM) data by YCharts.

That's enough to qualify the company as one of the fastest-growing stocks on the S&P 500. In its most recent complete fiscal year, Under Armour expanded at a blistering 29% clip.

Recent slowdown

2016 began with even faster gains, and the boost added credibility to management's initial 2016 forecast that predicted a 25% annual spike to $5 billion. However, Under Armour's expansion pace has slowed down from there.

Its second-quarter revenue improved by 28%, giving way to a 22% increase for the third quarter. As a result, CEO Kevin Plank and his executive team had to dial back their guidance and now see sales rising by 22% for the full year, raising the possibility that the company's best growth days are behind it.

Under Armour's slowdown isn't happening in a vacuum, though. Chief rival Nike (NYSE: NKE) was the Dow's worst performer last year as its short-term sales and profit results also disappointed Wall Street.

Where the growth is coming from

Most of Under Armour's recent gains have come courtesy of two big growth drivers: the push into footwear and international expansion. Revenue from outside of the U.S. is up almost 70% over the past nine months and now accounts for 15% of the business, compared to 9% in 2014. Nike currently gets just over half of its sales from outside geographies, which helps explain why Under Armour executives are so bullish about their long-term prospects. "We expect to be a global brand," Plank told investors in July. "The global expansion that we've been able to enjoy is something we're really excited about."

The spike is even more pronounced in a footwear segment that's about to grow into a $1 billion business responsible for a quarter of Under Armour's sales -- up from 14% just two years ago.

Data source: Under Armour financial filings.Chart by author.

Profitability is falling

The sports shoe business doesn't enjoy the same economies that apparel does, and so Under Armour has had to trade higher footwear sales for lower profits. Gross margin is down a full percentage point over the past three quarters.

UAA Gross Profit Margin (TTM) data by YCharts.

Rival Nike is also experiencing a profitability pullback, but the problem is more pronounced at Under Armour. At under 48% of sales, gross margin is sitting at its lowest point since the company went public. That's risky territory for a stock that's valued at a huge earnings premium to rivals and the broader market.

Growth with lower profits

Despite increased competition with Nike and others in the key U.S. market, Under Armour still believes it will pass $7.5 billion of annual revenue by the end of 2018, implying gains of around 22% in each of the next two years. Profit growth won't be nearly as strong as Plank and his team originally expected, though. Operating income should grow at a roughly 15% pace over that time to come in below their long-term target.

Laying the groundwork for future growth is the right strategy, even if it means lower earnings over the next few years. If all goes to plan, the company will then be in a much stronger profit position as an established global brand that's sprinting toward $10 billion in annual revenue.

10 stocks we like better than Under Armour When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Under Armour wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Demitrios Kalogeropoulos owns shares of Nike and Under Armour (C shares). The Motley Fool owns shares of and recommends Nike, Under Armour (A shares), and Under Armour (C shares). The Motley Fool has a disclosure policy.