5 Things All Investors Should Know

Image Source: Getty Images

Whether you're new to investing or have been going strong for some time, there are certain things you need to know about the markets and investing, in general. We asked five of our contributors to shed some light on these concepts for our readers, and here is what they had to say.

The Closest Thing to a Free Lunch in Investing

Chuck Saletta: The old saying might be,"There ain't no such thing as a free lunch," but in investing, there's one concept that can get you remarkably close: diversification. Done right, diversification can reduce the overall risk to your portfolio without affecting the overall expected return of your portfolio.

To see how diversification can help, imagine a situation where every stock you own is completely independent of every other stock, and has the following potential return profile:

|

Probability |

Return |

|---|---|

|

25% |

-100% |

|

50% |

20% |

|

25% |

100% |

Table by the author.

Your overall expected return would be 10% -- about in line with the market's long-run average -- but you'd have a 25% chance of losing everything. If you split your investments evenly across two stocks, your expected return would remain the same, but your chance of losing everything drops to 6.25%. Make it three stocks, and your chance of losing everything drops to about 1.6%, again without affecting your overall expected return.

The benefits of diversification are real, and best of all, you don't have to overcomplicate things to get most of the protections it provides. Simply split your investments across different companies in different, largely unrelated industries, and be willing to cross geographic boundaries while you're doing it. As long as every individual stock you pick looks like it's worth investing in on its own, the diversified combination will better protect your overall portfolio than any one company's stock on its own could.

Patience and perseverance can be profitable

Selena Maranjian: Many people get turned on to investing after hearing about how someone struck it rich by investing in a stock that skyrocketed. That's certainly an appealing prospect, but it's easier said than done. If it were such a simple task to identify stocks headed for the stratosphere, then most managed mutual funds wouldn't lag the overall stock market in performance.

Fortunately, you don't need brilliant stock picks in order to build a solid nest egg. You just need perseverance and patience.

You can accumulate a lot over time via compounding if you sock away relatively modest amounts and earn reasonable rates of return. Check out the table below:

|

Growing at 8% For |

$5,000 Invested Annually |

$10,000 Invested Annually |

$15,000 Invested Annually |

|---|---|---|---|

|

15 years |

$146,621 |

$293,243 |

$439,864 |

|

20 years |

$247,115 |

$494,229 |

$741,344 |

|

25 years |

$394,772 |

$789,544 |

$1.2 million |

|

30 years |

$611,729 |

$1.2 million |

$1.8 million |

You may be able to achieve an average annual growth rate of 8% simply via an inexpensive broad-market index fund, with no stock picking required at all. There are many people out there who are making money off of investors by portraying the stock market as a very complicated and difficult thing to master. Building substantial wealth can be relatively simple, though, if you're diligent.

Keep your eyes focused on the long term

Brian Feroldi:When I first started investing, I focused all of my attention on what was happening in the markets that day, figuring that I was smart enough to make money off of short-term price movements. Thankfully, I failed miserably in my efforts, and have come to learn that, because short-term price movements are random, it's folly to try and day trade your way to success.

That's a hard truth for many investors to accept -- at least it was for me -- but the sooner you accept it, the better your results will be.

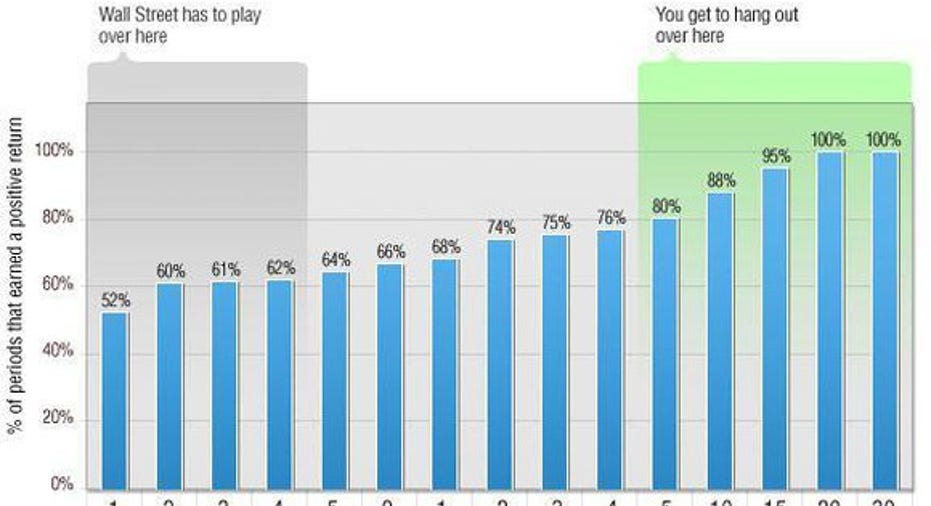

A few years back, myFoolish colleague Morgan Houselcreateda great chart that really helps to hammer this point home. He used data from Robert Shiller that data back to 1871, and looked at how often the market goes up -- in real terms, which adjusts for inflation -- over various holding periods.

Here's what that chart looks like:

Source: Robert Shiller, Morgan Housel's calculations.

As you can see, over extremely short holding periods, the odds of the markets moving higher are only slightly better than a coin flip. Even looking out toward a holding period of one year -- which is a time period that many on Wall Street consider to be extreme -- the odds of making money are still only two out of three.

However, once you start to look at multi-year holding periods, the odds of success start to reallytilt in your favor. If you're willing to stay invested in the market for five years, then you have an 80% chance of making money, and the odds only climb from there.

This graph has forever turned me into a long-term-only investor, and hopefully, it can do the same for you.

Taxes are not your friend

Matt Frankel: One thing all investors should be aware of is the power of tax-advantaged investing. If you have a 401(k) or similar retirement plan at work, you're already taking advantage of it.

When you open a brokerage account, you have the choice between a standard (taxable) account or a retirement account, usually a traditional or Roth IRA. With a traditional IRA, you may be able to deduct your contributions on your tax return this year. On the other hand, Roth IRA contributions aren't deductible, but your qualified withdrawals in retirement will be completely tax free. With both account types, you won't have to pay dividend or capital gains taxes on an annual basis.

The beauty is that, because you won't pay taxes on your dividends and investment profits when you sell a stock or fund, you can use all of your proceeds to reinvest. Over time, the effect of this can be truly incredible. Consider this example:

Let's say that you make two $5,000 investments in the same stock -- one in a taxable account and the other in a Roth IRA. This hypothetical stock has a 4% dividend yield, and the share price increases by 6% per year, on average, for a 10% annualized total return.

After 30 years, the taxable investment would grow to $67,680, assuming the dividend qualifies for the preferential 15% rate for most tax brackets. After selling the investment and paying capital gains taxes -- also 15% for most taxpayers -- you'll end up with $58,280. Not bad, right?

On the other hand, the exact same investment in a Roth IRA would have swelled to more than $79,300. And because Roth withdrawals are tax free, you can sell the stock and keep it all. This is 36% more than the same investment generated in a taxable account. That's the power of tax-advantaged long-term investing.

Don't waste money on expenses

Dan Caplinger: Most investors put the bulk of their attention on finding investments that will maximize their returns, expending huge amounts of effort in search of the next blockbuster stock. However, generating returns that surpass what the overall market produces won't do you any good if you end up spending all of your surplus gains on investment-related expenses.

For example, many investors use actively managed mutual funds to invest. These funds engage professional managers who seek out stocks and other investments that they hope will outperform their benchmarks. However, with expense ratios of 1% or more for many active stock funds, the managers that work for those funds start with a substantial handicap to low-cost alternatives like index funds. Put another way, if you invest in something that charges you a 1% fee, you -- or the professionals working for that investment -- will have to generate an investing advantage of one full percentage point just to get back to even.

The same dangers exist for other costs. Commissions can make stock trading prohibitively expensive, while surrender charges for life insurance policies and annuities can be draconian in their reach. If you can reduce or eliminate costs when you can, you'll ensure that you get to keep the bulk of the profits you generate from your investing.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.