4 Reasons to Love Oil Stocks

Image source: Chevron.

Oil prices started their decline in mid-2014, and since that point, oil stocks have been in a deep funk. It's understandable that investors would be sour on the group, particularly since the media is almost giddy at the opportunity to announce the name of the latest energy company to crater into bankruptcy. But it's during these dark times that you can find some really great bargains. And, truth be told, there are some pretty good reasons to love oil stocks -- even now.

CarsOne of the first things to think about when you look at oil is gasoline. It's one of the primary uses of oil. There's a huge infrastructure built around gasoline and its use in transportation. Just look around as you're driving and notice how many ExxonMobil (NYSE: XOM), Chevron (NYSE: CVX), and Royal Dutch Shell (NYSE: RDS-B)-branded stations there are. And those are just the big names.

To be sure, there are alternative fuels making inroads into the auto market. Electric cars and hybrids are the big ones. But these technologies are only scratching the surface right now. Essentially, it's hard to beat the portability, power, and ease of gasoline. And don't forget that a car isn't a disposable item. The things last for a decade or more.

So every new gasoline car sold today extends the life of the oil industry for as long as that car stays on the road. But don't think about this in terms of the U.S. market, where increasing efficiency is reducing the amount of gas we use overall. This is a global phenomenon driven by an increase in the number of cars being built and used around the world, with rising incomes in emerging markets leading the charge.

Gasoline will probably be replaced at some point. But the threat isn't imminent today, which makes the auto industry one key reason to love oil stocks.

The invisible handThe next fact that's important to remember is that oil is a commodity. Often a very volatile one, at that. This downturn may hurt, but it's hardly the first time that high prices have led to an oversupply of oil. When this happens, everyone is worried that low prices will remain in place forever. But look at the pullback throughout the industry, and you see the beginning of the next upturn.

The capital spending slowdown at Exxon. Image source: ExxonMobil.

ExxonMobil, for example, cut its capital spending between 2014 and 2015 and is expecting to trim at least another 25% this year. The direction is the same at Shell, and, frankly, at just about every major and minor oil player. But here's the thing. The less spent to look for oil, the less chance you you find new sources. That means that once demand and supply balance, you could quickly find that there's not enough oil to go around. That's when oil prices, and the shares of the companies that drill for the stuff, will rebound.

Sure, this time could be different, but that's not likely. So oil is cheap today, but the regular cycles in this volatile market suggest that won't last forever. And, thus, reason No. 2 for being enamored of oil stocks.

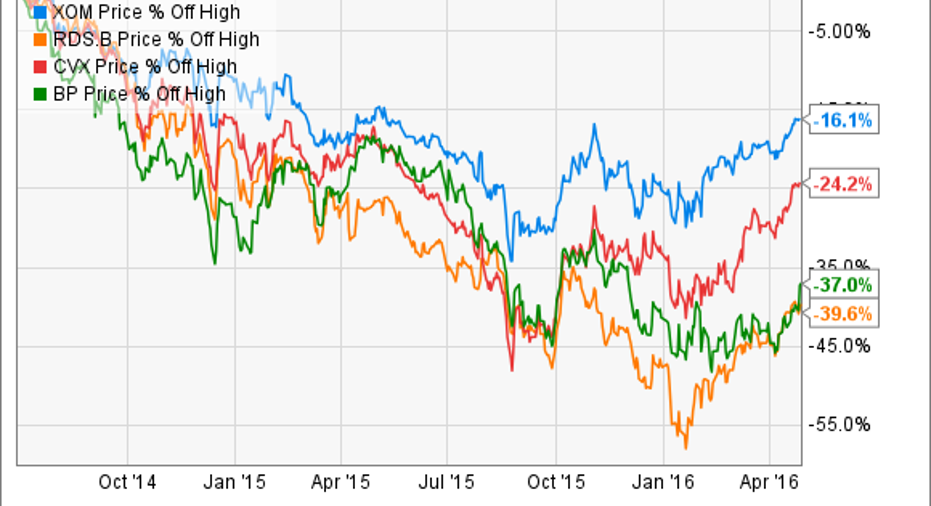

Cheap stock pricesAnd that sets up lovable reason three: Oil stocks are kind of cheap today. Although the quartet of oil giants have had a good run since around the middle of January, if you look back to mid-2014, the numbers are a bit different. Exxon, one of the strongest oil majors, has held up the best, down just 16% or so, with Shell posting the worst showing, down nearly 40%.

To be sure, all of these companies are facing big headwinds. But all have been around for a very long time -- more than 100 years in most cases -- and have lived through a downturn or two in their day. They are highly likely to see the other side of this one, too.

That doesn't mean an investment here is risk-free. That's simply not the case. All of these oil players are still spending billions of dollars to keep their businesses running at a time when revenues and earnings have hit the skids. So increasing debt loads and even dividend cuts have to be in the back of your mind. But for a long-term investor, these are likely to prove short-term issues.

And when looked at from a bigger-picture view, some of the problems aren't all that huge. For example, at the end of the first quarter Chevron's debt stood at just 22% of its capital structure. Sure, investors might like to see it lower, but that's hardly a number that should invoke the fear of insolvency.

DiversificationNow, you might have noticed that the oil companies I've noted are all majors. In other words, they have global portfolios and operate as drillers, refiners, and chemical companies. This was on purpose, since companies focused just on drilling oil and nothing else are riskier to own in a downturn. That's why most of the bankruptcies taking place are in this space. Sure, there's probably more upside in a wildcatter, but safer is better right now.

For the oil majors, diversification has been an important theme. While the oil side is hurting from low oil prices, the chemical and refining sides are benefiting from lower input costs (that is, low oil prices). So this side of the business has provided an offset to the decline on the oil side, resulting in a smoother ride.

These companies are also increasingly looking at natural gas as an important avenue for the future. Shell, for example, is in the midst of a large natural gas acquisition. This is worth remembering, because while electric cars may some day reduce the need for gasoline, natural gas is, as you read this, displacing coal in the electricity generating space. In other words, the oil giants aren't sitting around waiting to become obsolete. Diversification is a lovely thing in so many ways.

Do you love it?So there are four good reasons to love oil stocks, at least the largest, most diversified, and financially stable ones, such as Exxon, Shell, and Chevron. You may have noticed that I didn't mention dividend yields, which range from Exxon's 3.3% or so on the low end to Shell's 7.1% or so on the high end. Some of these companies do have enticing yields, and they appear willing to support the payouts at this point. But I don't think yield alone is the best reason to love an oil company. After all, there's always the risk that the company trims the payout. Dividends are more of an icing-on-the-cake issue.

Indeed, if you're a long-term investor buying an oil company today, you need to believe (1) in the big-picture future for oil, (2) that the oil market will eventually recover, (3) that the stocks you're looking at present a decent value, and (4) that the company you ultimately invest in is strong and diversified enough to withstand the downturn. At this point, I think Exxon, Shell, and Chevron all pass those tests -- and, as a little icing on the cake, they pay a nice dividend along the way.

The article 4 Reasons to Love Oil Stocks originally appeared on Fool.com.

Reuben Brewer owns shares of ExxonMobil. The Motley Fool owns shares of and recommends Chevron. The Motley Fool owns shares of ExxonMobil. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.