3 Things Investors Should Know About Intel Corporation

Image source: Intel.

Just about every tech investor has heard of chip giant Intel (NASDAQ: INTC). The company provides the chips for the vast majority of the personal computers and servers that are sold each year, generates more revenue than any other publicly traded chip company, and is wildly profitable.

It's also a very controversial name. Though the chipmaker holds dominant positions in several very lucrative markets, it has had a tough time branching out beyond its core business. Its efforts to attack the mobile processor market simply haven't worked, and its efforts to serve as a contract chip manufacturer haven't yet delivered much in the way of revenue.

Today I'd like to go over a few things about Intel that may be helpful to both current investors as well as to those considering taking a position in the stock.

Who are Intel's biggest customers?

According to Intel's latest annual report, the company's three largest customers during 2015 were as follows:

- 18% of Intel's total revenue in 2015 (or roughly $10 billion) came from sales to HP Inc.(NYSE: HPQ) and Hewlett-Packard Enterprise (NYSE: HPE). HP Inc. is a major provider of personal computers while Hewlett-Packard Enterprise is a major server hardware vendor.

- 15% of Intel's revenue in 2015 came from sales to privately held Dell. Dell, like HP Inc. and Hewlett-Packard Enterprise, is a major provider of both personal computers and servers.

- 13% of Intel's 2015 revenue came from Lenovo (NASDAQOTH: LNVGY), also a major vendor of personal computers and servers.

The chipmaker says that "no other customer accounted for more than 10% of [its] net revenue" in 2015.

Although Dell is privately held and doesn't disclose financial results, the information above suggests that current and potential Intel investors may be well-served to pay close attention to the financial results and related commentary from HP Inc., Hewlett-Packard Enterprise, and Lenovo (all three are publicly traded) for "hints" as to where Intel's business may be headed.

Significant dependence on personal computer market

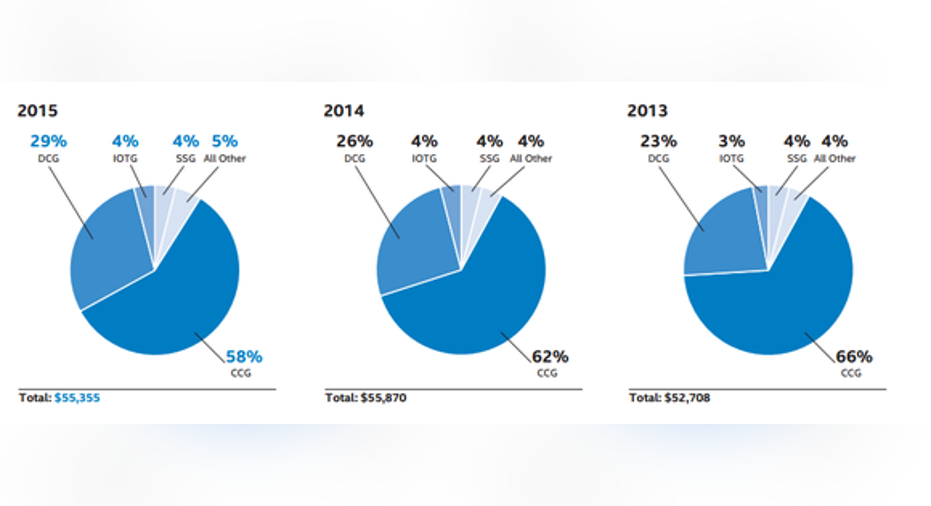

In its most recent 10-K filing, Intel provided breakdowns of its revenue by segment for 2013, 2014, and 2015, as you can see below:

DCG = data center group. IOTG = Internet of Things group. SSG = software and services operating segments. CCG = client computing group. Image source: Intel.

More than half of the company's revenue in 2015 still came from sales of chips into personal computers, though that figure has come down from 66% in 2013 to 58% in 2015 (partially as a result of the growth of other segments, but partially as a result of the decline in overall personal computer sales).

What this means for investors is that although Intel's revenue base is becoming increasingly diversified (particularly as its data center business continues to grow), its financial health is still substantially a function of the health of the overall personal computer market.

This means that investors shouldn't dismiss any positive or negative data points around the personal computer market, because odds are that, good or bad, they could be quite meaningful to the chipmaker's financial results (and, potentially, its stock price).

Intel's future is in the data center

That being said, investors will notice that the company's data center group (commonly abbreviated DCG) is a substantial and rapidly growing portion of its revenue base. In 2015, it hit 29% of revenue, and it probably won't be too long before it crosses the 33% threshold.

This means that, as far as investors should be concerned, the health of the overall server market as well as Intel's ability to maintain share and grow chip content there should also be quite important. And, over time, this segment is only going to become more important to the company.

The good news is that the overall market for data center processors and related solutions is quite robust, as Intel's growth in this segment over the years shows. The bad news, though, is that Intel is likely to face competitive pressures here over the next several years, meaning that Intel's ability to defend its high market share in key areas (such as enterprise and cloud servers) will become increasingly important to the narrative around the company.

Interestingly, Intel's data center group is large enough today to, given a reasonable amount of growth, offset declines in the personal computer market. Indeed, in 2015, Intel's client computing group, or CCG, took in $32.219 billion in revenue, while its data center group raked in $15.977 billion in revenue.

Based on those figures, for every 1% decline in CCG revenue, it would take about a 2.02% increase in DCG revenue to keep total revenue flat. Over time, as DCG becomes larger (and, presumably, CCG becomes smaller), it should take less growth from DCG on a percentage basis to offset declines in CCG going forward.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Ashraf Eassa owns shares of Intel. The Motley Fool recommends Intel. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.