3 Things Enbridge Has to Prove in 2017

Enbridge (NYSE: ENB) and Spectra Energy (NYSE: SE) are on the cusp of becoming an absolute behemoth in the oil and gas transportation and logistics business. Wall Street appears to be a big fan of the potential merger, as shares of Enbridge and Spectra are up 12% and 21.5%, respectively, and there are few signs that the deal won't happen. So it looks like it's full steam ahead for this North American logistics company.

For investors in this combined company, there are lots of reasons to be optimistic for the future, such as management's projection for 10% to 12% dividend growth all the way out to 2024. As great as that sounds, there are some things the company needs to do this year to show that it can indeed meet these lofty goals. Let's take a look at three things investors should demand that Enbridge do in 2017 to prove that this megamerger was worth it.

Image source: Getty Images

Smooth integration process

The ink isn't yet dry on the merger between Enbridge and Spectra Energy, but there hasn't been much in the rumor mill about the deal not passing muster with regulators. Spectra's shareholders have already voted to approve the deal. Based on this, I think we can reasonably assume that the deal will get approved without significant assets sales or changes.

According to management, this deal is an immense opportunity to save the company money in synergies. There's also thepotential for more favorable financing rates for new projects that will likely happen as a much larger company.

Image source: Enbridge investor presentation.

As with every merger and acquisition, though, the devil is in the details. The plan to save that much money may make sense on paper, but it does not necessarily mean it will be executed. Management says that these synergy estimates are conservative, but one thing they need to prove right out of the gate in 2017 is that these kinds of savings are achievable. More than anything in 2017, this is going to be the thing to watch in investor presentations and quarterly reports.

Managing its new energy empire

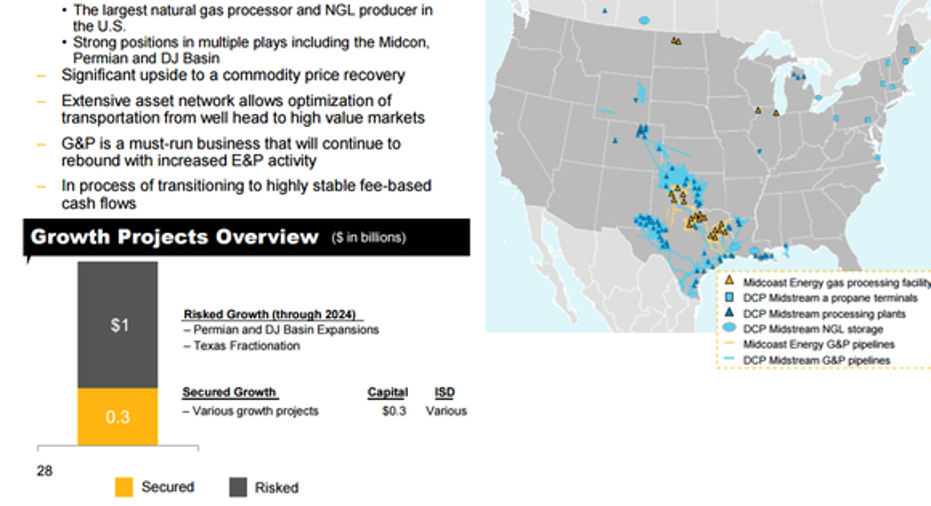

Here's one thing that isn't being discussed much with this Enbridge/Spectra Energy merger. Upon completion, the two businesses will be in charge of the capital allocation of seven separate publicly listed companies and subsidiaries in the U.S. and Canada. In certain cases, some of those companies will have overlapping interests. For example, both Midcoast Energy (NYSE: MEP) and DCP Midstream(NYSE: DCP) are both natural gas gathering and processing companies with a lot of geographic overlap.

Image source: Enbridge investor presentation.

If these entities were to remain separate, it would pose a capital allocation challenge for the parent company. Even though one company could have the better returns for a particular investment, Enbridge also has to balance the fact that investors in each business are going to expect a certain amount of growth. This will apply to all seven of these publicly traded units.

Granted, the company does have $48 billion in projects in the wings on top of the $26 billion currently under construction. So there is plenty of growth potential to be passed around. The bigger question is, if the company does for some reason become capital constrained, how will it balance the need for focusing on its highest-return projects while providing adequate growth for all of these entities? Pending any significant consolidation of its subsidiaries, this will be a major concern for 2017 and beyond.

Get into target leverage range

One of the largest benefits for the combined company is better access to credit. The consolidated business will have an anticipated total enterprise value of $165 billion, far and away the largest oil and gas infrastructure company in North America. That size combined with the company's cash flow should easily give it an opportunity to have a strong credit rating that will reduce the company's overall cost of new capital.

One thing to remember, though, is that size doesn't matter if its debt load is beyond its cash-generating abilities. That was one of the reasons that Kinder Morgan has run into so many headaches since its own consolidation and why it cut its dividend: It needed the cash to pay for its own projects and pay down debt.

Enbridge management estimates that the combined company will have a debt-to-EBITDA ratio of 6.2. That is high, even for this industry that is known to be fueled by high levels of debt. Management's target range will be below 5.0 times EBITDA, and expects to get there by 2019. However, it does say that it will be achieved as projects are placed into service, and there is no mention of paying down any debt. With so much money going into its current construction, one has to wonder if it can take on that much more additional debt and reduce its leverage as those projects come online. It doesn't happen much in this business.

Investors should keep a very close eye on the company's debt metrics over the next couple of years. If management can't stick to its promises on lowering its leverage, then there may be cause for concern.

What a Fool believes

2017 is going to be a big year for the combined Enbridge and Spectra Energy (assuming the merger goes off without a hitch). With all the opportunities it presents, though, there are some big hurdles to clear that investors should pay attention to. Making the integration a smooth process that captures synergies, finding a balance for all seven corporate entities, all while bringing its debt metrics into target range are key things that investors should have an eye out for. If it can achieve those things, then management's projections of long-term double-digit dividend growth may be possible.

10 stocks we like better than Enbridge When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Enbridge wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Tyler Crowe has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Kinder Morgan and Spectra Energy. The Motley Fool recommends DCP Midstream. The Motley Fool has a disclosure policy.