3 Terrible Reasons to Buy Great Panther Silver Ltd.

Great Panther Silver Ltd.(NYSEMKT: GPL)is a relatively small miner focused on silver, as its name implies. Generally rising precious-metals prices have led the company's stock to an impressive 140% or so advance this year. But there's a lot more to understand about this story and how it could affect the future for the miner. Here, then, are three terrible reasons to buy Great Panther Silver Ltd.

Image source: Great Panther Silver Ltd.

1. An intoxicating price advance

Great Panther's stock is up more than giant miners such as Newmont Mining (NYSE: NEM) and Barrick Gold (NYSE: ABX), which have advanced "just" 95% and 115% or so, respectively, this year. However, if you step back and look at these price moves, there's a big difference. Newmont, for example, has seen its stock go up from around $18 a share in January to around $35 a share recently. Great Panther's stock has gone from around $0.50 a share to around $1.20.

That wasn't a typo. There's a whole different scale of business going on here. While the price advance for Great Panther is impressive, you can't get caught up in the percentage gain because it isn't the whole story. Yes, big price moves are exciting, but you have to look deeper.

In this case, Great Panther is a penny stock where tiny absolute moves make for huge percentage moves. For more confirmation of just how small Great Panther is, take a look at the company's market cap, which at around $200 million is minuscule compared with some of the better known miners. Barrick's market cap, to highlight the difference, is $18 billion.

Being tiny can certainly be a benefit, as the percentage price increase shows, but it can also be a big risk. For example, Great Panther Silver is down around 45% from its high this year, compared with declines of 32% and 23%, respectively, for Barrick and Newmont.

So don't get seduced by Great Panther Silver's big price move. The advance has a lot more to do with the fact that it's a marginal miner (more on that in point 3), so it's highly leveraged to changes in silver prices that can quickly push the bottom line into the black, or red ---- with investors reacting accordingly.

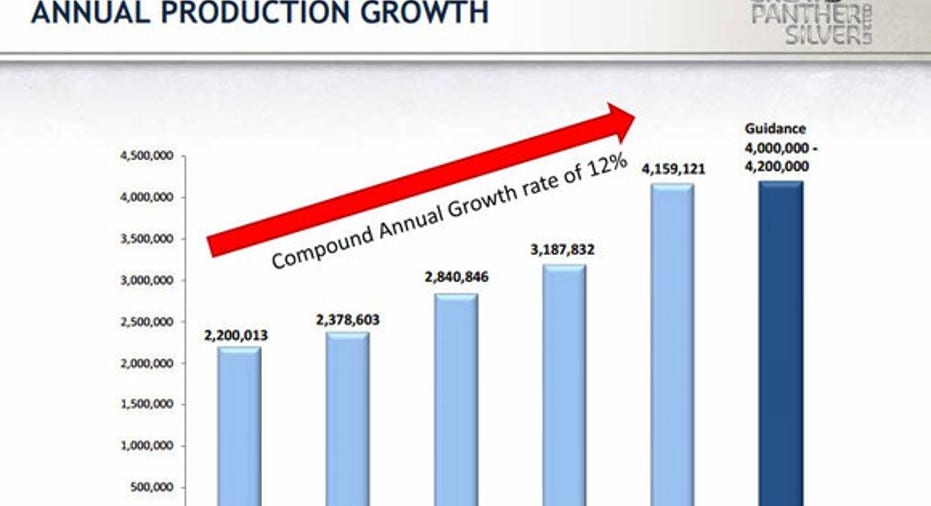

2. Production growth

In 2011, Great Panther Silver produced around 2.2 million ounces of silver. In 2015, it produced about 4.1 million ounces. That's a compound annual growth rate of around 12%. Impressive by any stretch of the imagination, particularly since Barrick's precious-metals production fall 20% over the same time span.

This makes sense, because Great Panther's business model is all about expanding. Although this year it expects production to be relatively flat compared with 2015, it has a number of exploration projects that could push growth even higher in the not too distant future. So, in some ways, production growth is exactly why you might want to own Great Panther.

However, with exploration and expansion comes risks. New mines are expensive to build, dangerous to run, and sometimes they don't produce the quality of ore you expect. In other words, the outcome of digging new holes is highly uncertain.

That's especially true here, where two mines account for virtually all of Great Panther's current production. And one, the Guanajuato mine complex, is 75% of the total. Adding another mine to the business would probably be a huge boost to production, but if things don't go as well as planned, a busted mine project could quickly turn into an expensive drag on the business.

Image source: Great Panther Silver Ltd.

And don't forget that relying on just two mines comes with its own production risks. For example, in the third quarter, silver production fell 13% because of temporary shutdowns and lower ore grades. The company expects to make up for lost ground by the end of the year, but it shows just how small the company is and what that can mean to its production -- both good and bad.

3. On the verge of a profit

Then there's the fact that Great Panther Silver is a hair away from turning a profit on the bottom line. In the second quarter it lost $0.01 a share. It lost $0.03 a share in the second quarter of 2015. It had been hovering in the range of $0.02 to $0.03 of red ink since that point. With the silver uptick this year, it looks like Great Panther could, possibly, make a profit at some point soon, assuming cost-cutting efforts continue to hold.

It would be easy to look at Great Panther making money, for a change, as a huge positive. But you can't count on that kind of result for the indefinite future. You see, the bigger impact here is really from silver prices. Great Panther is a marginal miner, with costs at a point where it basically needs higher silver prices to make money. Even if the company gets into the black, which would undoubtedly be good news, you can't ignore the bigger picture. At this point, if silver prices fall, Great Panther's results will follow quickly along.

So it's not that making a profit will be bad, but if you don't understand the nature of Great Panther Silver's position as a marginal miner focused on production growth, positive earnings might paint too good a picture. You'll want to make sure you dig deeper.

A risky investment, even if you understand it

Great Panther Silveris doing the right things and achieving success today, with the help of an improved silver market. But, that said, it is a small, marginal miner with a heavy focus on growing its production, a risky endeavor for any miner. A lot has to go right for the company to do well, including often volatile silver prices heading higher. You have to understand that if you are going to take the risk and invest here. Focusing only on the price advance, or production growth, or improving earnings alone could lead you to miss the bigger picture.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Reuben Brewer has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.