3 Smart Ways You Can Put $1,000 to Work Right Now

Whether it's from your tax return, a bonus at work, or some other means, if you've found yourself with an extra $1,000 or more on hand that you're looking to spend in a smart way, then you have a lot of choices. Below you'll read about three things you can do to help you build a bigger nest egg, protect your family's financial security, or help you get a leg up at work.

Here's a look at three smart ways to put $1,000 to work that you may not have thought of.

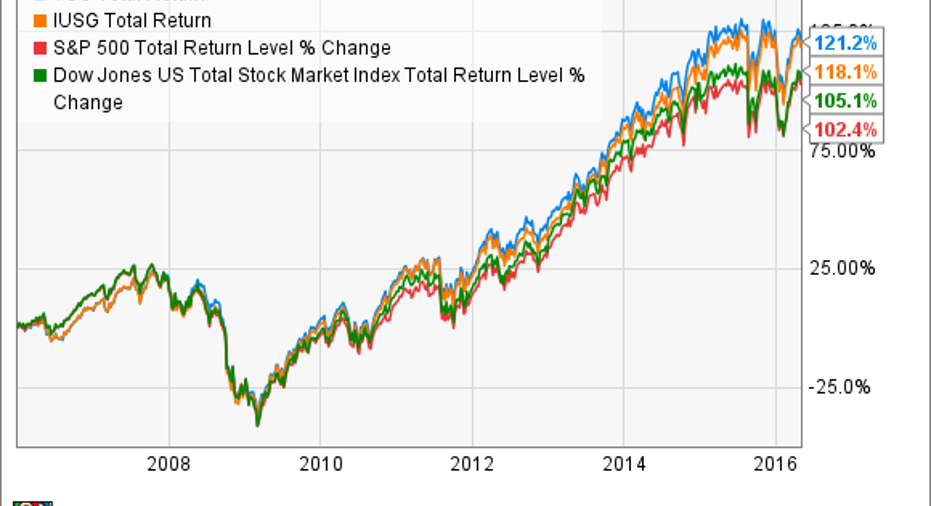

Buy a high-growth investment at a discountWhile the stock market has largely rebounded from the lows of earlier this year, there are a couple of index funds that are still trading below their 2015 highs:Vanguard Growth ETF andiShares Russell 3000 Growth Index (ETF).

Why invest in these funds? Because these two growth-focused ETFs have soundly outperformed theS&Pover the past decade:

VUG Total Return Price data by YCharts

Think about it this way: $1,000 invested in the Vanguard Growth ETF 10 years ago would be worth $2,212, and $1,000 invested in iShares Russell 3000 Growth Fund would be worth $2,118 today.

Even after the sharp rebound in recent months, long-term investors in these two growth funds will have a great shot at long-term market outperformance, and they should experience wonderful long-term returns.

Finally have an estate plan put together (or updated)It's never fun to talk about death. But there's one thing that's much, much worse: Picking up the pieces after a spouse or loved one dies with no estate plan in place.

Depending on where you live, a full estate plan including things like a revocable trust can cost more than $1,000, but in most states, you can at least get a comprehensive will drawn up for little to no cost. And even if you believe your odds of passing before your time are low, think about the additional -- and completely unnecessary -- stress you'll leave your loved ones with by not having a plan in place for your assets.

It's not just about honoring your wishes. It's also about identifying all of your assets, such as retirement accounts that may be with former employers, or other assets your survivors may not even know about. It will also make the legal process much easier if your assets are clearly identified in your will and your beneficiaries are equally clear. It's also about protecting those you care about from the potential consequences of state laws that might go against your wishes if there's no will in place.

And there's another ugly truth: Although most people like to think that their loved ones will be considerate and fair when it's time to divvy up the assets of a deceased family member, the reality is often quite different. Otherwise decent people may stoop to bickering over a dead loved one's material possessions. Even worse, if your will is out of date (e.g., if it bequeaths your home to your ex-spouse), then you may leave your family with a mess of your making.

You won't live longer just because you don't have a will, and you won't die faster if you have one. But your survivors are 100% more likely to have an easier time moving forward if you spend some time and money on estate planning.

Sharpen your mind and skillsWhether it's taking a class in your field of expertise, exploring a new discipline, or taking a general course in something like public speaking, you can likely sign up for an online class from an accredited college or university for a few hundred bucks. Not only could this help improve your value to your current employer, but it could also make you more marketable to prospective employees.

Furthermore, it doesn't have to be something specific to your current area of expertise. One big issue millions of American workers face today is that the skills employers seek often don't match up with what job seekers have. If you have an extra $1,000 or more to spend, then investing it in education or skills that improve your appeal to employers could be the smartest money you've ever spent.

The article 3 Smart Ways You Can Put $1,000 to Work Right Now originally appeared on Fool.com.

Jason Hall has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.