3 Oil Stocks to Buy in June

What a difference just a few months can make. After touching lows of $27 this spring, the price of a barrel of West Texas Intermediate crude has rallied to approximately $50. As one might expect, this near-90% rally has taken oil and gas stocks along for the ride -- but fear not: It's not too late for Foolish investors to get on board some of the best names in the space. While no one knows what the future holds for oil prices, it's hard to argue that you can go wrong buying strong, low-cost operators with balance sheets built to weather any downturn.With this in mind, three Fools put their heads together to come up with three oil and gas producers that are worthy of your consideration.

Image source: Getty Images.

Matt DiLalloDevon Energy's stock has been hammered over the past year, down more than 40% despite the fact oil is only down 15%. One reason for its relative underperformance is the company's decision to spend $2.5 billion to bolster its position in two emerging oil plays last December. The market didn't like that deal, as it thought Devon was not only overpaying for that acreage, but was weakening its balance sheet in the midst of one of the worst oil markets in decades.

Devon Energy didn't see it that way. Instead, it saw the chance to bulk up on one of the most profitable oil plays in the country at a time when prices in general were still depressed. Furthermore, it planned to jettison a boatload of non-core assets to maintain its balance sheet strength.

While the company did get off to a rough start this year, and was forced to slash its capex and its dividend due to the continued crash of oil prices, things are starting to look up for Devon. It recently announced a number of noncore asset sales, which will significantly bolster the company's cash position. Furthermore, with oil now back up to $50 a barrel, Devon Energy's cash flow and its drilling returns will vastly improve. In fact, with its burgeoning cash position, the company could be ready to start putting drilling rigs back to work and accelerating its production growth.

Devon Energy has a lot of upside. Not only was its stock unfairly sold off last year due to its acquisition, but it has tremendous growth potential as oil prices continue to rise. These catalysts make it a pretty compelling oil stock to buy this month.

Sean O'ReillyMy pick for an oil stock to buy in June, Occidental Petroleum , doesn't get discussed much by those looking to invest in the sector. But make no mistake: Occidental has a great deal to offer Foolish investors.

Occidental has a storied history, dating back to 1921. In the 1950s, it came to the attention of Dr. Armand Hammer, who eventually took on the role of CEO. Hammer expanded Occidental's operations internationally, as well as made forays into the chemical industry. Today, in spite of various scandals over the years, including the compensation package of former CEO Ray Irani and various questionable environmental and political practices, Occidental has emerged as a forward-thinking and progressive organization. In April,Vicki Hollub, a multidecade veteran of the Occidental organization, was appointed its CEO -- inaugurating a woman into the boys' club that is still, arguably, the executive realm of the oil and gas industry.

Like its peers, Occidental has found it difficult to generate a profit in the current oil environment. Looking past these difficulties, one quickly realizes that today's "oil recession"is an opportunity to buy shares in a nearly 100-year-old enterprise (no doubt having seen its fair share of hard times in that period), but an innovative one at that. As early as 1972, Occidental began researching what is now known as shale drilling -- a process it now uses with great effect.

Occidental Petroleum currently sports a market capitalization of around $57 billion, down from $78 billion or so at its peak in 2014. Clearly, Wall Street is still paying a premium for this high-quality enterprise. Occidental generated $5.9 billion in profits in fiscal year 2013 (the last full fiscal year before oil prices began their precipitous decline), and investors have strong reason to believe those days will return again. As recently noted in an investor presentationdated May 25, total spending per barrel of production is down 30% since FY 2014, and ongoing domestic production costs per barrel of oil equivalent are down 13% since FY 2015.

Increased efficiency and the ever-higher profits they imply if and when oil prices recover, coupled with a strong balance sheet, make Occidental Petroleum a great pick for the month of June.

A slow-growth oil company largely known for its refining business may not sound like a market-beating investment idea, but there are two key reasons that's not necessarily the case forPhillips 66:

- Phillips 66 management is investing in higher-growth midstream and petrochemical operations.

- Aggressive share repurchases and steady dividend growth will further augment per-share returns.

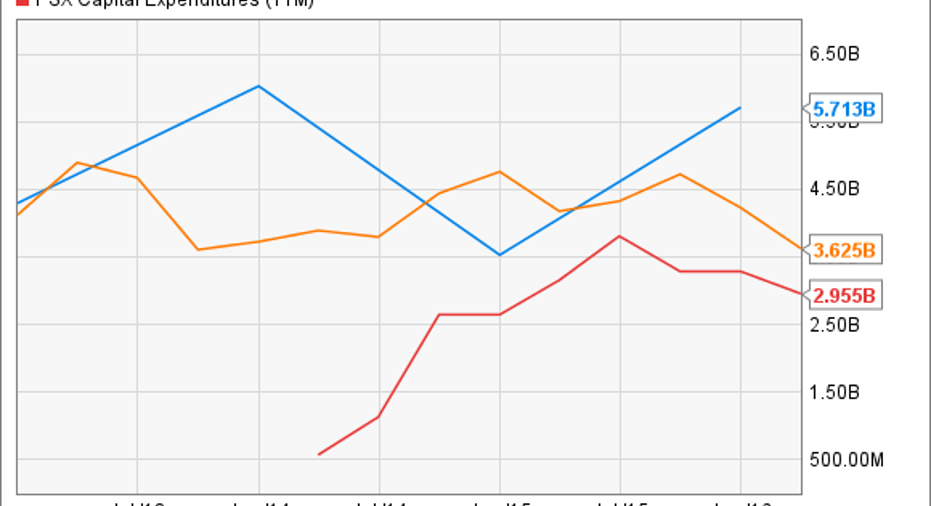

Here's the company's operating cash flow, net income, and its capital expenditures since spinning out ofConocoPhillips in 2012:

PSX Cash from Operations (Annual) data by YCharts.

As you can see, Phillips 66 spends a lot on capital investment, and that spending has been largely shifting to take advantage of higher-growth opportunities in natural gas infrastructure and petrochemicals manufacturing.

North America's massive natural gas reserves are driving this shift. Phillips 66's midstream segment is developing pipeline, gathering, storage, and export facilities to connect producers to markets, while its petrochemicals business, a joint venture withChevroncalled CPChem, is taking advantage of cheap domestic natural gas as a feedstock to produce high-demand chemicals used to make everything from fertilizer to tires to T-shirts.

Dividend growth and aggressive share buybacks will also likely keep driving per-share returns. Since going public, the company has repurchased 16% of its shares, and increased its quarterly dividend from $0.20 to $0.63 per share.

PSX Shares Outstanding data by YCharts.

Bottom line: If Phillips 66 management continues doing an excellent job of investing in the right growth projects, and aggressively returning excess cash to shareholders via dividend growth and share buybacks, this should be a market-beating long-term stock to own. Now's a great time to buy shares.

The article 3 Oil Stocks to Buy in June originally appeared on Fool.com.

Jason Hall owns shares of Phillips 66. Matt DiLallo owns shares of ConocoPhillips and Phillips 66. Sean O'Reilly has no position in any stocks mentioned. The Motley Fool owns shares of Devon Energy. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.