3 Numbers Explaining Bank of America's Credit Card Business

Image source: iStock/Thinkstock.

Credit cards are one of Bank of America's most important product lines, yet they're rarely a center of conversation among analysts and commentators.

Given this, I dug through the North Carolina-based bank's latest quarterly filing with the Securities & Exchange Commission to learn more about its credit card operations. What follows are three numbers that help put the extent of these operations in perspective.

1. Portfolio size

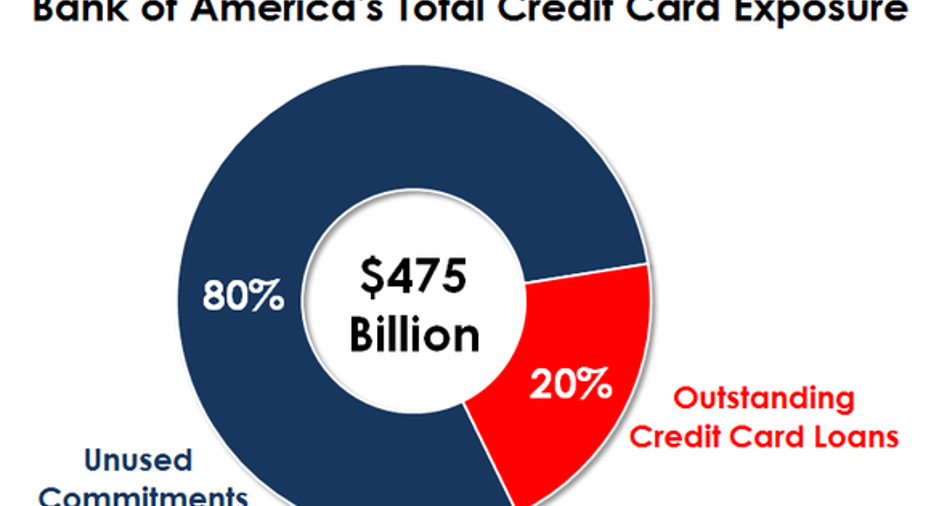

The first number is $96.4 billion. That's the size of Bank of America's credit card portfolio.

When you buy something on a Bank of America credit card, it records the purchase as a loan on its balance sheet. Its $96.4 billion portfolio is thus the cumulative amount of unpaid balances across all of its customers.

This is a big number, even for a bank with $2.2 trillion in assets on its balance sheet. Outside of residential mortgages, it's Bank of America's second largest category of loans, accounting for 22% of its outstanding consumer loans.

It's also a big number when you compare it to other banks. JPMorgan Chase and Citigroup both have larger portfolios, but Bank of America's is still three times the size of Wells Fargo's, the third-biggest U.S. bank by assets.

Data source: Quarterly regulatory filings. Chart by author.

2. Unused credit commitments

When you're talking about credit cards, the size of Bank of America's outstanding credit card portfolio is only half the issue. The other half concerns the size of its unused credit commitments.

Let's say you have a Bank of America credit card with a $2,000 balance and a $10,000 limit. The $8,000 difference is an unused credit commitment -- Bank of America has made it available, you just haven't used it.

If you add up the unused credit commitments of all Bank of America customers, it comes out to $378.6 billion. Another way to think about this is that Bank of America's customers have used an average of 20% of their available credit.

Data source: Bank of America's 1Q16 10-Q. Chart by author.

3. Credit card purchase volumes

The final number I found interesting was $51.2 billion: This is the purchase volume of Bank of America's customers in the first three months of the year. It's the amount they spent on their cards during the first quarter.

This is important not only for Bank of America, which generates interchange income every time its customers make a purchase with their cards, but also for the wider economy, as consumer expenditures account for roughly 70% of the nation's gross domestic product.

It's worth noting, moreover, that this figure doesn't include the value of debit card transactions by Bank of America customers, which added up to $69.1 billion in the first quarter. On an annualized basis, this amounts to roughly half a trillion dollars' worth of consumer purchases, which adds up to almost 4% of all consumer purchases made in the United States on an annual basis.

The article 3 Numbers Explaining Bank of America's Credit Card Business originally appeared on Fool.com.

John Maxfield owns shares of Bank of America and Wells Fargo. The Motley Fool owns shares of and recommends Wells Fargo. The Motley Fool recommends Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.